Audit Requirements for Nonprofits: Your 2026 Compliance

Understand the essential audit requirements for nonprofits in 2026. This guide details compliance steps and best practices for financial transparency.

Abdifatah Ali

Co-Founder

Your team finally landed the grant. The board is excited, program staff are already planning delivery, and development is drafting the announcement. Then someone forwards the agreement and highlights one phrase: audited financial statements required.

That moment catches a lot of nonprofit leaders off guard. They assumed audits were mainly a big-organization issue, or something tied only to federal funding. Instead, they find out that audit requirements for nonprofits often come from several places at once, and the rule that matters most may have nothing to do with the threshold everyone talks about.

A new Executive Director usually doesn't need a lecture on accounting theory. They need to know what applies, what doesn't, what can wait, and what needs immediate attention. That's the practical problem. A nonprofit can be well run, mission focused, and still get tripped up by a state filing rule, a renewal requirement, or a clause buried in a grant agreement.

That's why this topic matters. An audit is more than a finance exercise. It affects registration, grant renewals, board oversight, budgeting, calendar planning, and how confidently you can say yes to funding opportunities. If your organization works across multiple states, receives government funds through an intermediary, or applies to foundations with formal due diligence, the compliance picture gets crowded fast.

If you're also sorting out the broader finance side of compliance, this guide to managing tax for charities is a useful companion because tax compliance and audit readiness often live in the same operational reality.

Introduction When Does Good News Mean More Paperwork

The most common mistake I see is assuming there is one audit rule. There isn't. There are several, and they operate independently.

A nonprofit might be below the federal threshold and still need audited statements because a state requires them for charitable registration, or because a grantmaker wrote the requirement directly into the award terms. Another organization may not be legally required to audit yet, but its board or funding strategy may make an annual audit the right move anyway.

Practical rule: Don't ask only, "Do we need an audit?" Ask, "Who might require one, on what basis, and by when?"

That shift matters because the consequences are different. A federal audit issue brings one kind of risk. A missed state filing creates another. A missed funder condition can stall payment, delay renewal, or weaken your credibility during reporting season.

For a new Executive Director, the smartest starting point is simple. Build a list of every possible trigger. Federal funds, state registration states, grant agreements, bylaws, and board policies. Then sort them by deadline and type of scrutiny required. Once you do that, the audit requirements get much less mysterious.

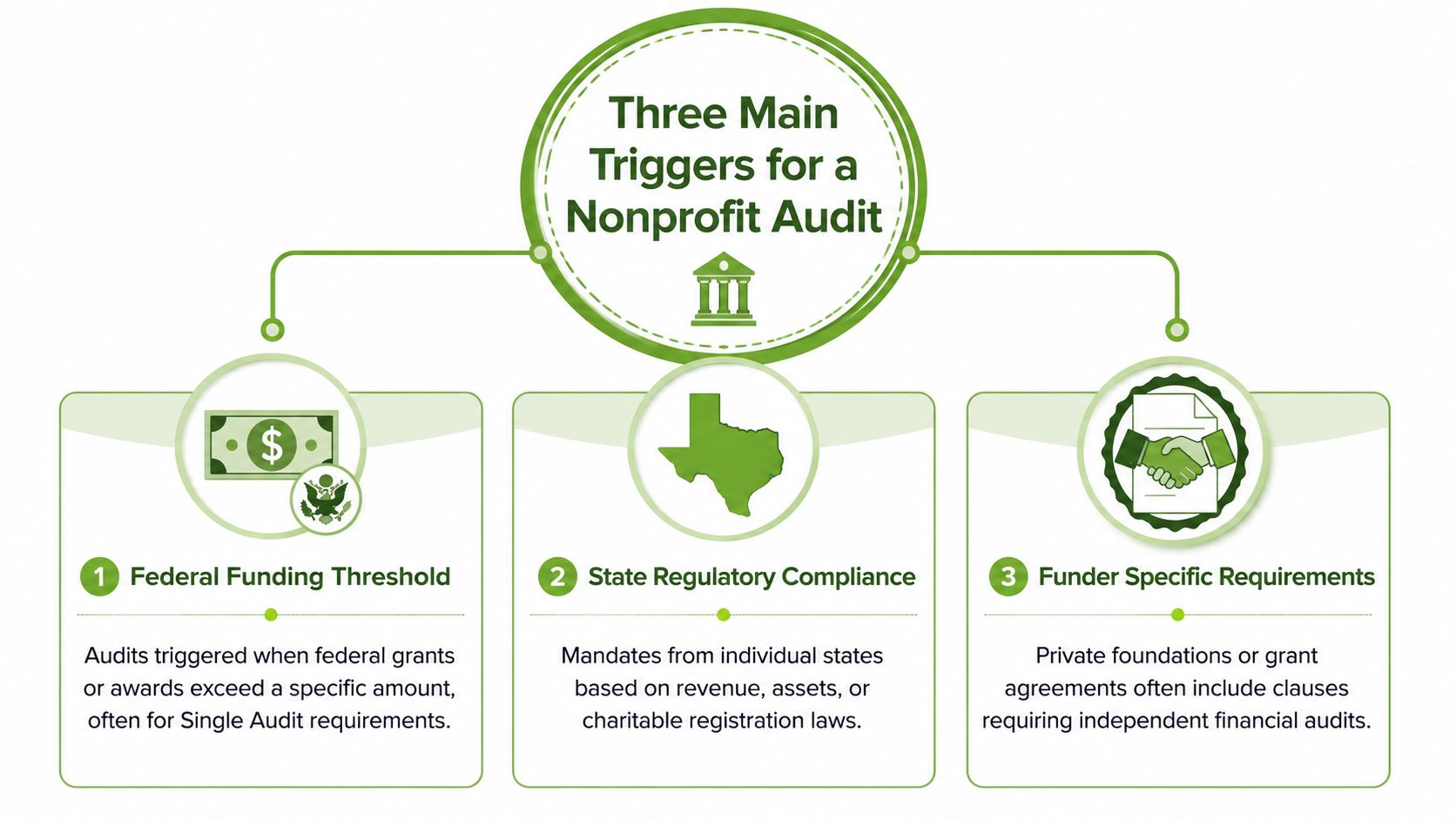

The Three Main Triggers for a Nonprofit Audit

If you want a clean mental model, think of nonprofit audit compliance as a three-legged stool. Federal mandates, state rules, and funder requirements each support part of the structure. Ignore one leg, and the whole thing wobbles.

Federal funding

Federal rules get the most attention, and for good reason. They can trigger a Single Audit, which is a specific type of audit tied to federal awards rather than just general financial reporting.

But federal rules aren't the only gate. A lot of leaders hear the federal threshold and stop there. That's where trouble starts, especially for smaller organizations receiving mixed funding from grants, reimbursements, and pass-through awards.

State compliance

States often create the more surprising requirement. Some tie audit obligations to charitable solicitation registration. Others use revenue-based thresholds. Some accept a review at one level and require a full audit at another.

One of the clearest examples of the gap comes from Brady Ware's nonprofit audit compliance overview, which notes that federal rules require audits only for nonprofits expending over $1M in federal funds since October 1, 2024, while Louisiana mandates audits at $500K revenue and financial reviews at $200K. That's the compliance trap in one sentence.

For leaders outside the U.S. or those comparing governance practices across jurisdictions, this Australian NFP audit guide is useful because it shows how audit obligations can also vary sharply by local legal structure and regulator expectations.

Funder-specific requirements

Private foundations, corporate funders, and public agencies can all add their own audit expectations. Sometimes the grant agreement requires a full independent audit. Sometimes it asks for audited financial statements from the most recent year. Sometimes it allows a review. Sometimes the agreement is vague and needs clarification before you sign.

That matters because grant terms don't wait for your internal readiness. If the agreement says you must submit audited statements and you don't have them, the issue isn't theoretical. It's operational.

Why these triggers stack

These triggers are not either-or. A nonprofit can face all three at once.

- Federal exposure: You expend enough federal awards to trigger a Single Audit.

- State exposure: You register to solicit contributions in states with separate audit thresholds.

- Funder exposure: A private grant agreement requires audited statements even if no law does.

A nonprofit can be compliant in one lane and still fail in another.

That is why audit requirements for nonprofits should be managed as a full compliance map, not as a one-time accounting question.

Understanding Different Types of Financial Scrutiny

When someone says, "We need an audit," the first response should be, "What kind?" People use the word loosely. The actual requirement may be a financial review, a financial statement audit, or a Single Audit. Those are not interchangeable.

What each engagement is meant to do

A financial review is narrower. It gives limited assurance and usually involves less testing and less disruption. In practice, it may satisfy a state filing rule or a funder that wants some outside verification but not full audit-level work.

A financial statement audit is broader. The auditor examines whether the financial statements are fairly presented under GAAP. This is the format most boards and funders mean when they request "audited financials."

A Single Audit goes further because it adds federal compliance testing. It isn't just about whether the numbers are presented fairly. It also looks at internal controls and whether the organization followed the rules attached to federal awards.

Financial Review vs Financial Audit vs Single Audit

| Attribute | Financial Review | Financial Statement Audit | Single Audit |

|---|---|---|---|

| Primary purpose | Limited outside scrutiny of financial statements | Independent opinion on financial statements | Financial statement audit plus federal award compliance testing |

| Level of assurance | Limited assurance | Reasonable assurance | Reasonable assurance on statements plus compliance work on federal programs |

| Typical trigger | State rule, lender, board, or funder may accept it | State rule, board policy, or funder requirement | Federal award expenditure threshold under Uniform Guidance |

| Scope of work | Inquiry and analytical procedures | Broader testing of balances, transactions, and controls | Financial audit work plus testing of internal controls and compliance over federal awards |

| Best fit | Smaller organizations with lighter requirements | Organizations needing audited statements for stakeholders | Organizations with federal funding exposure that crosses the required threshold |

| Common misunderstanding | Treated as “basically an audit” when it isn't | Assumed to satisfy all grant compliance demands | Assumed to replace all state or funder requirements automatically |

What works in practice

The best approach is to match the engagement to the requirement, not your preference.

If a state allows a review, a review may be perfectly sensible. If a funder specifically requires audited financial statements, trying to substitute a review usually wastes time. If federal awards trigger a Single Audit, there is no lighter alternative that will satisfy that rule.

Ask for the exact wording. "Audited financial statements," "independent review," and "Single Audit" each point to a different engagement.

The operational trade-off

More scrutiny means more preparation. A review can still be work, but a full audit usually requires deeper reconciliations, stronger schedules, and cleaner documentation. A Single Audit raises the bar further because grant files, procurement support, subrecipient monitoring, and internal control evidence all matter.

That's why leaders should separate two questions. First, what type of engagement is required? Second, is our internal documentation strong enough to get through it without chaos?

Navigating Federal Single Audit Requirements

The federal trigger is clearer than most state rules. It's still demanding, but at least the standard is defined.

According to Gatekeeper's explanation of nonprofit audits, the primary federal audit trigger for nonprofits is the Single Audit requirement, mandated under the Uniform Guidance when an organization expends $1,000,000 or more in federal awards during its fiscal year, effective for fiscal years beginning on or after October 1, 2024.

What counts toward the threshold

The key word is expends, not just receives. The compliance question is tied to federal awards used during the fiscal year. That distinction matters for organizations that receive multi-year grants, reimbursement-based contracts, or pass-through funds administered by a state agency.

Pass-through funds still count when they are federal in origin. If a state agency distributes federal grant dollars to your nonprofit, those expenditures can be part of the Single Audit calculation. This is one reason small finance teams misread their exposure. They track the payer, but not the source.

Another area that causes confusion is shared costs. If your nonprofit allocates staff time, occupancy, or administrative expenses across programs, your indirect cost approach needs to be defensible. This overview of indirect cost calculation methods is helpful because weak cost allocation tends to surface during grant compliance reviews.

What auditors examine

A Single Audit is built around three practical questions.

- Are the financial statements fairly presented under GAAP?

- Are internal controls over federal programs sound?

- Did the nonprofit comply with the rules attached to the federal awards?

Those questions sound tidy on paper. In the field, they mean document requests, walkthroughs, reconciliations, and support for how decisions were made.

The verified guidance in the source material also notes four broad document groups that often matter in this process:

- Financial records: general ledger details, reconciliations, and supporting schedules

- Governance records: board minutes and organizational approvals

- Program compliance evidence: support showing funds were used as intended

- Vendor and subrecipient trail: records that show who was paid and under what terms

Where nonprofits usually stumble

The federal threshold isn't the hard part. Counting correctly is. The harder part is proving that spending matched the award terms and that controls existed before the auditor arrived.

Common weak spots include:

- Grant files spread across systems: Finance has one version, programs have another.

- Unclear pass-through identification: Staff know the contract came from a state agency but don't know whether the funds are federal.

- Loose cost allocation support: Payroll or shared expense allocations exist, but the backup is thin.

- Subrecipient confusion: Teams treat every external partner like a vendor and miss the compliance difference.

If federal funds touch multiple departments, one person should own the master award inventory. Without that, Single Audit prep becomes a scavenger hunt.

For leaders who may cross the threshold soon, the smartest move is early classification. List every award, identify whether it is federal or pass-through federal, note the assistance listing details where applicable, and align each award with the records that support spending and compliance. That work is far easier before year-end than after the auditor starts asking questions.

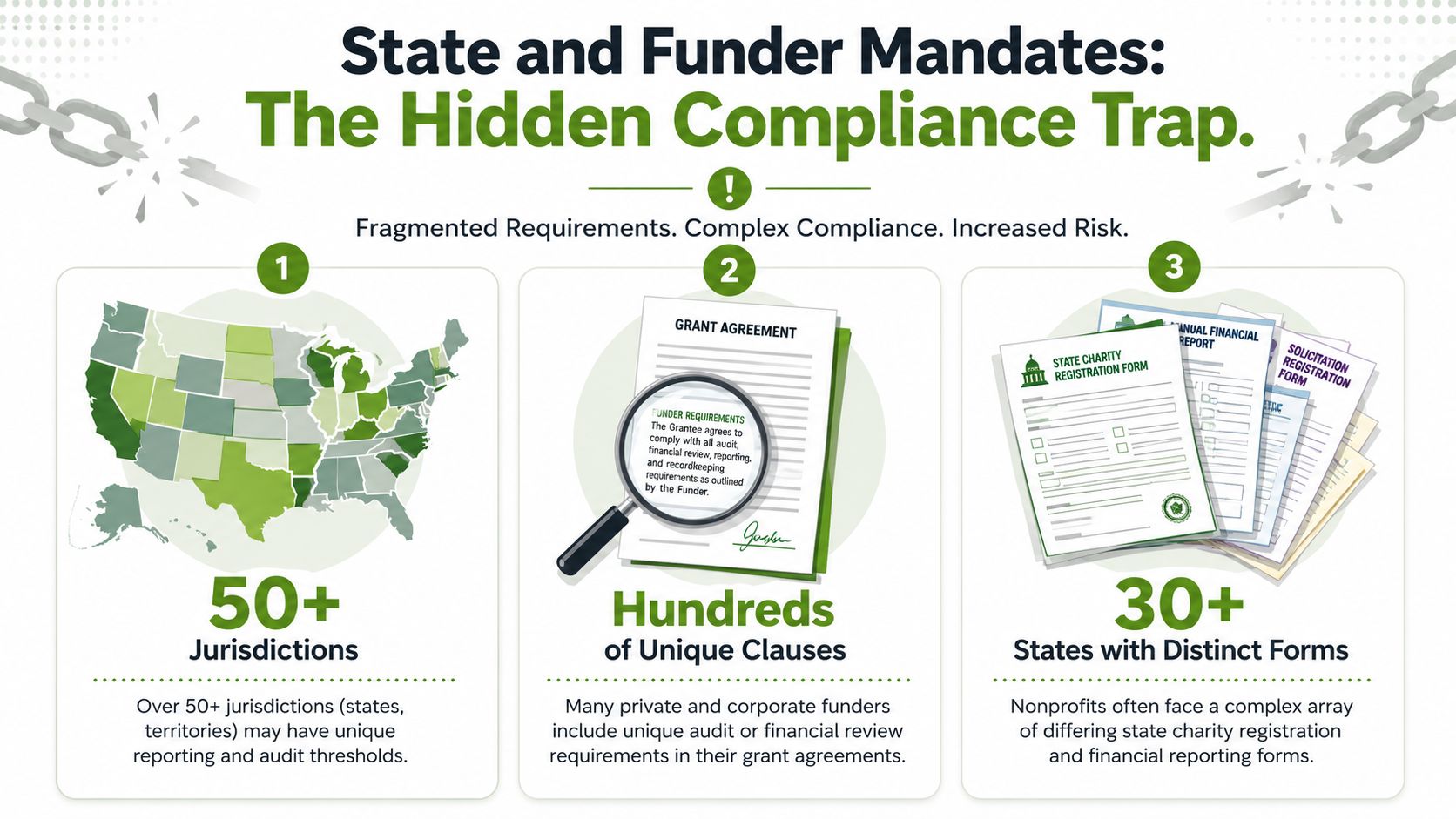

State and Funder Mandates The Hidden Compliance Trap

Most nonprofit leaders know to watch federal funding. Fewer realize how often state registration law or a grant agreement creates the first real audit requirement.

That's the hidden trap. A nonprofit can sit well below the federal Single Audit threshold and still be required to obtain audited financial statements.

The state-by-state patchwork

The U.S. doesn't have one charitable solicitation standard. It has a patchwork.

According to Cogency Global's review of charitable registration audit rules, 21 states require an audit for charitable registration renewals and annual report submissions, and 16 states require one for initial registration, with thresholds for contributions or revenue ranging from $300,000 to $1 million.

That means a nonprofit's fundraising footprint matters, not just its accounting size. If you solicit in multiple states, your compliance burden can rise before your internal team feels “large enough” to justify formal audit planning.

Specific examples make the point clearer:

- Illinois: audit requirement at $300,000 or more in charitable contributions, as noted in the same Cogency Global source.

- Georgia: exemption threshold of $1 million in revenue, excluding investment income, also from that source.

- California: nonprofits with annual revenues of $2 million or more must obtain an audit and submit it to the Attorney General within nine months of fiscal year-end, according to SMCO CPA's summary of nonprofit audit rules.

Those aren't close calls. They reflect entirely different state approaches.

Why smaller nonprofits get blindsided

The organizations most likely to miss these rules are often disciplined but lean. They have a controller or outsourced bookkeeper, a development lead, and an Executive Director juggling everything else. No one has time to manually compare every state registration rule against current revenue and contribution patterns.

That gap gets wider when funders add custom requirements. A private foundation may ask for your most recent audited statements as part of due diligence. A corporate grant may condition payment on a clean set of external financials. A government pass-through award may not trigger a federal Single Audit, but still demand stronger documentation than your team currently maintains.

For teams trying to stay organized across awards and deadlines, a centralized grant compliance tracking system can reduce the risk of missing these overlapping obligations.

The trap isn't just the threshold. It's the assumption that one threshold answers every question.

What actually works

Treat state and funder requirements as separate workstreams.

One practical method is to maintain a simple matrix with these columns:

| Compliance area | What to track |

|---|---|

| State registrations | States where you solicit, filing deadlines, audit or review trigger |

| Grant agreements | Exact language on financial statements, reviews, or audits |

| Renewal obligations | Whether the requirement appears only at initial filing or also at renewal |

| Responsible owner | Staff member, consultant, or outside firm accountable for follow-up |

Then add one discipline that most nonprofits skip. Review every new funding agreement before signature for finance implications, not just program terms. If the grant requires audited statements and your organization does not have them, that issue should be resolved before acceptance, not discovered during reporting.

Your Practical Audit Preparation Checklist and Timeline

A smooth audit doesn't begin when the auditor sends the request list. It begins months earlier, when your records are still easy to fix.

Three to six months before year-end

Start with readiness, not paperwork. Confirm what kind of engagement you need, whether your board expects it, and when the final report will be required for filings or funders.

Then clean up the core records:

- Reconcile cash: Every bank and credit account should tie out cleanly.

- Review grant files: Agreements, amendments, reporting schedules, and restrictions should be easy to locate.

- Check board records: Minutes should reflect major approvals and financial oversight.

- Test internal controls: Make sure approval and segregation practices are being followed in reality, not just in policy.

This is also the right time to identify whether your organization will need extra support. Small nonprofits often underestimate how much staff time an audit consumes. If you need a process guide designed for lean teams, this resource on audits for small organizations is a practical starting point.

One to two months before fieldwork

Now gather the schedules your auditor will likely request. Different firms use different formats, but the categories are predictable.

Prepare items such as:

- Cash and balance sheet support: bank reconciliations, prepaid schedules, payable detail, receivable aging

- Revenue support: grant agreements, contribution records, restriction schedules, deferred or refundable revenue detail

- Expense support: payroll summaries, contractor payments, major vendor listings

- Governance and tax records: board list, board minutes, prior financial statements, recent filings

- Fixed assets and commitments: asset listings, leases, and debt documents if applicable

A lot of audit stress comes from version confusion. Finance has a PDF. Development has a spreadsheet. Programs have email approvals. Pick one shared repository and use it consistently.

Auditors don't mind questions. They do mind three conflicting versions of the same schedule.

During fieldwork

Respond in batches. Keep a request log. Assign one internal coordinator even if several staff members own different records.

The coordinator's job is not to answer every question personally. The job is to control flow, maintain version discipline, and make sure responses are complete. That one habit can prevent weeks of circular follow-up.

Many teams also benefit from seeing how a structured workflow supports audit readiness in practice:

After the draft arrives

Read the draft carefully. Focus on findings, management comments, and any internal control recommendations. Then do three things quickly.

- Brief the board or finance committee in plain language.

- Assign corrective actions with owners and deadlines.

- Update your recurring calendar so the same issue doesn't return next year.

The strongest audit prep systems aren't glamorous. They are orderly. They tell you where the agreement lives, who approved the expense, when the report is due, and which version is final. That's what makes the next audit easier.

Choosing an Auditor Managing Costs and Common Pitfalls

Selecting an auditor is not a commodity purchase. It's a judgment call with operational consequences.

A firm that understands nonprofits will ask better questions about restrictions, grant revenue, board governance, and compliance expectations. A firm that mostly serves other industries may still be competent, but your team often ends up teaching them the basics of nonprofit reporting while the clock runs.

What to look for in a firm

Start with fit.

- Nonprofit experience: Ask what kinds of nonprofit clients they serve and whether they handle the specific engagement you need.

- Clear engagement scope: The proposal should say whether the work is a review, financial statement audit, or Single Audit.

- Communication style: You want a team that explains issues plainly and gives realistic timelines.

- Request discipline: Good auditors send organized lists and explain priority items.

Don't skip the engagement letter. Read what the auditor expects from management, what deadlines apply, and what services are not included. Many unpleasant surprises come from assumptions made before kickoff.

Managing cost without cutting the wrong corners

Audit cost is real, and for smaller nonprofits it can feel disproportionate. The wrong response is to delay decisions, choose the cheapest option blindly, or assume cleanup can happen after fieldwork starts.

What usually keeps cost manageable is not bargain shopping. It's preparation.

A prepared client gives the auditor complete schedules, timely answers, and clean reconciliations. An unprepared client creates rework. Rework usually costs more, even if the original proposal looked cheaper.

Pitfalls that create avoidable pain

Here are the issues that most often turn a routine audit into a draining one:

- Waiting too long: If you start after year-end with messy books, every task becomes urgent.

- Treating grants casually: Restrictions, reporting terms, and amendments need to be documented, not remembered.

- Letting development and finance diverge: Revenue records should align across teams.

- No internal owner: Without a coordinator, requests scatter and responses conflict.

- Choosing on price alone: A low proposal can become expensive if the process drags or findings multiply.

The best auditor relationship feels rigorous, not adversarial. They should challenge your documentation without making your staff afraid to ask questions.

Done well, an audit strengthens more than compliance. It tightens routines, improves board reporting, and gives your organization more confidence when the next funding opportunity arrives.

If your team wants a simpler way to keep grant documents, deadlines, reporting requirements, and compliance records in one place, Fundsprout can help. It's built for mission-driven nonprofits that need to track funding requirements from application through renewal, with a clearer audit trail and less last-minute scrambling.

Try 14 days free

Get started with Fundsprout so you can focus on what really matters.