Your Guide to a Sample Nonprofit Budget Template That Works

Download our free sample nonprofit budget template. Master your finances, simplify grant reporting, and build a sustainable financial future for your mission.

Abdifatah Ali

Co-Founder

Ready to finally get a grip on your nonprofit's finances? Here is your downloadable sample nonprofit budget template in both Excel and Google Sheets formats. It's designed to give you immediate clarity and a solid structure for your financial planning.

Your Essential Nonprofit Budgeting Toolkit

A well-built budget is so much more than a spreadsheet; it’s the financial command center for your mission. It turns numbers on a page into a strategic roadmap, helping you tell a powerful financial story to funders, your board, and your own team. When you move beyond simple expense tracking, a dynamic budget becomes your best tool for navigating the realities of fluctuating donations and rising costs.

The Strategic Value of a Good Budget

In the current climate, proactive budgeting isn't just good practice—it's essential for survival. Nonprofits are constantly dealing with shifts in funding and broader economic pressures that directly impact planning.

For instance, federal discretionary domestic spending, a critical funding source for many, is projected to fall by up to 8% in real terms over the next two fiscal years. With nearly one-third of U.S. nonprofits relying on government support, these kinds of contractions make strategic budgeting more critical than ever. You can read more about these financial trends and what they mean for the sector.

A budget isn’t about restriction; it’s about empowerment. It gives you the data-driven confidence to make bold decisions, allocate resources for the biggest impact, and prove your organization’s stability to grantmakers.

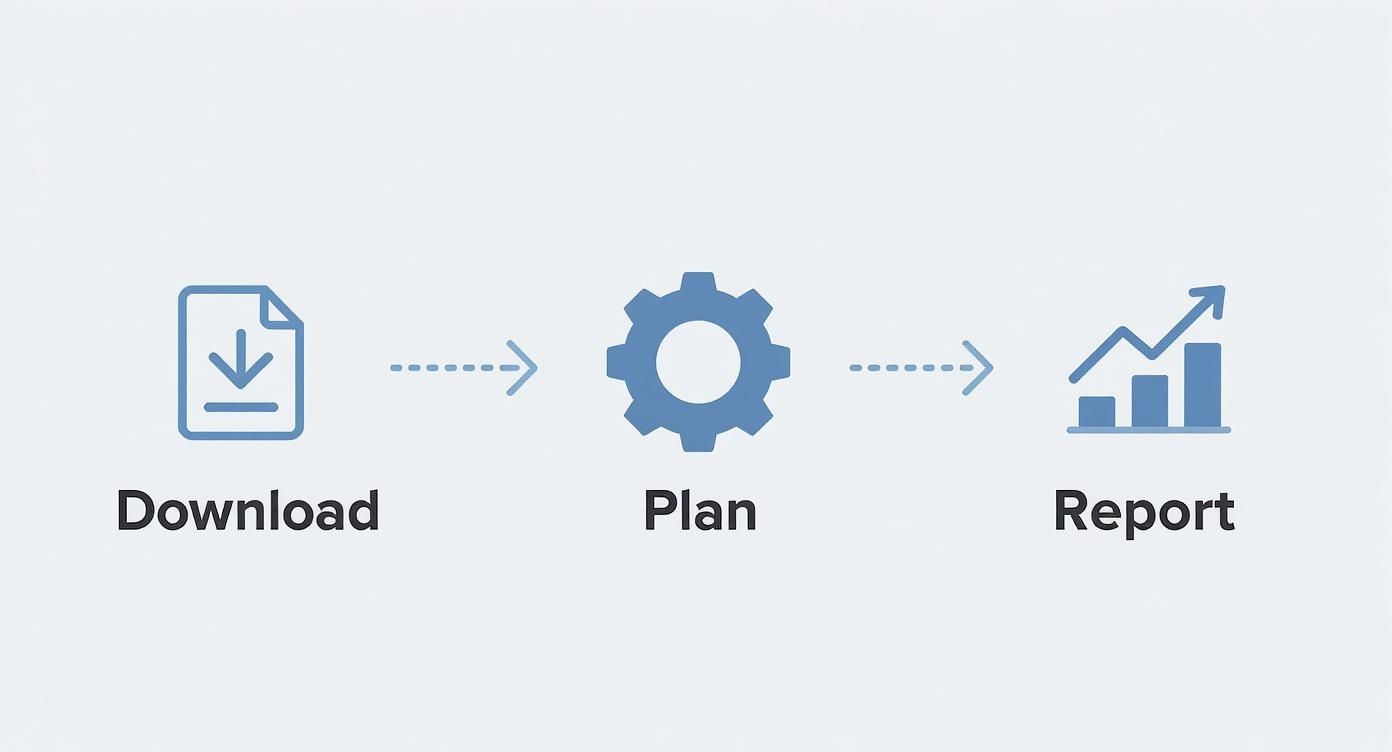

Getting started is straightforward. The infographic below shows the simple, three-step cycle of using this template.

This process really highlights how the template isn't a one-and-done document. It's a living tool for continuous financial management—from the initial setup to ongoing strategic reporting.

Understanding Your Budget Template Components

Our downloadable toolkit isn't just a single spreadsheet. It’s a set of interconnected sheets, each built to solve a specific financial planning problem.

Here’s a quick look at what’s inside and how each piece helps you manage your finances more effectively.

Inside Your Nonprofit Budget Template

A quick look at the sheets included in your download and the specific problems they solve for your financial planning.

Each of these components works together to give you a complete and practical picture of your organization's financial health, helping you plan with confidence.

Building Your Annual Operating Budget

The annual operating budget is the financial heart of your organization. Think of it as the master plan, the single document that maps out every dollar you expect to bring in and spend over the next fiscal year. This isn't just a spreadsheet; it's the tool that keeps every activity—from your core programs to your payroll—squarely aligned with your mission.

So, let's build one. Grab the sample nonprofit budget template you downloaded and open the "Annual Operating Budget" tab.

For this walkthrough, we'll pretend we're the "Community Arts Alliance," a small nonprofit providing free art classes to local youth. Our mission is to create a realistic, funder-ready budget for the coming year. This is less about filling in cells and more about strategic foresight.

Forecasting Your Revenue Streams

First things first: income projection. One of the most common mistakes I see is over-the-top optimism. A much stronger approach is conservative and evidence-based. Let's break down our revenue into clear, defensible categories.

- Individual Donations: Looking at last year, the Community Arts Alliance raised $45,000 from individual donors. We have a big year-end appeal planned, and we feel a 5% growth goal is reasonable. Let's budget $47,250.

- Grants: We have a signed grant agreement for $25,000 from the City Arts Council—that's confirmed money. We've also submitted three other proposals, but until we get that award letter, we don't count them. This is how you keep a budget grounded in reality.

- Corporate Sponsorships: A local bank has sponsored our summer program for $10,000 for the past two years. We'll pencil that in, but I'm also making a note to call our contact and confirm they plan to renew.

- Earned Income: Our annual art auction is a reliable earner, historically netting around $8,000 after all expenses are paid. We'll stick with that number.

This granular approach gives us a total projected revenue of $90,250. Notice how every single figure is tied to a specific source or historical data. That's exactly the kind of diligence funders and your own board need to see.

Strategically Categorizing Expenses

With our income projected, it's time to look at expenses. The key here is all about proper categorization. You'll see the template divides expenses into three functional buckets: Program, Administrative, and Fundraising. This isn't arbitrary; it mirrors the IRS Form 990 and is the industry standard.

Program Expenses

These are the costs tied directly to delivering your mission. For our Community Arts Alliance, that looks like:

- Salaries & Wages: The portion of our Art Instructor's salary spent actually teaching classes.

- Program Supplies: All the clay, paint, and canvases needed for the youth workshops.

- Venue Rental: The monthly cost for the studio space where the magic happens.

Administrative Expenses

You might know this as overhead or Management & General (M&G). These are simply the costs of keeping the lights on.

- Salaries & Wages: The Executive Director's salary, plus the slice of the Art Instructor's time spent on admin tasks.

- Rent & Utilities: For the small back office, which is separate from the program studio.

- Insurance: General liability and D&O insurance are non-negotiable.

- Professional Fees: Costs for our part-time bookkeeper and the annual audit.

Fundraising Expenses

Quite simply, this is what it costs you to raise money.

- Salaries & Wages: A percentage of the Executive Director's time is dedicated to donor meetings and grant writing.

- Special Event Costs: The direct expenses for our art auction, like catering and marketing materials.

- Online Donation Platform Fees: Those small but steady processing fees from our online giving portal.

Key Takeaway: A crystal-clear distinction between program, administrative, and fundraising expenses is non-negotiable. It proves you're financially transparent and helps you calculate your overhead rate—a metric funders always look at.

Handling Personnel Costs Accurately

Personnel is almost always your biggest line item, and it's also the easiest place to make a costly error. You can't just budget for gross salaries. You absolutely must include fringe benefits and payroll taxes.

A reliable way to do this is to calculate fringe as a percentage of total salaries. This bucket should include:

- Payroll Taxes: FICA (Social Security and Medicare) and unemployment taxes (FUTA/SUTA).

- Benefits: Health insurance, retirement contributions, and paid time off.

For our Community Arts Alliance, we'll estimate fringe benefits at 22% of gross salaries. So, if our total salaries are $60,000, we must budget an additional $13,200 for these associated costs. Our total personnel expense becomes $73,200. Forgetting this step can blow a hole in your budget before the year even starts.

This kind of careful planning is more important now than ever. A recent sector-wide survey highlighted that financial stability is a growing concern for nonprofits, driven by rising costs and shrinking government support. Many organizations reported government funding cuts of over 10%, forcing them to make tough choices about staff or programs. Understanding the findings on nonprofit financial stability helps frame the real-world pressures your budget needs to withstand.

This challenging environment makes unrestricted funding, like that from operating grants, incredibly valuable. These are the grants that support the essential administrative and fundraising activities that are often the hardest to fund. You can dive deeper into how to secure operating grants for nonprofit organizations in our guide. By building a detailed, realistic annual budget, you're not just planning—you're creating the foundational document you need to pursue and manage this kind of critical funding.

Getting Granular: How to Build Budgets for Programs and Grants

Your annual operating budget is your nonprofit's financial roadmap for the entire year. It’s the 30,000-foot view. But when it comes to funders and grantmakers, they want to get on the ground level. They're investing in a specific outcome, and they need to see exactly how their money will make that happen.

This is where a dedicated program budget shines. It’s more than just a spreadsheet; it’s a powerful storytelling tool that translates your mission into direct, tangible action. It answers the one question every funder is asking: "What will it really cost to achieve these results?"

To get started, head over to the 'Program Budget' tab in our sample nonprofit budget template. We designed this sheet specifically to isolate the financials of a single initiative. It's perfect for building a grant proposal or even just managing a program internally.

The All-Important Split: Direct vs. Indirect Costs

At the heart of any solid program budget is the clear separation of direct and indirect costs. I can't stress this enough. Getting this right isn't just about good accounting; it shows funders you have a sophisticated understanding of what it takes to run your programs well.

- Direct Costs: These are the expenses that exist only because of the program. If you shut down the program tomorrow, these costs would disappear. Think of salaries for program-specific staff, workshop supplies, or client transportation.

- Indirect Costs (or Overhead): These are the shared, central expenses that keep the whole organization running, which in turn allows your program to succeed. We're talking about a portion of the Executive Director's salary, the office rent, accounting software, and insurance.

Funders expect to see both. Trust me, a budget showing only direct costs is a huge red flag. It tells a grant reviewer that the organization might not be planning for sustainability and doesn't grasp the true cost of doing its work.

Let’s Build a Sample Program Budget

Let's walk through a real-world example. Imagine we're creating a budget for a new "Youth Success Tutoring Program." The plan is to provide weekly tutoring for 50 middle school students over a full school year. We're putting together an application for a $50,000 grant.

First up, the direct costs. These are usually the easiest to calculate and justify.

- Personnel: We'll need a part-time Program Coordinator ($15,000/year) and two Tutors ($10,000 each). That’s a direct salary total of $35,000. We’ll also add a standard 20% for fringe benefits ($7,000), bringing our total direct personnel cost to $42,000.

- Supplies: We'll need workbooks, pencils, and other materials. We’ve budgeted $50 per student, which comes out to $2,500.

- Student Transportation: To make the program accessible, we'll offer bus tokens to students who need them. Let's budget $1,500 for the year.

- Volunteer Background Checks: This is a non-negotiable safety step. At $25 per check for our 20 volunteers, that’s another $500.

Add it all up, and our total direct program expenses are $46,500. Now for the part people often get nervous about: the indirect costs.

Expert Tip: Don't shy away from including indirect costs in your grant proposals. I’ve seen people worry it makes them look "too administrative." The opposite is true. Sophisticated funders appreciate seeing the full cost of running a high-quality program. It shows you’re a savvy operator planning for the long haul.

Calculating and Justifying Your Indirect Costs

Indirect costs are the operational lifeblood of your organization. They keep the lights on and provide the essential infrastructure that makes your direct program work possible.

The most common method for allocating these is an indirect cost rate—a percentage of your direct costs. Every funder is different, but a cap of 10-15% is pretty standard. For this example, we’ll use a 10% rate.

The calculation is simple:

$46,500 (Direct Costs) x 10% = $4,650 (Indirect Costs)

That $4,650 represents the tutoring program's fair share of the organization's overhead. It helps cover the slice of the Executive Director's time spent on oversight, the portion of the rent for the space where planning happens, and the accounting software used to track every dollar.

Finally, we add our direct and indirect costs together for the grand total:

$46,500 (Direct) + $4,650 (Indirect) = $51,150 (Total Program Cost)

Notice our total cost is just a bit over the $50,000 grant we’re requesting. That's actually a good thing. It communicates to the funder that they would be a cornerstone supporter while also showing that we have other revenue streams (like individual donations) to cover the full expense. This kind of detailed, transparent financial story gives grant reviewers the confidence they need to invest.

For a deeper dive into this process, be sure to check out our complete nonprofit program budget template and guide.

Mastering Your Monthly Cash Flow

Your annual operating budget is the roadmap, but your monthly cash flow is the gas in the tank. You can have the best map in the world, but you won't get far if you can't pay for fuel.

This is where the 'Monthly Cash Flow Projection' tab in our sample nonprofit budget template becomes so incredibly important. It helps you stop thinking about what you'll spend and start focusing on when the money actually comes in and goes out.

I've seen it happen time and again: a nonprofit looks great on paper with a projected annual surplus, but they're staring down a cash crunch in August because a huge grant payment won't arrive until October. That’s not just a minor headache. It’s a genuine crisis that can put payroll and rent payments at risk, threatening to derail your most important work.

A cash flow projection is your early warning system. It helps you anticipate the natural ups and downs of your bank account, turning what could be a nasty surprise into something you can actually plan for and manage.

Charting Your Financial Peaks and Valleys

Let's use a real-world example. Think of an animal rescue organization mapping out its year. Their annual budget looks solid, even showing a small surplus. But when we dig into the timing of their finances, a potential disaster starts to emerge.

- Steady Expenses: Their biggest costs are predictable. Payroll for shelter staff, rent for the building, and utility bills are due every single month, like clockwork.

- Lumpy Income: Their income, on the other hand, is anything but steady. Their main fundraising gala is a huge success in May. They also rely on a large foundation grant, but that check always lands in the third quarter, usually around September.

When you plot this out on a cash flow forecast, a worrying pattern becomes obvious. July and August look incredibly tight. The money from the gala is long gone, but the big grant check is still weeks away. Without this forecast, the leadership team might not see the cliff they're approaching until their bank balance is flashing red.

This is the entire point of cash flow management. It isn’t about looking backward at your accounting. It's about looking forward so you can make smart decisions before you're in a pinch, not while you're in the middle of one.

By spotting this two-month gap way back in April, the organization has plenty of time to react. They could plan a small summer fundraising appeal to tide them over or maybe even arrange with their biggest supplier to extend payment terms for a month. What could have been a full-blown crisis becomes a simple, strategic adjustment.

Building Your Own Cash Flow Projection

Using the template is pretty straightforward. You'll just work month by month, plugging in all the cash you realistically expect to come in and go out.

Cash Inflows (Receipts):

This is for all the cash you expect to actually hit your bank account in a given month.

- Grant Payments: This is a big one. Don't list the full grant award when it's approved. Instead, put the payment amount in the specific month you know the check will arrive.

- Individual Donations: Look at your history. You probably get a big bump in giving in December and a dip in the summer. Your projection should reflect that reality.

- Program Fees: If you run workshops or sell tickets, estimate the monthly revenue based on past trends and any current registrations.

Cash Outflows (Disbursements):

Here, you'll list everything you plan to spend. The key is to list it in the month the money actually leaves your account.

- Payroll & Benefits: This is usually your biggest and most consistent cash outflow.

- Rent & Utilities: Another set of predictable bills to plug in each month.

- Program Supplies: Planning a summer camp? Even if the camp runs in July, the cash you spend on supplies in June belongs in the June column.

- Major Payments: Don't forget those big, one-off expenses like your annual insurance premium or a large equipment purchase. Slot them into the correct month.

Truly understanding your cash flow is also fundamental to a smart fundraising strategy. When you can pinpoint your leanest months, you can better time your appeals and look for sources of funding for nonprofits that might offer more predictable payment schedules.

Once you’ve entered all your inflows and outflows, the template automatically calculates your net cash flow for each month (what came in minus what went out). More importantly, it gives you a running ending cash balance. That final number is your guide. If you see it dipping into the red in a future month, you know exactly when you need to act. This simple exercise transforms your budget from a static document into a living, breathing management tool that ensures you always have the cash on hand to keep your mission moving forward.

Avoiding Common Nonprofit Budgeting Pitfalls

Even the most passionate and well-run nonprofits can hit financial speed bumps that put their mission at risk. Having a solid sample nonprofit budget template is your first line of defense, but knowing what financial traps to look for is just as important. Let’s talk about some of the most common mistakes I see organizations make—and how you can steer clear of them.

One of the biggest culprits? Overly optimistic revenue forecasts. It’s so easy to get swept up in the excitement of a new fundraising campaign or the possibility of a big grant. The problem is, when you build a budget on best-case scenarios, you're setting yourself up for a cash flow crisis. Hope is not a financial strategy.

A much safer approach is to ground your projections in what you know—your past performance and funding you have already secured. This builds a budget based on reality, not just ambition.

Build a More Resilient Forecast

To avoid the "hope and a prayer" approach, I always recommend building a three-tier forecast right into your budget spreadsheet. This gives you a much more honest picture of your potential financial health.

- Pessimistic Scenario: What happens if that major grant falls through? Or if your annual appeal brings in 15% less than last year? This is your bare-bones survival budget.

- Realistic Scenario: This is your most likely path, based on your track record and confirmed funding. Think of this as your primary operating plan.

- Optimistic Scenario: Here’s where you can dream a little. If you do exceed your goals, what will you do with the extra funds? This lets you plan for growth without banking on it.

Using this method turns your budget from a static, rigid document into a dynamic tool that prepares you for whatever comes your way.

Mismanaging Indirect Costs and Reserves

Another costly mistake I see all the time is failing to account for indirect costs in grant proposals. When you only budget for the direct, visible expenses of a program, you’re forcing your unrestricted funds to subsidize the grant. This slowly starves your core operations—the very infrastructure that makes your programs possible.

Always make sure you include a line item for indirect costs. You can often justify this with a federally negotiated rate or a standard 10-15% of direct costs.

Forgetting to build and maintain an operating reserve is like trying to run your mission without a safety net. A reserve fund—typically three to six months of operating expenses—is what allows your organization to weather unexpected financial storms, such as a delayed grant payment or an unforeseen repair.

The best practice here is to get your board to approve a formal policy for your reserve fund. This policy should spell out its purpose, how big it should be, and the specific rules for when you can dip into it and how you'll replenish it. This keeps everyone on the same page and protects that fund for genuine emergencies.

The financial world for nonprofits is always in flux, which makes these kinds of risk-mitigation strategies more critical than ever. We're seeing a huge focus on diversifying revenue streams as organizations navigate economic uncertainty. With nearly all U.S. nonprofits operating on budgets under $5 million—and over 90% managing less than $1 million annually—there's simply no room for error. The best budget templates now help you track these different income sources and build in contingency plans.

You can learn more about the key nonprofit trends impacting financial planning. By getting ahead of these common pitfalls, you can turn potential weak spots into strengths, building a more resilient and sustainable organization for the long haul.

Nonprofit Budget FAQs: Your Questions Answered

Even with the perfect template, questions are bound to come up. Budgeting isn't just about plugging in numbers; it's about strategy, storytelling, and smart planning. I've gathered some of the most common questions I hear from nonprofit leaders to help you navigate those tricky spots.

How Do I Budget for a Brand-New Nonprofit with No Financial History?

Starting from a blank slate can feel intimidating, but it's also a chance to get things right from the very beginning. Since you don't have past performance to guide you, your budget needs to be built on solid research and a realistic fundraising strategy.

First, do some detective work. Find a few established nonprofits in your area with a similar mission and scale. You can usually find their public Form 990s online, which are a goldmine of information for benchmarking costs like salaries, rent, and insurance. This gives you a real-world baseline to work from, rather than just guessing.

On the revenue side, be both optimistic and conservative. Don't just pull a fundraising goal out of thin air. Instead, build your revenue projections from the ground up based on your fundraising plan. Detail which grants you'll apply for, how many individual donors you plan to cultivate, and any corporate sponsors you're targeting.

A great strategy for new organizations is to create three different budget scenarios: a 'bare bones' version to keep the lights on, a 'realistic' one that achieves your core goals, and an 'aspirational' budget for when everything goes right. This shows funders you’re not just a dreamer—you’re a planner who is ready for anything.

What Is a Budget Narrative and Why Do Funders Require It?

Think of a budget narrative as the story behind your spreadsheet. It’s a document that accompanies your budget in a grant proposal, explaining why you need the money you're asking for. It brings your numbers to life.

For instance, instead of a line item that just says $5,000 for "Marketing," your narrative would break it down: "This funding will cover printing 2,000 program brochures ($1,500), running targeted social media ads to recruit 50 new volunteers ($2,500), and our email marketing software for the year ($1,000)."

A good narrative does three things really well:

- It proves you've done your homework and are transparent about your costs.

- It justifies every dollar, showing funders their investment will be used wisely.

- Most importantly, it connects the money directly to the mission, making your request far more compelling.

How Often Should We Review and Adjust Our Nonprofit Budget?

Your budget should be a living, breathing document, not something you create in January and file away. At a minimum, your board or finance committee needs to be looking at a "budget vs. actual" report quarterly, though I strongly recommend doing it monthly. This report is simple but powerful: it shows what you planned to spend and earn versus what actually happened.

These regular check-ins are your early warning system. Is fundraising lagging? You can pivot your strategy now. Is a program consistently going over budget? You can investigate why before it becomes a major problem. This kind of proactive oversight keeps small hiccups from turning into full-blown crises and helps your team make smarter decisions all year long.

What Is the Difference Between a Capital Budget and an Operating Budget?

Getting this right is fundamental to clean financial management. Your operating budget is all about the day-to-day. It covers the predictable revenue and expenses required to run your programs and keep the lights on for one fiscal year—think salaries, rent, program supplies, and utilities.

A capital budget is for the big, one-off stuff. These are major, long-term investments that aren't part of your regular operations. We're talking about things like:

- Buying a new van or even a building

- A major renovation of your office space

- Purchasing expensive equipment that will last for years

Because these are significant, long-term assets, they're budgeted and funded separately, often through a dedicated capital campaign or specific grants. Keeping them separate from your operating budget gives everyone a much clearer picture of your organization's ongoing financial health.

Ready to take the guesswork out of grant funding? The Fundsprout AI platform helps you find the right funders, craft winning proposals, and manage your grants from start to finish. Stop chasing dead ends and start building a sustainable funding pipeline. Discover how Fundsprout can power your mission.

Try 14 days free

Get started with Fundsprout so you can focus on what really matters.