Your Guide to the Non Profit Organization Income Statement

Master your non profit organization income statement. Learn to prepare, analyze, and use it to boost your financial health and secure more grants.

Abdifatah Ali

Co-Founder

A nonprofit's income statement, more formally known as a Statement of Activities, is a financial report that lays out all your revenue and expenses over a specific timeframe—whether that's a month, a quarter, or a full year. In simple terms, it shows whether you ended the period with a surplus or a deficit, giving you a clear snapshot of your organization's financial health.

Why Your Statement of Activities Is Your Financial Story

Think of the Statement of Activities less like a dry accounting document and more like your organization's financial story for the year. It’s a narrative that shows everyone from your board members to your newest donors exactly how you brought in resources. More importantly, it shows how you put those resources to work to move your mission forward.

For anyone invested in your cause, this statement answers the most critical question they have: "How did you use our support to make a real impact?"

This document is so much more than a compliance checkbox. It's one of your most powerful tools for building trust and proving your effectiveness. While a for-profit business focuses on the bottom line (net income), a nonprofit's Statement of Activities centers on the change in net assets, highlighting both financial sustainability and your commitment to the mission.

The Core Purpose of an Income Statement

At its heart, the Statement of Activities serves three vital functions for any mission-driven organization. When you understand these purposes, the statement shifts from being a chore to a strategic asset.

- Transparency and Accountability: It gives stakeholders a clear, honest breakdown of where the money went. This is the bedrock of donor trust.

- Strategic Decision-Making: It provides your leadership team with the hard data they need to make smart choices about budgets, program expansion, and future fundraising efforts.

- Compliance and Reporting: This statement is a mandatory part of your annual reporting, including the Form 990 tax filing, ensuring you meet all legal requirements.

The health of the entire nonprofit sector can often be seen in the stories these statements tell. Recent data, for instance, paints a complex picture. In fiscal year 2025, while a strong 62% of nonprofits reported revenue growth on their income statements, about 25% saw declines and 14% stayed flat. This really highlights the different financial pressures organizations are facing and underscores why solid financial reporting is non-negotiable. You can dig into these trends and the state of nonprofit revenue growth over at CCS Fundraising.

A well-prepared Statement of Activities does more than just report numbers; it validates your mission. It shows that every dollar received is thoughtfully invested in creating change, turning financial data into a compelling case for continued support.

To better understand these differences, let's compare the nonprofit Statement of Activities with its for-profit counterpart, the Income Statement. While they both track money in and money out, their goals and language are fundamentally different.

Nonprofit vs For-Profit Income Statements at a Glance

This table makes it clear: nonprofits are telling a story of impact, while for-profits are telling a story of profit.

From Report to Narrative

Ultimately, mastering your Statement of Activities gives you control over your organization's financial narrative. It helps you justify funding requests, celebrate your wins, and pinpoint areas that need a little more attention.

This statement is a key piece of your broader financial communications, working hand-in-hand with other documents to paint a complete picture of your work. For example, it provides the financial backbone for the stories you tell in your annual report. You can learn more about how this all fits together by reviewing our guide on the ideal nonprofit annual report format.

By embracing this report as a storytelling tool, you can more effectively secure the funding you need to grow and sustain your important work.

Breaking Down Your Statement of Activities

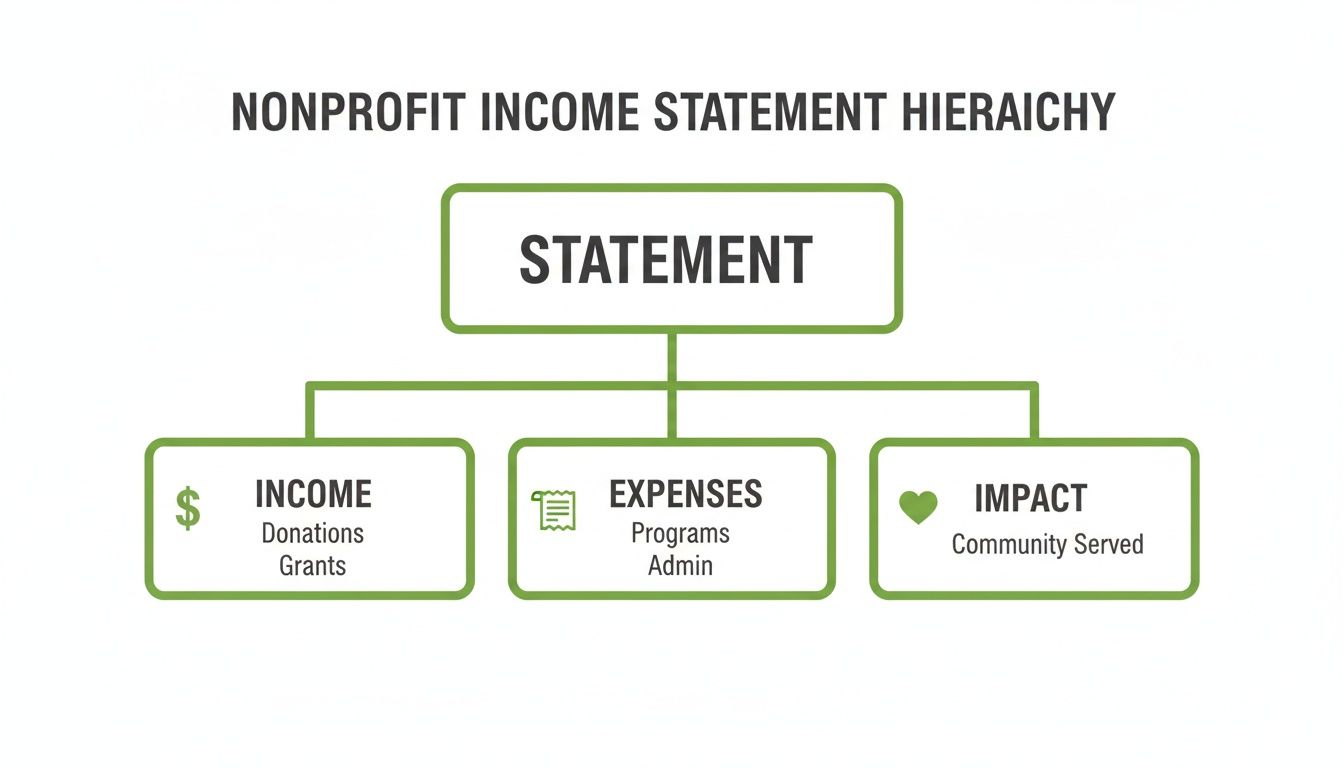

To really get a feel for your nonprofit's financial health, you need to know how to read its income statement, which in the nonprofit world is called a Statement of Activities. Think of it less like a dense financial document and more like a story with two main acts: the money that came in (revenue) and how you put that money to work for your mission (expenses).

This simple diagram shows how the statement connects the dots between your funding, your work, and your impact.

As you can see, the statement is designed to be a bridge, showing a clear path from a donation all the way to its effect on the community you serve. Let's walk through each of these building blocks so you can see exactly how they fit together.

The Two Sides of Nonprofit Revenue

Here’s the biggest difference between a nonprofit's Statement of Activities and a for-profit income statement. For-profits just track sales. We have to classify every dollar based on what the donor intended. This is a critical distinction, and it's one of the first things savvy funders look for.

All your revenue will fall into one of two buckets:

Revenue Without Donor Restrictions: This is your most flexible money. You can use it for anything that supports your mission, from keeping the lights on to launching a brand-new program. Think individual donations, general operating grants, and ticket sales.

Revenue With Donor Restrictions: This is money that comes with strings attached. The donor has earmarked it for a specific program, a particular timeframe, or a special project. A classic example is a grant given only to fund a youth literacy program. You are legally and ethically bound to honor those restrictions.

This separation isn't just an accounting headache; it's a promise you make to your supporters. It shows you’re a good steward of their money. When the goal of a restricted donation is met—say, the literacy program is completed—the funds are then "released from restriction." On the statement, you'll see them move over to the unrestricted side, ready to be spent.

A clear separation between restricted and unrestricted funds is the bedrock of donor trust. It proves your organization has the internal controls to honor every donor's specific intent, which is a major signal of good governance to grantmakers.

Understanding Your Income Streams

Within those two main categories, your Statement of Activities will list out all the different ways you bring in money. A healthy-looking statement usually shows a good mix of income types. This diversification signals financial resilience—it means you’re not dangerously dependent on a single source of funding.

Common income sources you'll see include:

- Contributions: Gifts from individual donors, local businesses, and corporate sponsors.

- Grants: Awards from government agencies or private foundations.

- Program Service Fees: Earned income from your mission-related activities, like tuition for a class or ticket sales for a performance.

- Special Events: The net income you make from fundraisers like galas, charity auctions, or 5K runs.

- Investment Income: Earnings from your endowment or other invested funds.

The Three Functional Expense Categories

After showing all the money that came in, the Statement of Activities switches gears to show how you spent it. To give donors and funders complete transparency, Generally Accepted Accounting Principles (GAAP) require nonprofits to sort every expense into one of three "functional" areas. This breakdown shows exactly how much money went directly to the mission versus how much it cost to run the organization.

1. Program Services Expenses

This is the good stuff—the costs directly tied to doing the work your nonprofit was created to do. For an animal shelter, this is vet care, pet food, and adoption events. For a food bank, it's the cost of buying and distributing food. This category is the heart of your mission.

2. Management and General Expenses

Often just called "admin" or "overhead," these are the essential background costs that keep the organization running. Think accounting fees, the executive director's salary, liability insurance, and the office rent. This is the crucial infrastructure that makes all your program work possible.

3. Fundraising Expenses

This bucket includes all the costs you incur to raise money. It covers things like the salaries for your development team, the cost of a direct mail campaign, grant writing consultants, or the software you use for online donations. Smart fundraising is an investment in your organization's future.

Sorting expenses this way lets anyone calculate key metrics, like the program expense ratio, which reveals what percentage of your spending goes straight to the cause. While there’s no single magic number, a healthy balance between these categories shows you're both focused on your mission and building a stable, sustainable organization.

How to Prepare Your Nonprofit Income Statement

Creating your first non profit organization income statement can feel intimidating, but you absolutely don't need to be a CPA to do it. Think of it like building with LEGOs. You start by gathering all your pieces (your financial records), sorting them into the right piles (revenue and expenses), and then clicking them together to build a clear picture of your mission’s financial health.

This guide will walk you through the process step-by-step, turning what seems like a complex chore into a manageable and even empowering task.

Step 1: Gather Your Financial Records

First things first, you need to pull together all your financial data for the period you're reporting on, whether it's a single quarter or your entire fiscal year. This is where consistent, day-to-day bookkeeping really pays off. The goal here is a complete paper trail of every dollar that came in and every dollar that went out.

Your essential documents will include:

- Bank Statements: The ground truth for all your cash transactions.

- Donation Records: Details on every grant, individual gift, and corporate sponsorship, making sure to note any donor-imposed restrictions.

- Invoices and Receipts: Proof of all payments you've made for goods and services.

- Payroll Records: All the details on salaries, benefits, and payroll taxes for your team.

- Grant Agreements: The actual contracts that spell out funding amounts, timelines, and exactly how the money can (and can't) be used.

To make life easier, dedicated finance management software can be a game-changer. These tools can automate much of this gathering process, saving you precious time and cutting down on the risk of human error.

Step 2: Classify Your Revenue and Expenses

With all your data in hand, it’s time to sort. This is arguably the most crucial part of preparing a non profit organization income statement. Every single transaction needs to land in the right bucket to ensure your final report is transparent, accurate, and compliant.

Start with your revenue. You’ll classify all incoming funds into two main groups: "With Donor Restrictions" or "Without Donor Restrictions." This distinction is the bedrock of nonprofit accounting; it shows funders and your board that you’re stewarding their contributions responsibly.

Next, you have to classify every single expense. This isn't just about what you spent money on (like "rent" or "printing"), but why you spent it. Each expense must be assigned to one of three functional categories:

- Program Services: These are the costs directly tied to carrying out your mission. Think of the supplies for your after-school program or the veterinarian bills for your animal shelter.

- Management & General: This is the essential overhead that keeps the lights on—administrative salaries, office utilities, insurance, and other core operational costs.

- Fundraising: This bucket includes all costs associated with raising money, from running a gala to paying for your grant writer's time.

This functional classification tells a powerful story. With over 12.5 million people employed by U.S. charitable organizations, the sector is a major economic force. And when you look at how nonprofits are funded, you see that over 80% of revenue comes from program service fees and government contracts. Accurately tracking how that money is spent is essential for demonstrating impact.

Step 3: Allocate Shared Costs

Here's a common sticking point. What do you do with costs that support the whole organization, like your office rent or the executive director’s salary? These are shared costs, and you need a logical way to spread them across your three functional expense categories.

An allocation plan is simply a documented, reasonable method for distributing these shared expenses. A common approach is to allocate costs based on how staff spend their time or how much office space each function uses.

For example, if your program director spends 70% of their time on program work, 20% on general administration, and 10% on fundraising events, you would allocate their salary using that same 70/20/10 split. The key is to be consistent and to write down your methodology. Auditors and grantmakers will definitely ask to see it.

Step 4: Assemble the Statement of Activities

You’ve gathered, sorted, and allocated. Now it’s time for the final assembly. Using a spreadsheet or your accounting software, you’ll put all the pieces together.

- Revenue Section: Start by listing all your income sources, separated into columns for "Without Donor Restrictions" and "With Donor Restrictions." Then, total up each column.

- Expense Section: Next, list your expenses by their functional category (Program, Management & General, and Fundraising).

- Calculate the Change in Net Assets: Finally, subtract your total expenses from your total revenue. This gives you the bottom line: your surplus (or deficit) for the period.

This final number instantly tells you whether your organization brought in more money than it spent. As you put this statement together, you'll see how closely it mirrors your budgeting process. If you're looking to strengthen that connection, our sample nonprofit budget template can be a great tool to help guide your financial planning.

How to Analyze Your Statement for Strategic Growth

Your Statement of Activities is so much more than a compliance document. Think of it as a strategic map that tells the real story of your nonprofit's financial health. When you learn to read between the lines, you can turn this report into a powerful tool for making smarter decisions and spotting trends before they become problems.

The goal here isn't to find one "right" answer. It’s about asking the right questions. Your income statement holds the clues to your operational strengths and weaknesses, but you have to know where to look. This is how you transform financial data from a simple rearview mirror into a GPS for your organization's future.

Asking Key Strategic Questions

Let's start by treating your statement like a diagnostic tool. Your mission is to uncover the narrative behind the numbers and use it to shape a proactive, forward-thinking strategy.

Here are the fundamental questions you should be asking:

- Is our revenue diversified? Are we leaning too heavily on a single grant or one big fundraising event? A healthy mix of funding—from individual gifts and corporate sponsorships to earned income—is a sign of real financial stability.

- How efficient are our programs? What's the relationship between our program expenses and the results we’re actually delivering? This line of questioning connects your spending directly to your mission's impact.

- Are our fundraising efforts paying off? Take a hard look at how your fundraising costs stack up against the revenue they bring in. This is how you calculate the return on investment for your different campaigns and decide what to double down on.

- Are we operating with a surplus or a deficit? A consistent surplus is fuel for reinvestment and growth. On the other hand, recurring deficits are a major red flag that demands immediate attention.

By analyzing your Statement of Activities, you're essentially conducting a financial health check-up. Spotting trends early—like rising administrative costs or a slow decline in individual giving—allows you to make corrective adjustments before they become critical issues.

To get a better sense of how your operations impact revenue, consider how strategic nonprofit website development can be a game-changer for donations and supporter engagement. A strong online presence is often a key piece of a diversified income puzzle.

Turning Data Into a Funder Narrative

One of the most valuable uses of this analysis is in building a compelling story for your funders. Grantmakers and major donors absolutely look at your non profit organization income statement to gauge your sustainability and your ability to manage their investment well.

Don't just hand them the numbers—interpret them. If your administrative costs went up, explain why. Maybe you invested in new accounting software for better financial oversight or finally hired a development director to expand fundraising. Frame these as strategic investments, not just "overhead."

For instance, if your statement shows a significant surplus, explain your plan for it. Will it seed a new pilot program, build up your cash reserve for stability, or be invested in technology to scale your impact? A clear plan demonstrates foresight and strong governance. You can dig deeper into growing your financial base in our guide on how to increase nonprofit revenue streams.

Calculating Key Financial Ratios

To take your analysis a step further, you can calculate a few key ratios directly from your Statement of Activities. These metrics provide standardized benchmarks for assessing your financial performance, turning raw numbers into truly actionable insights. They also give you a way to compare your organization to others in the sector.

Here are some of the most essential ratios that can be pulled right from your income statement.

Key Ratios to Understand Your Financial Health

By tracking these ratios consistently over time, your leadership team and board can get a clear, ongoing picture of your financial health. This data-driven approach allows you to set realistic goals, demonstrate strong financial stewardship, and confidently plan for a sustainable future.

Common Mistakes and How to Avoid Them

An accurate non profit organization income statement is the foundation of donor trust and legal compliance. But even with the best intentions, it's surprisingly easy for small errors to creep in and undermine your credibility. These slip-ups usually aren't malicious; they often come from a few common misunderstandings about nonprofit accounting rules.

The good news? Once you know what to look for, these traps are completely avoidable. Let's walk through the most frequent mistakes I see in the field and give you clear, practical ways to make sure your financial story is always accurate, transparent, and ready for scrutiny.

Putting a few simple checks and internal controls in place will do wonders for protecting your organization’s reputation and building rock-solid confidence with your funders.

Misclassifying Revenue and Restricted Funds

This is probably the single biggest error I see nonprofits make: mishandling restricted funds. It's a classic mistake to receive a grant for a specific program and just lump it into your general operating account. Doing this doesn't just violate accounting principles—it breaks the promise you made to your donor.

- What Not to Do: You get a $25,000 grant earmarked for a new youth mentorship program. You log it as general "grant revenue" and dip into it to cover administrative salaries that have nothing to do with the new program.

- What to Do Instead: Record the $25,000 as revenue "With Donor Restrictions." Then, as you actually spend money on the mentorship program, you "release" those funds from restriction on your Statement of Activities. This moves the money to the unrestricted side to offset those specific program expenses.

Getting this right sends a powerful signal to grantmakers that you have your financial house in order.

Don't just track what you received; track the intent behind it. Your first line of defense is a clear system for tagging restricted funds in your accounting software. This simple step ensures you honor every donor's wishes.

Improperly Allocating Shared Expenses

Many nonprofits either take a wild guess when allocating shared costs like rent and salaries or, even worse, don't allocate them at all. This can seriously distort your financial picture, making your administrative costs look way too high or your program expenses seem artificially low.

An auditor or a savvy funder will immediately raise an eyebrow at a statement where all the utilities are dumped into the "Management & General" bucket. They know your program staff used those lights and that office space, too. A logical, documented allocation plan isn't just a good idea—it's essential.

The Fix: A Clear Allocation Method

The best approach is to create a simple, reasonable, and consistent allocation plan. A time study is one of the most common and defensible methods.

- Survey Your Staff: Ask your team to track their time for a typical week, breaking it down by percentage spent on program activities, administration, and fundraising.

- Create Averages: Tally up the hours and calculate the average percentages for different roles or for the organization as a whole.

- Apply Consistently: Use these percentages to split your shared costs. For example, if your team spends 70% of its time on programs, you should allocate 70% of the office rent and utilities to Program Services expenses.

Forgetting In-Kind Donations

Volunteered time and donated goods have real, tangible value, and they belong on your non profit organization income statement. Forgetting to include them understates both your revenue and your expenses, which paints an incomplete picture of what it truly takes to run your programs.

- What Not to Do: A local marketing firm donates a full-day branding workshop for your staff, a service they normally bill at $5,000. You gratefully accept but don't record the transaction.

- What to Do Instead: You should record $5,000 as in-kind contribution revenue and a corresponding $5,000 as a management or program expense (depending on the workshop's focus). This shows the true level of community support you have and the real cost of your operations.

Accurately tracking these donations demonstrates the full breadth of your organization's support network and gives a much more honest view of your financial health.

Frequently Asked Questions

Even after you get the hang of financial statements, some questions always pop up when you try to apply the rules to real-life situations. This section is all about tackling those common head-scratchers that nonprofit leaders often face with their nonprofit organization income statement, also known as the Statement of Activities. Think of this as your practical guide for getting past points of confusion and feeling more confident about your organization's financial story.

We're going to step away from the theory and get right into the nitty-gritty, addressing the specific scenarios you'll almost certainly run into.

What Is the Difference Between a Statement of Activities and a Balance Sheet?

This is easily one of the most common mix-ups for new board members and even seasoned leaders. The best way to keep them straight is to think of a video versus a photograph.

The Statement of Activities (your income statement) is the video. It shows your organization's financial performance over a period of time—usually a quarter or a full fiscal year. It tells the whole story of your revenue coming in and your expenses going out, ending with whether you had a surplus or a deficit.

On the other hand, the Statement of Financial Position (your balance sheet) is a snapshot. It captures your financial health at a single moment in time, like the very last day of the year. It simply lists what you own (assets), what you owe (liabilities), and what's left (your net assets). Both are vital for a complete financial picture, but they tell very different parts of your organization's story.

How Do We Handle a Multi-Year Grant on Our Income Statement?

Multi-year grants are fantastic for planning and stability, but the accounting rules can feel a bit backward at first. When a funder promises you a multi-year grant, GAAP (Generally Accepted Accounting Principles) requires you to recognize the full value of that pledge as revenue in the year you receive the promise, not as the cash trickles in.

Here’s how that plays out in the real world:

- The Scenario: You just secured a $300,000 grant that will be paid in three annual installments of $100,000.

- Year 1 Treatment: Right away, you have to record the entire $300,000 on your Statement of Activities as revenue "With Donor Restrictions." In this case, the restriction is based on time—the donor intends for you to use the funds over three years.

- Year 2 & 3 Treatment: In each of the following years, as time passes, you'll "release" that year's portion from the restriction. This is a bookkeeping entry where you reclassify $100,000 from restricted net assets to unrestricted net assets, making it available to spend.

This process ensures your nonprofit organization income statement reflects the full commitment from the funder while also clearly showing stakeholders which funds are actually available to use right now.

Do We Still Need an Income Statement If We Are a Small, All-Volunteer Nonprofit?

Yes, absolutely. Even if you're a tiny organization with no paid staff, a formal nonprofit organization income statement is critical. For starters, it’s a matter of accountability to your donors, no matter how small their gifts. It’s how you prove you're being a good steward of their support.

Beyond that, it gives your volunteer board the ability to make smart, strategic decisions with real data instead of just guessing. It helps answer basic but essential questions like, "Did our annual bake sale actually make money?" or "Can we truly afford to launch that new community project we're so excited about?"

And most importantly, you’ll need formal financial statements to:

- Apply for just about any grant.

- File your Form 990 to maintain your 501(c)(3) tax-exempt status with the IRS.

- Register as a charity with state officials.

Building good financial habits from day one creates a strong foundation for growth and makes it much, much easier to attract bigger funding down the road.

How Can We Improve Our Program Expense Ratio for Funders?

The program expense ratio—the slice of your budget spent directly on your mission—is a metric that many funders look at closely. But improving it isn't just about cutting overhead; it's about smart strategy and, crucially, accurate accounting.

First, make sure you're accurately allocating shared costs. So many nonprofits shortchange their programs by not allocating a fair portion of costs like rent, utilities, and leadership salaries. If a manager spends half their time on Program A, half of their salary should be counted as a program expense. Implementing a logical allocation plan, as we discussed earlier, can legitimately and significantly improve your ratio overnight.

Second, start looking for ways to work smarter. Could a new piece of software or a better internal process reduce administrative tasks, freeing up more staff time for mission-related work?

Finally, think about strategic growth. When you secure a new grant that's earmarked for program expansion, your ratio naturally improves because your program spending grows faster than your overhead. The goal isn't just to chase an arbitrary number, but to build a ratio that truly reflects your organization's impact and sustainability.

Ready to take the guesswork out of grant writing and compliance? Fundsprout is an AI-powered platform designed to help your nonprofit find the right funding opportunities, craft winning proposals, and manage your reporting with ease. From discovering relevant grants to auto-populating funder templates, Fundsprout helps you build a stronger financial future for your mission. Discover how Fundsprout can help you succeed.

Try 14 days free

Get started with Fundsprout so you can focus on what really matters.