Mastering Nonprofit Annual Reporting Requirements 2026

Master your nonprofit's annual reporting requirements. Our 2026 guide simplifies IRS Form 990, funder, & state filings into a manageable system.

Abdifatah Ali

Co-Founder

Year-end reporting rarely fails because people don't care. It fails because the data lives in six places, the deadlines live in someone's inbox, and the story of the work never got documented while the work was happening.

If you're running a nonprofit, you've probably lived some version of this. Finance has the year-end numbers. Program staff have outcomes in a case management system, a spreadsheet, or their heads. Development needs a clean narrative for funders. The board wants a polished annual report. Then someone realizes one report is due on a fiscal-year basis, another wants calendar-year data, and a grantor wants a very specific template that doesn't match either.

That scramble isn't just stressful. It costs credibility, staff time, and decision quality. Teams end up recreating numbers, revising language under pressure, and making avoidable errors because there was never a single operating system for annual reporting requirements.

I've seen organizations make a major shift once they stop treating reporting as a last-quarter event. The fix isn't working harder in deadline season. It's building a repeatable system that runs all year. If you're also juggling grants, contracts, and partner obligations, a practical look at how AI helps track contract compliance is useful because the discipline is similar. You need one place to track obligations, dates, and evidence.

A good annual reporting process also has to account for overlap. The same program activity may feed a board report, a donor update, a grant renewal, and a compliance filing. That's why a centralized approach to managing multiple grant reporting requirements matters so much. When the underlying system is sound, each report becomes an output, not a fire drill.

Beyond the Deadline Dread

The most common mistake I see is simple. Teams wait until a due date gets close, then try to assemble a full-year record from whatever happens to be available.

That approach creates three predictable problems. First, numbers drift because different departments pull from different cut-off dates. Second, narratives get padded with activity descriptions because no one captured outcomes when they happened. Third, leadership ends up reviewing reports in a rush, which is when inconsistent language and missing disclosures slip through.

What the scramble really costs

The cost isn't only compliance risk. It also shows up in staff morale.

Program leaders get frustrated when they're asked to reconstruct details months later. Finance staff get stuck translating internal accounting categories into external reporting formats under tight deadlines. Executive directors become the final editors of everything because no one trusts the data flow enough to delegate with confidence.

Annual reporting requirements feel overwhelming when the real problem is workflow design, not effort.

I've watched small teams outperform larger ones because they used a steady rhythm. They logged reporting obligations early, assigned owners, documented source data, and reviewed changes before year-end. Their reports weren't easier because the rules were lighter. They were easier because the system was better.

A different frame

Annual reporting can do more than satisfy a regulator or funder. Done well, it becomes your cleanest record of financial stewardship, program execution, and mission progress.

That shift matters. When reporting is organized year-round, the annual cycle stops being a compliance burden and starts feeding fundraising, board communication, renewal strategy, and internal planning. The organizations that handle annual reporting requirements well don't rely on heroic effort. They rely on documented process.

The Five Pillars of Nonprofit Reporting

Most nonprofits don't have one annual reporting requirement. They have a stack of them, serving different audiences for different reasons. It helps to sort that stack into a manageable structure.

Financial statements

This pillar is the backbone. It tells readers what came in, what went out, what the organization holds, and how resources were used.

For some organizations, this is mostly about internal readiness and board oversight. For others, it's the foundation for state filings, grant reports, lending relationships, and annual public communications. If your financial statements are late, unclear, or disconnected from program reporting, every other pillar gets harder.

Annual filings and regulatory disclosures

These are the formal submissions that keep you compliant with federal, state, and local expectations. They may ask for financial information, governance details, operational data, or legal disclosures.

The purpose isn't storytelling. It's accountability and transparency to oversight bodies. That distinction matters because teams often make the mistake of drafting these filings like donor communications. Regulators want consistency, completeness, and supportable records.

Programmatic reports

Programmatic reporting answers a different question. Did the work happen, and what changed because of it?

Many nonprofits struggle because they collect activity logs but not decision-ready evidence. Running a workshop is an activity. Showing what participants gained, completed, or changed afterward is program reporting.

Donor and funder reporting

Supporters need confidence that funds were used as promised. Some want a concise narrative with a few key metrics. Others want a line-by-line response to a grant agreement.

This pillar is where reporting quality directly affects renewal probability and relationship strength. Teams that keep reusable program summaries, approved financial descriptions, and source-backed metrics save enormous time here.

Governance and compliance updates

This last pillar gets ignored until it creates a problem. Board minutes, policy reviews, internal approvals, conflict disclosures, and documented changes in operations often sit outside the reporting conversation until someone asks for them.

Practical rule: If a report depends on a board approval, policy status, or organizational change log, treat that documentation as part of annual reporting requirements, not as a separate administrative task.

These five pillars don't operate in isolation. They share data, but they don't share the same audience or format. That's why a strong reporting system has one source of truth underneath multiple report types above it.

Decoding What Each Report Actually Requires

The phrase annual reporting requirements sounds tidy. In practice, each report asks for a different mix of numbers, narrative, certifications, and supporting documentation. If you don't separate those demands clearly, teams start reusing the wrong material in the wrong place.

Same organization, different reporting logic

A board packet, a grant report, a state filing, and a public annual report may all describe the same year. They still shouldn't be written the same way.

Financial audiences need clean statements and notes. Funders often want restricted-use explanations, milestone status, and program outcomes. Government filings may require prescribed forms, exact labels, and formal disclosures. The fastest way to create trouble is to assume one polished narrative can be copied everywhere.

For nonprofits trying to tighten the finance side of this work, a practical reference on accounting for grants helps because grant accounting categories often drive what you can report confidently later.

Annual reporting requirements at a glance

| Report Type | Primary Audience | Core Purpose | Typical Deadline |

|---|---|---|---|

| Financial statements | Board, management, funders, regulators | Show income, expenses, assets, liabilities, and notes | Varies by governing body, funder, or jurisdiction |

| Federal and state annual filings | Government agencies | Maintain compliance through required disclosures | Set by the applicable filing authority |

| Grant and contract reports | Funders and contracting agencies | Show use of funds, activities, outcomes, and compliance | Set by grant agreement or contract terms |

| Audit or unaudited financial report package | Regulators, oversight agencies, boards, funders | Demonstrate financial reporting status and required disclosures | Depends on applicable rules |

| Mission or annual impact report | Donors, community, partners | Communicate accomplishments, stewardship, and future direction | Usually tied to the organization's annual communications cycle |

One overlooked requirement that lowers anxiety

Many smaller organizations assume compliance always requires a full audit. That's not always true.

Per Texas requirements for agencies not issuing stand-alone reports, an unaudited submission can still be compliant if the agency clearly marks "UNAUDITED" at the top of every page and includes the required transmittal language stating that no opinion has been expressed, as detailed in the Texas annual financial reporting requirements for agencies not issuing stand-alone reports. That is a useful reminder for nonprofits that "unaudited" and "non-compliant" are not the same thing.

Fear drives poor decisions. I've seen organizations delay filings while trying to secure an audit they didn't need for that submission. If the governing requirement allows an unaudited format with specific disclosure language, follow the rule exactly instead of guessing.

What strong teams document in advance

The organizations that report smoothly don't wait to "start the report." They collect the building blocks throughout the year:

- Source-controlled financial data: Approved reports tied to your accounting system, with clear cut-off dates.

- Program evidence: Attendance, service counts, completion records, case notes, and outcome summaries with definitions.

- Narrative proofs: Short written explanations of what changed, what didn't, and why.

- Approval records: Board votes, policy adoptions, budget approvals, and leadership sign-off dates.

- Submission artifacts: Final versions, confirmation receipts, and any correspondence about clarifications or extensions.

If you're trying to reduce manual handoffs, a good example of operational thinking is Odoo ERP for compliance workflows. Not because every nonprofit needs a full ERP, but because the underlying lesson is right. Compliance gets easier when documents, ownership, and process steps live in one controlled workflow instead of scattered files.

Navigating the Most Common Reporting Traps

Most reporting failures don't come from obscure rules. They come from assumptions that feel reasonable until a reviewer rejects the submission or asks questions your team can't answer cleanly.

The calendar-year trap

One of the most expensive assumptions is that your internal fiscal year will match external reporting requirements. It often doesn't.

The clearest example comes from HRSA. The 2024 UDS Manual requires health centers with fiscal years other than January 1 through December 31 to report on the calendar year, not the grant year or internal fiscal year, as stated in the 2024 UDS Manual from HRSA. That's the kind of requirement that catches teams off guard because their accounting, budgeting, and board cycles may all be organized differently.

When this mismatch isn't addressed early, staff end up reconciling data manually. Numbers need to be cut on different dates. Program totals may need to be rebuilt from case records. Finance and program staff may both be "right" while still reporting different figures because they used different periods.

If a funder or agency defines the reporting period differently from your internal books, your first job is reconciliation design, not report drafting.

Other traps that cause avoidable errors

The period mismatch is the biggest hidden trap, but it isn't the only one. A few more show up repeatedly.

- Inconsistent organization-wide counts: Staff counts, participant totals, sites served, or partner numbers change from report to report because no one locked a definition and source.

- Outputs presented as outcomes: Teams report activities completed, then imply impact without evidence that conditions changed.

- Unlogged program changes: Staff alter service delivery, staffing patterns, or timelines during the year but don't document the change until reporting season.

- Narrative drift: Different writers describe the same initiative differently across funders, public reports, and board materials.

Why documentation of change matters

Federal-style reporting often expects more than a happy-path summary. It expects you to account for changes, missed milestones, and mixed results.

That's one reason I push teams to maintain a change log all year. If staffing changed, a vendor failed, a site closed temporarily, or a program model was adjusted, capture it when it happens. Waiting until year-end turns a simple explanation into a reconstruction exercise.

A credible report doesn't pretend the year was neat. It shows that the organization tracked reality, responded, and can explain the record.

The nonprofits that avoid these traps don't necessarily have bigger teams. They have reporting definitions, reporting calendars, and evidence trails that are agreed on before the pressure rises.

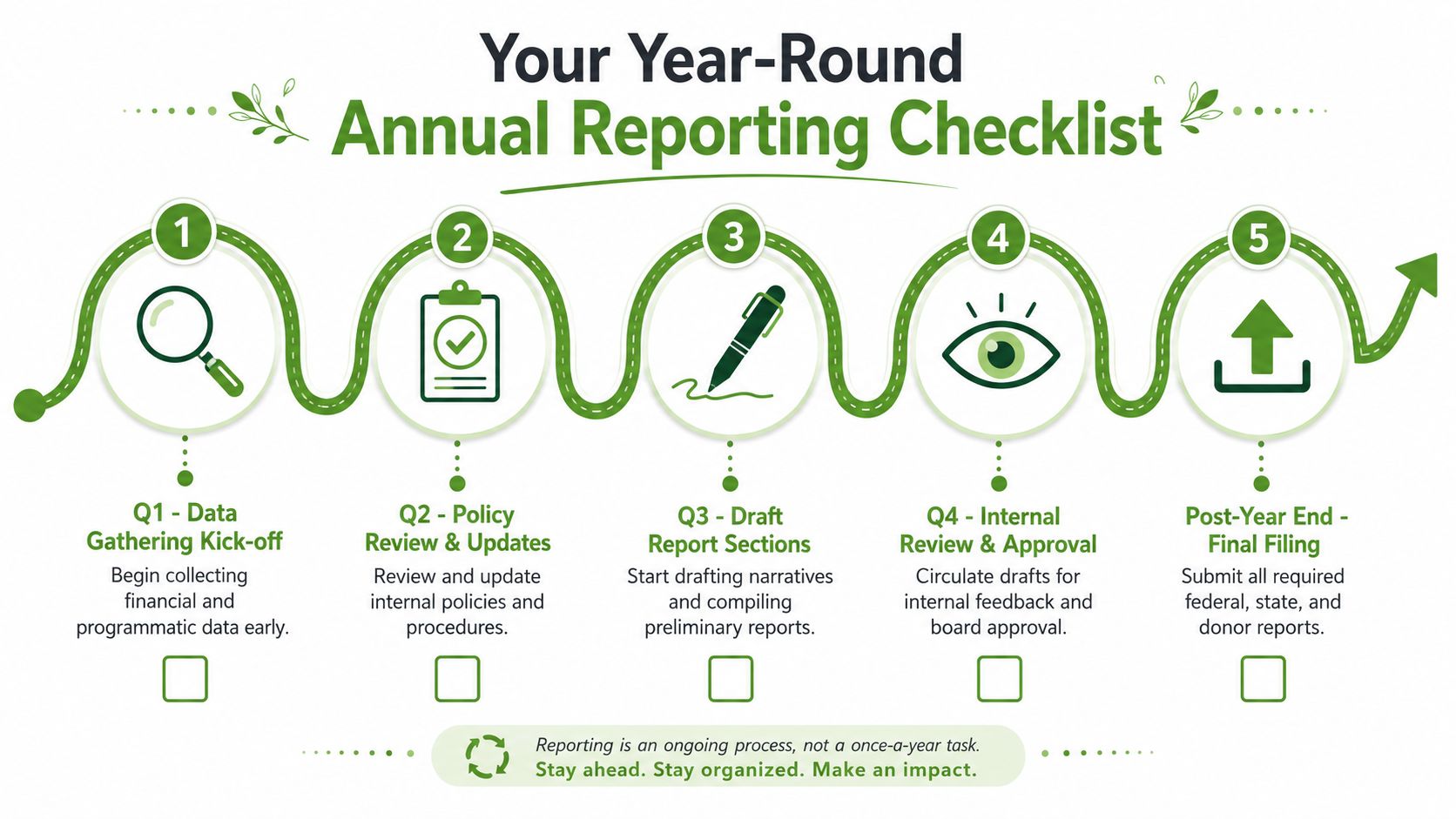

Your Year-Round Annual Reporting Checklist

Good reporting starts long before year-end. If you're still treating annual reporting requirements as a fourth-quarter project, the process will keep feeling heavier than it needs to.

This operating rhythm works well for most nonprofits because it spreads the load, reduces rework, and gives leadership time to review with a clear head. It also protects you from fixed statutory deadlines. For example, Washington requires local government annual reports to be submitted within 150 days after the close of each fiscal year, according to the Washington State reporting guidance. A deadline like that leaves very little room for cleanup if your records aren't already in order.

Q1 setup and ownership

The first quarter is where disciplined teams remove most later confusion.

- Map every reporting obligation: Build one master calendar that includes federal filings, state submissions, grant reports, donor commitments, and board approval dates.

- Assign one owner per report: One person should coordinate each report, even when several departments contribute.

- Lock data definitions: Agree on how you'll count participants, staff, sites, outputs, and outcomes.

- Create a document map: Identify where each required input will come from, including accounting exports, CRM fields, case management records, and board files.

If you're missing ownership at this stage, the same questions will keep resurfacing all year.

Q2 data quality and policy review

The middle of the year is the best time to catch structural issues because there's still time to fix them.

Use this window to compare finance and program records, review policy updates, and test whether grant restrictions and internal coding still align. If a team has changed how it delivers services, document the change now rather than trying to remember the sequence later.

A useful practice is a mid-year reporting review meeting with finance, development, program leadership, and operations in the same room. The agenda should be narrow: deadlines, data quality, changes in scope, and reporting risks.

Q3 narrative capture and evidence assembly

By the third quarter, start building report components, not just gathering raw inputs.

- Draft core narratives early: Write short summaries of each major program, including what was planned, what happened, and what changed.

- Collect support files: Save board-approved documents, budget revisions, signed amendments, and final versions of policy updates.

- Interview program staff: Capture outcome stories while details are still fresh and before turnover or memory loss gets in the way.

- Reconcile special reporting periods: If any submission uses a period that doesn't match your standard internal cycle, prepare that bridge now.

Field note: The best annual reports are usually assembled from monthly and quarterly records. The worst ones are reconstructed from memory.

Q4 review and submission readiness

The final quarter should be for review, formatting, and approval. It shouldn't be the first time anyone sees the core content.

Run a line-by-line review for consistency across numbers, terminology, and dates. Confirm that every narrative claim has support behind it. Check whether any report requires board approval, executive certification, or a specific file format.

Then create a submission packet for each report. Include the final file, supporting documents, sign-off record, and proof of submission. This small discipline saves real pain when an agency, auditor, or funder asks follow-up questions months later.

Streamlining Compliance with Smart Workflows

Manual reporting isn't just slow. It encourages inconsistency because every cycle starts from scratch. Teams rebuild timelines, hunt for old narratives, and re-check requirements they should already have organized.

A better model is to treat compliance as infrastructure. That means building one durable workflow for collecting data, storing evidence, drafting content, reviewing versions, and tracking submissions.

Build a single source of truth

Start with a central reporting library. It doesn't need to be fancy at first. It does need to be controlled.

That library should hold approved organizational descriptions, current leadership lists, core program summaries, standard financial language, reporting calendars, and final submitted versions. Add a metric dictionary so staff know exactly how each recurring number is defined and where it comes from.

Standardize what can be standardized

Not every report can be automated, but much more can be standardized than most nonprofits realize.

Create reusable narrative blocks for common questions. Maintain a change log for staffing, service model adjustments, and major operating events. Use templates for internal review so legal names, dates, and core descriptions don't drift from one submission to another.

The discipline used in formal government reporting is instructive here. U.S. Department of Defense annual research reports require a complete summary of accomplishments aligned with the approved statement of work, including both positive and negative findings, and they shift emphasis from activities to accomplishments as a project nears completion, as described in the DoD annual research reporting guidance. Nonprofits benefit from the same habit. Don't just log what staff did. Log what changed, what didn't, and what needs explanation.

Use tools to reduce handoffs

Software earns its keep. The right tool won't replace judgment, but it can remove repetitive coordination work.

- Deadline tracking: Systems can flag upcoming due dates and assign tasks before the rush begins.

- Template support: Teams can populate recurring fields from stored organizational data instead of retyping the same facts.

- Audit trail: Version history and submission records make follow-up much easier.

- Cross-team visibility: Finance, development, and program staff can see what is pending and what is final.

For organizations with public-facing or regulated workflows, tools built around public sector compliance tools show the value of role-based tracking and structured approvals. In the nonprofit grant world, grant compliance tracking software is useful for the same reason. It centralizes obligations, status, and supporting records instead of leaving each grant manager to maintain a separate private system.

One practical option in this category is Fundsprout. It supports funding and reporting workflows by tracking deadlines, organizing requirements, and helping teams populate report content from stored program and organizational information. That's not magic. It's process support. But process support is exactly what reduces deadline-season chaos.

Smart workflows don't make annual reporting requirements disappear. They make them visible early enough that your team can manage them calmly.

Turn Your Reporting Burden into a Strategic Asset

The nonprofits that handle annual reporting requirements well usually reach the same conclusion. Reporting is not separate from strategy. It is strategy, documented.

When your reporting system is sound, you stop arguing about which spreadsheet is right. You stop rebuilding the same narrative for every audience. You catch period mismatches before submission week. You know whether a report needs audited statements, an unaudited disclosure, a board action, or a special reporting period because that logic is already built into the workflow.

That changes how the organization operates. Compliance gets steadier. Funder communication gets sharper. Leadership gets a cleaner view of what the organization accomplished. Even setbacks become usable because they are documented clearly and explained credibly.

Good annual reporting doesn't come from better last-minute writing. It comes from year-round ownership, definitions, evidence, and review. Build that system once, and every future cycle gets easier to manage and more useful to the mission.

Your next report shouldn't begin when the deadline reminder arrives. It should begin with the next staff meeting, the next board approval, the next financial close, and the next program update that gets documented properly.

If your team wants a more organized way to manage funding pipelines, reporting deadlines, narrative drafts, and compliance records in one place, Fundsprout is built for that kind of year-round workflow. It helps nonprofits move from reactive reporting to a structured process that supports applications, renewals, and annual compliance without reinventing the system each cycle.

Try 14 days free

Get started with Fundsprout so you can focus on what really matters.