A Nonprofit's Guide on How to Calculate Indirect Costs

Learn how to calculate indirect costs for your grant proposals. Our guide covers formulas, the de minimis rate, and NICRA to help you secure full funding.

Abdifatah Ali

Co-Founder

Calculating your indirect costs is pretty straightforward on the surface: you identify all your shared operational expenses, add them up into a single "indirect cost pool," and then divide that total by a direct cost base. But the result of that simple math is what’s so important—it reveals the true cost of running your programs, helping you secure the full funding you actually need to deliver on your mission.

Why Mastering Indirect Costs Is a Game Changer

Figuring out your indirect costs is so much more than a box-checking accounting task. It’s a core strategy for ensuring your nonprofit's long-term health and ability to make a real impact. These expenses—you’ve probably heard them called overhead or Facilities & Administrative (F&A) costs—are the essential, everyday resources that allow your programs to exist and succeed.

Think about the rent for your office, the salary of your executive director, the utility bills, or your IT support. You can't cleanly tie any of these costs to a single grant-funded project, but every single one of your projects relies on them. Without these foundational expenses, the lights go out, the computers don't work, and there's no leadership steering the ship.

Shifting from "Burden" to Engine

For far too long, overhead has been seen as a necessary evil or, even worse, a sign of inefficiency. This mindset isn't just outdated; it's genuinely harmful. It forces nonprofits to constantly underinvest in their own core infrastructure, which inevitably leads to staff burnout, high turnover, and weaker programs.

The truth is, your indirect costs are the engine that powers your mission forward. They are a direct reflection of your organization's core strength and stability. When you accurately calculate and recover these costs through your grants, you can finally:

- Invest in your team with fair salaries, benefits, and professional development.

- Maintain a safe and effective workspace with reliable technology and facilities.

- Ensure strong governance and financial oversight, which is key to building funder trust.

- Innovate and grow because you have the capacity to actually plan for the future.

When you leave these very real expenses out of your grant proposals, you're essentially asking for less money than your programs actually cost to run. This creates a dangerous cycle of scarcity where your team is stretched thin and the entire organization is just one unexpected expense away from a crisis.

A Blackbaud analysis shows organizations that accurately claim these costs in proposals can secure 20% more funding by demonstrating the full operational picture. This avoids the common trap where 40% of nonprofits underclaim indirects, which can erode their financial reserves by up to 18% each year. You can get more insights on how nonprofits calculate indirect costs at Planergy.com.

Getting this calculation right is a strategic imperative. It completely changes the conversation with funders from "How low is your overhead?" to "What does it truly take to achieve these amazing outcomes?" When you present a clear, data-backed indirect cost rate, you're making a powerful case for the full investment your mission deserves—allowing your nonprofit to thrive, not just survive.

Figuring Out Your Cost Pools and Allocation Bases

Before you can even think about calculating a rate, you’ve got to get your financial house in order. The first real step is sorting every single one of your organization's expenses into one of two buckets: direct costs or indirect costs. Getting this right is everything—it's the foundation for a rate that is both accurate and easy to defend.

Direct costs are usually the easy part. These are the expenses you can point to and say, "That belongs to Project X." Think of the salary for a program coordinator who spends 100% of their time on a single federally funded initiative, or the art supplies purchased exclusively for that program's workshops.

Indirect costs, however, are all about the shared expenses. These are the essential costs of doing business that keep the lights on and support all your programs, not just one. This collection of shared costs becomes your indirect cost pool.

Building Your Indirect Cost Pool

To assemble your indirect cost pool, you’ll need to do a deep dive into your chart of accounts. The goal is to flag every expense that isn’t tied directly to a specific project. It’s a common mistake for nonprofits to stop at the big-ticket items like rent and utilities, but that often means leaving money on the table.

To make sure your pool is comprehensive, look for these often-overlooked categories:

- Administrative Salaries: The slice of salaries for your Executive Director, finance team, HR, and development staff that supports the entire organization.

- Occupancy Costs: Don't just stop at rent. This bucket should also include utilities, property insurance, security monitoring, and general building maintenance.

- Professional Services: Remember to include the fees for your annual audit, general legal advice, and bookkeeping services that aren't grant-specific.

- Technology and IT Support: Think shared software subscriptions, internet service, IT helpdesk contracts, and the depreciation on servers, laptops, and printers.

- Insurance: Your general liability, workers' compensation, and Directors & Officers (D&O) policies are classic examples of indirect costs.

- Professional Development: Any training that benefits staff across different departments or builds the overall capacity of your organization fits here.

As you categorize these expenses, keeping an eye on potential small business tax deductions can be a smart move for your overall financial strategy, since many of these indirect costs can have tax implications.

Choosing Your Allocation Base

Once you've added up all your indirect costs, you need a fair and logical method for spreading them across your various programs. This method is your allocation base. The base you pick should have a direct, causal relationship with the overhead costs you've tallied.

At its core, the formula is simple: Total Indirect Costs ÷ Allocation Base = Indirect Cost Rate. You’re basically just choosing which direct costs will serve as the denominator in that equation. But this choice is a big deal—it will dramatically affect your final rate.

Key Takeaway: Think of the allocation base as the yardstick for assigning overhead. A program that’s "bigger" according to that yardstick will be responsible for a larger share of the organization's indirect costs.

For most nonprofits, the choice comes down to one of two common bases:

- Direct Salaries and Wages: This base is exactly what it sounds like—it only includes the direct labor costs for staff working on your projects. It’s wonderfully simple and easy to track.

- Modified Total Direct Costs (MTDC): This is the gold standard for federal grants. MTDC includes all your direct costs except for certain items that are specifically excluded. Common exclusions are equipment, capital expenses, patient care costs, and the portion of any subaward that exceeds $25,000.

How Your Choice of Base Changes Everything

Let's see this in action. Imagine a community arts nonprofit has an indirect cost pool of $150,000. Watch what happens to their rate when they switch their allocation base.

Just by changing the allocation base from Direct Salaries to MTDC, the calculated rate plummeted by almost 17%. This makes it crystal clear that selecting the right base for your organization isn't just an accounting exercise—it's a critical strategic decision.

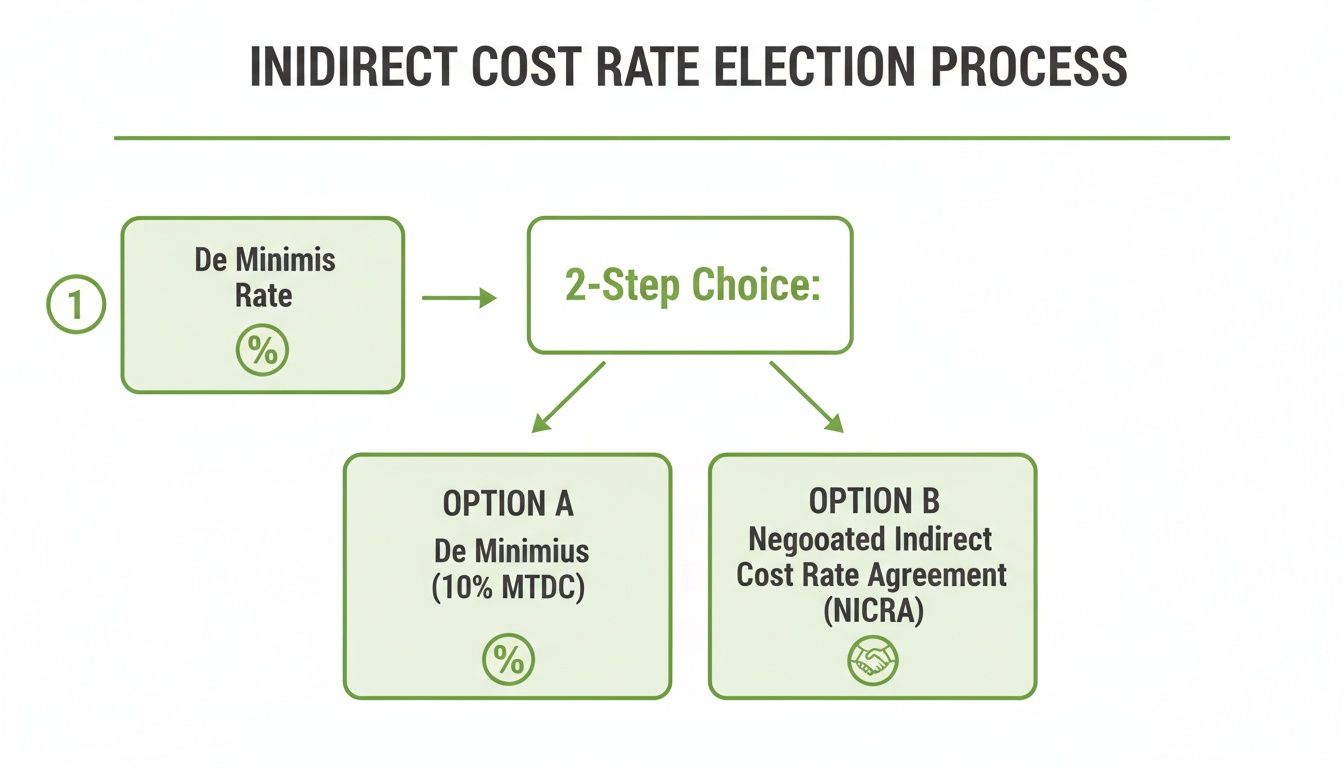

Choosing Your Path: The De Minimis Rate vs. a NICRA

After sorting your expenses into direct and indirect cost pools, you’ve hit a critical fork in the road. The decision you make here directly impacts how you recover the essential overhead costs that keep your nonprofit running. For any organization working with federal grants for nonprofits, the choice typically comes down to two main options: a simple, one-size-fits-all rate or a custom-tailored one.

This isn’t just a math problem; it’s a strategic decision. You're weighing your organization's time, resources, and long-term financial health. You can either go with the straightforward 10% de minimis rate or put in the work to establish a formal Negotiated Indirect Cost Rate Agreement (NICRA). Each has its place, and the right choice depends entirely on your specific situation.

Understanding the 10 Percent De Minimis Rate

Think of the de minimis rate as the "easy button" for indirect cost recovery. It’s a flat 10% rate that eligible organizations can apply to their Modified Total Direct Costs (MTDC). The real beauty of this option is its simplicity—you don't have to conduct a complex cost analysis or enter into a lengthy negotiation with a federal agency.

So, who gets to use it? Federal guidelines are clear: any organization that has never had a federally negotiated indirect cost rate can elect to use the de minimis rate. This makes it a fantastic starting point for:

- Small or new nonprofits just dipping their toes into the federal funding pool.

- Organizations with lean administrative teams that simply don't have the bandwidth for a complex negotiation.

- Nonprofits whose actual indirect costs are right around 10% anyway, making a full NICRA process feel like overkill.

The introduction of this rate was a game-changer for smaller organizations. The post-2014 Uniform Guidance made it much easier for thousands of smaller nonprofits to claim a fair share of their overhead. This led to a 40% increase in cost recovery for many who had previously been forced to claim nothing at all.

But its simplicity is also its biggest weakness. If your actual indirect costs are 15%, 25%, or even higher, sticking with the 10% de minimis rate means you are knowingly leaving money on the table with every single grant.

When to Pursue a Negotiated Rate (NICRA)

A NICRA is a formal, binding agreement between your nonprofit and a "cognizant" federal agency (usually the one that provides the most funding to you). The process involves putting together a detailed proposal breaking down your cost pools and allocation base. The agency then reviews, audits, and negotiates with you to land on an official, unique rate for your organization.

Yes, this path demands a significant upfront investment of time and meticulous record-keeping. But the payoff can be massive. A NICRA lets you recover the actual cost of your overhead, which for many established organizations is significantly higher than the 10% de minimis cap.

A NICRA is more than just a number; it's an official validation of your organization's true operational costs. It provides a defensible, government-approved rate that you can use with confidence across all your federal grant proposals.

Going after a NICRA is the right strategic move if your nonprofit:

- Receives a large volume of federal funding or has ambitious plans to scale its federal grant portfolio.

- Consistently sees its true indirect costs running well above the 10% threshold.

- Has the financial and administrative staff in place to manage the detailed proposal and negotiation.

The NICRA process shifts your whole approach. You're no longer just accepting a standard rate; you're making a data-backed case for what it truly costs to run your programs well.

Making the Right Choice for Your Organization

Choosing between these two paths comes down to an honest look at where your nonprofit is today and where you want to be tomorrow. Don't just default to the de minimis rate because it seems easier. Run a quick, back-of-the-napkin calculation of your actual indirect rate. If the number you see is 18%, you have a powerful financial incentive to invest in the NICRA process. On the other hand, if your rate is 9%, the de minimis rate is a perfectly logical and efficient choice.

To help you visualize the decision, here’s a quick comparison of the two approaches.

De Minimis Rate vs. NICRA: Which Is Right for You?

This table breaks down the key differences to help you decide which path aligns best with your organization's capacity and financial strategy.

Ultimately, the goal is to choose the method that ensures your organization’s financial health and sustainability without creating an undue administrative burden.

Calculating Your Indirect Cost Rate: A Worked Example

Theory is one thing, but rolling up your sleeves and crunching the numbers is where it all clicks. Let's walk through the process together using a fictional nonprofit, the "Community Wellness Center" (CWC), to see how this plays out in the real world.

This hands-on example will cut through the jargon and show you exactly how the formula works, giving you a clear model to adapt for your own organization.

Setting the Scene: The Community Wellness Center

Imagine the Community Wellness Center is a 501(c)(3) with an annual budget of roughly $1.25 million. They’re running several fantastic grant-funded programs: a mobile health clinic, nutrition workshops, and mental health counseling.

To get a handle on their true costs, their finance director needs to dig into the annual expenses and sort everything into two buckets: the indirect cost pool and the direct cost base.

First, Tallying the Indirect Cost Pool

The indirect cost pool is simply the total of all those shared expenses that keep the lights on and the organization running—things that can't be pinned to a single program. After a careful review of their general ledger, CWC’s team comes up with this list of annual indirect costs:

- Administrative Salaries & Benefits: The slice of salaries for the Executive Director, Finance Manager, and Office Admin comes out to $120,000.

- Occupancy Costs: Rent and utilities for their main office space total $65,000 for the year.

- Professional Services: This covers their annual audit and general legal fees, which are $15,000.

- Insurance: General liability and D&O policies add up to $10,000.

- Office Supplies & Technology: Shared costs for things like computers, software licenses, internet, and paper are $22,000.

- Other Miscellaneous Overhead: Catch-all items like bank fees and general marketing materials total $18,000.

Add it all up, and the Community Wellness Center has a total Indirect Cost Pool of $250,000. As you do this for your own nonprofit, don't forget that items like equipment depreciation can be a key part of this calculation. You'll often need to know how to calculate depreciation for assets used across the organization.

Next, Determining the Direct Cost Base

Now, the team needs to identify all the costs that are directly tied to delivering their specific, grant-funded programs. This becomes their allocation base. For simplicity, CWC has decided to use a Direct Salaries and Wages base for their calculation.

Here are their direct program costs for the year:

- Program Staff Salaries & Benefits: The salaries for their clinic nurses, nutritionists, and counselors total $750,000.

- Direct Program Supplies: This includes medical supplies for the mobile clinic and educational materials for workshops, costing $150,000.

- Program-Specific Travel: Mileage reimbursement for the mobile clinic staff comes to $50,000.

- Consultants: They hired a data analyst for a specific grant, which was a $50,000 contract.

Since CWC chose Direct Salaries and Wages as their base, they will only use that specific figure from the list above. This gives them a Direct Cost Base of $750,000.

Applying the Indirect Cost Rate Formula

This is where the magic happens. The math is actually pretty simple.

The formula is:

Indirect Cost Pool / Direct Cost Base = Indirect Cost Rate

Plugging in CWC's numbers:

$250,000 / $750,000 = 0.3333

Voila! The Community Wellness Center has an indirect cost rate of 33.3%.

This is the point where a nonprofit has to make a choice: stick with the simple 10% de minimis rate or go through the process of establishing a formal, negotiated rate based on these real numbers.

As you can see, the de minimis rate is a straightforward, no-questions-asked option. But for an organization like CWC with a calculated rate of 33.3%, negotiating a formal rate (a NICRA) is the only way to recover their true overhead costs.

Putting the Rate into Action on a Grant Proposal

Armed with their new 33.3% rate, CWC can build much more realistic grant budgets. Let's say they're applying for a new $150,000 grant. They've mapped out the direct project costs as:

- Direct Salaries: $100,000

- Direct Supplies: $15,000

- Total Direct Costs: $115,000

To figure out the indirect costs for this specific grant, they apply their rate to the grant's direct salary base:

$100,000 (Direct Salaries) x 33.3% = $33,300 (Indirect Costs)

The Full Grant Budget Picture:

- Total Direct Costs: $115,000

- Total Indirect Costs: $33,300

- Total Grant Request: $148,300

This calculation ensures their proposal asks for what they truly need—not just the money to run the program, but a fair share of the essential administrative support that makes the work possible. If you need help structuring this, our comprehensive https://www.fundsprout.ai/resources/grant-budget-template can be a lifesaver.

How to Document and Defend Your Rate to Funders

You’ve done the hard work of calculating your indirect cost rate. That’s a major step, but you're not quite at the finish line. The next challenge is presenting that number to funders in a way that tells a story of your organization's stability and effectiveness.

This is where your documentation becomes your best friend. Funders, especially government agencies, won't just take your rate at face value. They need to see the receipts, literally. A well-organized package of supporting documents anticipates their questions and proves your rate is grounded in solid financial reality, not just wishful thinking.

Building Your Evidence File

I always tell clients to create a dedicated binder—whether it's a physical one or a folder on a shared drive—that holds every single piece of evidence behind your calculation. When a program officer eventually asks for backup, you won't be scrambling. You'll have the answer right there.

Your evidence file should, at a minimum, include these essentials:

- Audited Financial Statements: Your most recent audit is the bedrock of your calculation. It’s a third-party-validated snapshot of your total expenses.

- Detailed General Ledger: This is where you show your work. It lets a reviewer trace exactly how you classified every expense as either direct or indirect.

- Written Cost Allocation Policy: A formal, board-approved policy is non-negotiable. It defines how you separate direct from indirect costs and proves your methodology is consistent and intentional.

- Payroll Records and Time Studies: For staff whose time is split—like an Executive Director who also manages a specific program—you absolutely need timesheets or personnel activity reports (PARs) to justify how you allocated their salary.

Getting these documents in order isn't just about passing an audit. It signals to funders that you have a strong culture of financial transparency, which builds tremendous trust.

Weaving Your Rate into the Grant Narrative

The budget justification section of your grant proposal is where you bring the numbers to life. Don't just list your indirect cost rate as a line item and move on. You have to connect the dots for the funder, showing them what their investment in your "overhead" actually buys.

Instead of a line that just says "Indirect Costs (25%)," you need a narrative that frames it as essential for success.

A Quick Tip from the Field: Stop using the word "overhead." Instead, try "shared mission support" or "core operational support." This simple language shift changes the conversation from administrative burden to the foundational infrastructure that makes your direct services possible. Funders start seeing these costs as an investment in your impact, not just a tax on their grant.

Here’s some sample language you can adapt for your own proposals:

- For a NICRA: "Our federally negotiated indirect cost rate of 25% (NICRA dated 1/1/2024) covers essential administrative and facility costs that provide a stable foundation for this program. This includes a proportional share of our financial management, HR, and IT infrastructure, which ensures strong compliance and operational excellence."

- For the De Minimis Rate: "We have elected to use the 10% de minimis indirect cost rate, which allows us to recover a portion of the vital operational support—like rent, utilities, and administrative oversight—that makes this project possible."

This kind of narrative answers the "What are we actually paying for?" question before it's even asked. It reassures the funder that their money is going to a well-run, stable organization that can deliver on its promises.

Remember, strong documentation is a core part of effective financial oversight. You can learn more about this in our comprehensive guide to grant management best practices.

When you combine rock-solid documentation with a compelling story, your indirect cost rate is no longer just a number. It becomes a powerful statement about your organization's value and long-term sustainability.

Answering Your Toughest Questions About Indirect Costs

Even with a solid process, a few tricky questions always seem to pop up when calculating indirect costs. Nonprofits often get stuck on the same handful of issues, especially when trying to balance internal realities with a funder's specific rules. Let’s tackle some of the most common questions I hear from grant teams out in the field.

Think of this as your go-to guide for those gray areas. The goal here is to give you clear, practical answers so you can navigate these hurdles and apply your rate with confidence.

Can We Include Fundraising Costs in Our Indirect Cost Pool?

This question comes up all the time, and getting it right is crucial for compliance. The short answer for federal grants is almost always no.

Under Uniform Guidance (2 CFR 200), fundraising costs are generally considered unallowable. The government’s logic is that these expenses support your organization's overall existence, not the direct work of a specific federally funded project.

However, the game can change with private foundations. Some will allow you to include a portion of fundraising or development costs, but you have to make a strong case for how those activities directly benefit the program they're funding. Always, always check the funder's guidelines. Never assume.

When you're putting together a Negotiated Indirect Cost Rate Agreement (NICRA) for a federal agency, the safest bet is to exclude all fundraising costs from your pool. It’s a huge red flag in an audit and can put your entire rate proposal at risk.

This is a perfect example of why careful cost allocation is so critical. What one funder allows, another will flat-out deny.

How Often Should We Recalculate Our Indirect Cost Rate?

Your indirect cost rate isn't a "set it and forget it" figure. It’s a living number that needs to reflect what's actually happening in your organization.

Best practice is to recalculate your rate every single year. Think about it—your expenses are always in flux. Rent goes up, salaries get adjusted, you add new software subscriptions, and program priorities shift. An annual calculation keeps your rate accurate, defensible, and real.

If you have a formal NICRA, you’ll be on a required schedule to resubmit your proposal anyway, usually every one to four years. But even if you’re just using the 10% de minimis rate, doing an internal review of your actual costs each year is just smart financial management. It helps you see if that 10% is still cutting it or if it’s time to start the process of negotiating a formal rate.

What’s the Real Difference Between MTDC and TDC?

Getting this right is absolutely essential if you're managing federal grants. The acronyms look similar, but they produce wildly different budget outcomes.

- Total Direct Costs (TDC): This is the simple one. Your indirect rate gets applied to the entire sum of your direct project costs. No exceptions, no exclusions.

- Modified Total Direct Costs (MTDC): This is the base that federal agencies almost always require. MTDC is a more nuanced calculation. You start with your total direct costs and then back out certain big-ticket or distorting expenses.

What gets excluded from the MTDC base? It's usually things like:

- Equipment purchases

- Capital expenditures

- Patient care costs

- Rental costs and tuition remission

- The portion of any single subaward over $25,000

Since MTDC carves out these major expenses, it results in a smaller base for the rate to be applied to, which means less indirect cost recovery. Your funder’s guidelines will always tell you which base to use. Using the wrong one is a classic—and costly—mistake that auditors find all the time.

What If a Funder Caps Indirect Costs Below Our Actual Rate?

Welcome to one of the most frustrating realities in grant funding. This happens all the time, especially with private foundations and some state grants. Many funders will impose their own cap—often 10%, 12%, or 15%—no matter what your meticulously calculated, federally-approved rate actually is.

So, what do you do? Let's say your NICRA is 25%, but a foundation will only pay 15%. That leaves a 10% gap that the grant won't cover. You've got a few options for managing that shortfall.

- Try to Educate the Funder. Don't be afraid to share a summary of your NICRA or a one-pager on how you calculated your rate. Sometimes, this can open a conversation. It shows them your request is based on real data, not just a number you picked out of thin air.

- Rethink Your Direct Costs. Scour your budget. Are there any costs you classified as indirect that could be justifiably moved to the direct cost column for this specific project? For instance, maybe a portion of a program director's salary can be allocated as a direct cost if they're spending a significant amount of time directly overseeing that project's activities.

- Cover the Gap with Unrestricted Funds. This is often the unavoidable reality. You’ll have to cover the unrecovered indirect costs with your hard-earned unrestricted funds. This is a powerful reminder of why having a diverse funding strategy—with individual giving and other revenue—is so vital for supporting your core mission.

Ultimately, a funder's cap forces you into a strategic decision. You have to look at the numbers with clear eyes and ask: can we truly afford to take on this grant and absorb the costs it won’t cover?

At Fundsprout, we believe that securing the full cost of your mission shouldn't be a struggle. Our AI-powered platform helps your nonprofit find the right funders, craft proposals that make a powerful case for your full needs, and manage compliance with ease. Discover how you can stop leaving money on the table.

Try 14 days free

Get started with Fundsprout so you can focus on what really matters.