Mastering Accounting for Grants A Practical Nonprofit Guide

A practical guide to accounting for grants. Learn revenue recognition, expense tracking, and reporting to ensure nonprofit compliance and financial health.

Abdifatah Ali

Co-Founder

Grant accounting is how nonprofits record and report the money they receive from foundations, corporations, and government agencies. It's all about tracking funds, recognizing revenue at the right time, and making absolutely sure every dollar is spent according to the funder's rules. This isn't just about bookkeeping; it's the financial discipline that builds trust and keeps the funding pipeline open.

Why Getting Grant Accounting Right Is a Matter of Survival

Let's be real—the rules of grant accounting can feel like a maze. But in the crowded, competitive world of nonprofit funding, mastering it isn't optional. It’s a core survival skill. Strong grant accounting is what proves you're a responsible steward of funds, which is exactly what funders need to see.

When your financial records are flawless, you give donors the transparency they crave. You can draw a straight line from their investment to your impact in the community. That's how you turn a one-time grant into a long-term partnership.

Keeping Your Footing in a Shifting Funding Landscape

The ground is always moving under a nonprofit's feet. As government priorities shift, public funding can dry up. It’s a real challenge—a recent analysis showed 34% of nonprofits saw their federal grants shrink, while 29% experienced cuts from state and local governments.

This has created a mad dash for foundation grants. In fact, 87% of foundation leaders have seen a significant spike in applications as nonprofits scramble to fill those funding gaps.

With more competition comes more scrutiny. Foundations can afford to be picky. If an organization's grant financials are messy or unclear, it’s a huge red flag and an easy "no" for a grantmaker with a stack of proposals to review.

"Your financial reports are more than just a compliance task—they're a story about your impact and stewardship. Clean grant accounting is the foundation of that story."

The Core Principles You Can't Ignore

At its core, grant accounting follows the Generally Accepted Accounting Principles (GAAP), specifically a standard known as ASC 958-605. Think of it as the official rulebook that ensures everyone reports revenue the same way. Getting a handle on a few key concepts is essential for staying compliant.

- Conditional vs. Unconditional Grants: A grant is conditional if you have to overcome a specific hurdle to get the money, like securing matching funds. You can't record the revenue until you've met that condition. An unconditional grant has no strings like that, so you can usually recognize the revenue right away.

- Restricted vs. Unrestricted Funds: Restricted funds are earmarked by the donor for a specific purpose, project, or time frame. Unrestricted funds give you flexibility. Your accounting system absolutely must track these two types of funds separately to avoid accidentally misusing money.

Getting these distinctions wrong can lead to painful audit findings, financial restatements, and a serious blow to funder confidence. When you apply these principles correctly, you paint a clear and accurate picture of your organization's financial health. Building strong internal controls is a huge part of this, as we cover in our guide on grant management best practices. This foundational knowledge is your map for navigating a tough funding environment.

When do you actually count grant money as income? This is probably the most critical question in grant accounting, and the answer directly impacts the accuracy of your financial story. Getting the timing right isn't just a technicality—it’s the cornerstone of compliance and transparent reporting.

The biggest mistake I see is booking revenue the moment a check arrives. The reality is, the timing depends entirely on the strings attached to the grant. Specifically, we need to look at whether a grant is conditional or has donor-imposed restrictions. These two concepts drive the entire accounting process.

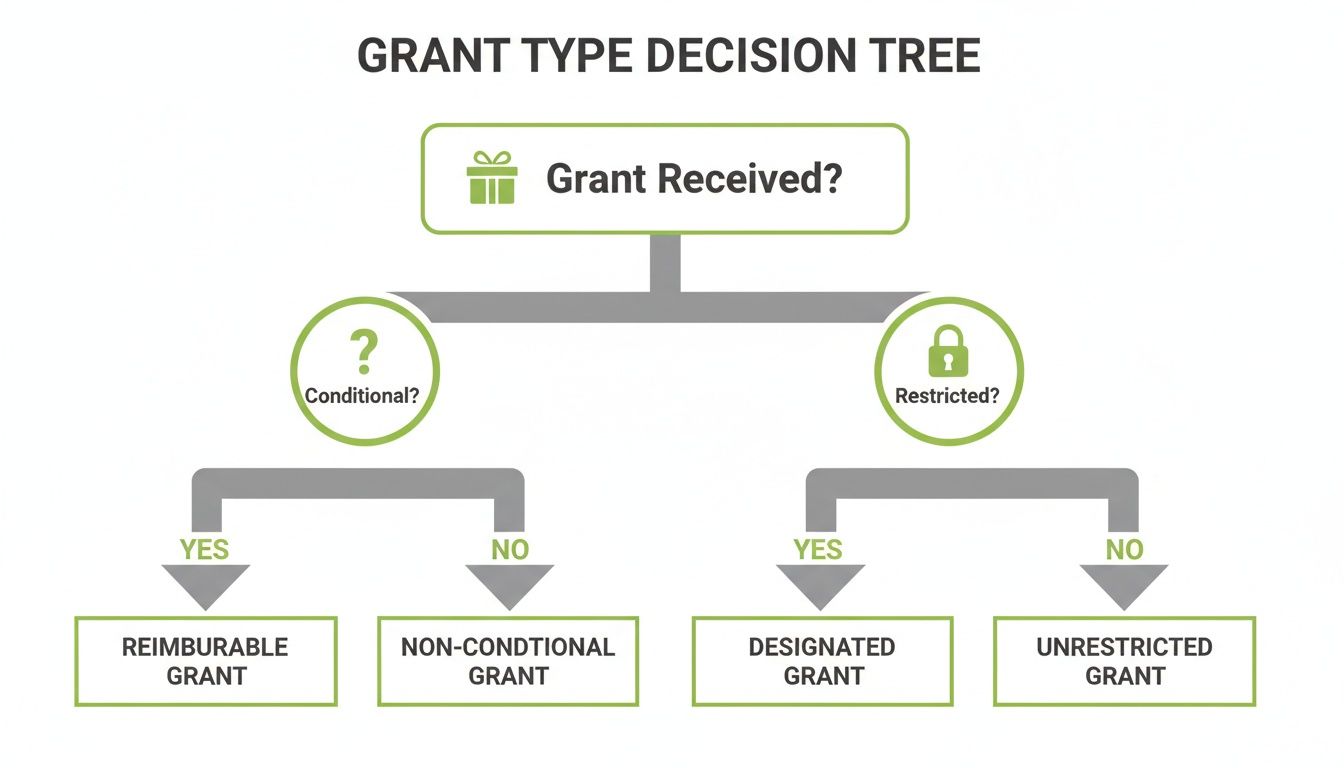

The Critical Difference: Conditions vs. Restrictions

A condition is a major hurdle you have to clear before you're truly entitled to the funds. Think of it as a barrier that, if you fail to overcome it, gives the funder the right to ask for their money back. Until that condition is met, the grant money isn't yours to claim as revenue.

A donor restriction, on the other hand, just dictates how or when the funds must be used. For example, a grant might be restricted to a specific summer literacy program or for buying a new van. The money is definitely yours, but you have to honor the donor’s wishes.

This decision tree is a great visual for the first questions to ask when a grant award letter hits your desk. It’s your roadmap to the correct accounting treatment.

As you can see, figuring out if a condition exists is always step one. It's the factor that most directly impacts when you can recognize the revenue.

Unconditional Grants: The Simpler Path

Let's start with the most straightforward scenario: an unconditional grant. This is a gift where the funder hasn't put up any significant barriers you have to meet to earn the money.

- Unrestricted Unconditional Grant: This is the dream scenario. A funder gives you $25,000 for general operating support with no strings attached. You can recognize the full $25,000 as revenue the moment the grant is awarded.

- Restricted Unconditional Grant: A funder gives you $25,000 specifically for your after-school tutoring program. There are no other conditions. You still recognize the full $25,000 as revenue immediately, but you’ll classify it on your books as "Revenue with Donor Restrictions."

When the cash comes in for either of these, your journal entry is a simple debit to Cash and a credit to Grant Revenue (either with or without donor restrictions).

The core principle is simple: If the grant is unconditional, you recognize the revenue when the promise is made. A restriction just changes the classification of that revenue, not the timing.

Conditional Grants: The Deferred Revenue Rule

This is where grant accounting gets tricky. With conditional grants, you absolutely cannot recognize revenue until you've met the specific condition spelled out in the grant agreement. Until then, any cash you receive sits on your balance sheet as a liability—usually called Deferred Revenue or Refundable Advance.

Your approach to recognizing revenue will also be shaped by your overall accounting method. It's crucial for any nonprofit leader to have a solid handle on understanding the difference between cash basis and accrual accounting.

Here are a few classic examples of conditions:

- A Matching Requirement: A foundation awards you a $50,000 grant, but only if you raise another $50,000 from other donors. You can't recognize any of the foundation's grant revenue until you've actually secured those matching funds.

- Cost-Reimbursement: A government agency agrees to reimburse your organization for specific, eligible program expenses. You only "earn" the revenue as you incur and document those costs.

- A Specific Outcome: A funder provides $100,000 on the condition that you successfully serve 500 meals to seniors in a specific quarter. You can only recognize the revenue after you’ve met that performance target.

Under U.S. GAAP, specifically FASB ASC 958-605, revenue from contributions is recognized only when they are unconditional. For conditional grants, this means you wait.

Let’s walk through a common cost-reimbursement scenario. Imagine you receive a $20,000 advance on a government grant that reimburses your program staff's salaries.

Initial Journal Entry (When you get the cash):

- Debit: Cash $20,000

- Credit: Deferred Revenue $20,000

In the first month, you incur and pay $5,000 in eligible salaries. You have now officially met the condition for that portion of the grant.

Monthly Journal Entry (To recognize the earned revenue):

- Debit: Deferred Revenue $5,000

- Credit: Grant Revenue $5,000

You repeat this process each month as you incur more eligible expenses, moving money from the liability account (Deferred Revenue) to an income account (Grant Revenue). This method is essential for making sure your financial statements accurately reflect the revenue you have truly earned.

Grant Revenue Recognition Scenarios

To make this even clearer, here’s a quick-reference table that breaks down how to handle different grant situations.

This table covers the most common scenarios you'll encounter. Always refer back to your specific grant agreement, as that is the ultimate source of truth for determining the proper accounting treatment.

Getting a Handle on Grant Expenses: Tracking and Allocation

Winning a grant is a fantastic moment, but for the finance team, it's just the starting line. Now comes the real test: proving your organization's stewardship by diligently tracking every single dollar. This isn't just about bookkeeping; it's about creating an airtight audit trail that links every expense back to the grant's intended purpose.

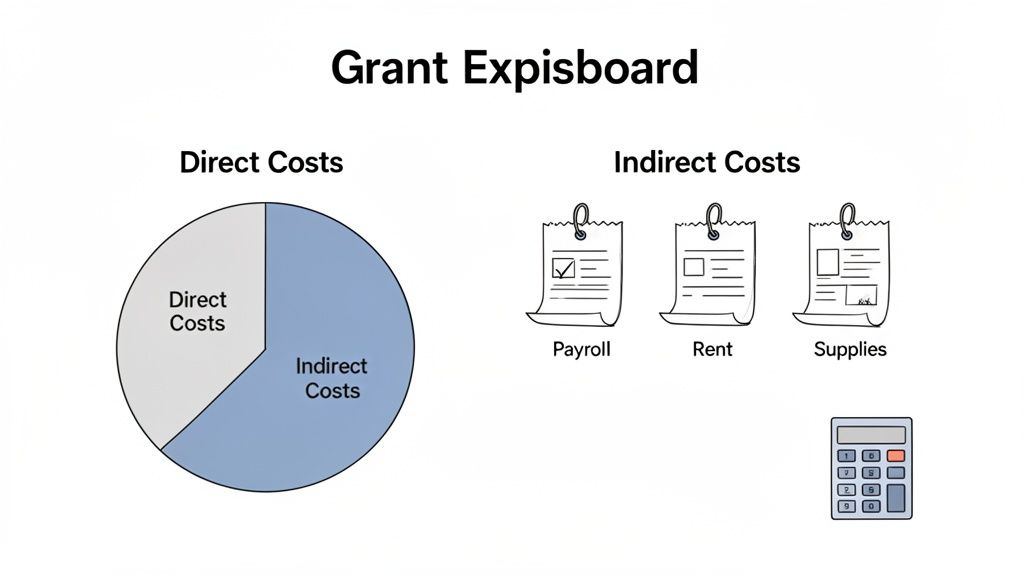

The first and most critical task is to properly categorize every cost you incur. Every single expense needs to be sorted into one of two buckets: direct costs or indirect costs. Getting this distinction right is absolutely non-negotiable for accurate financial reports and, most importantly, getting reimbursed by your funder.

Separating Direct and Indirect Grant Costs

So, what's the difference? Think of direct costs as anything you can point to and say, "We only paid for this because of Grant X." These are expenses tied specifically and exclusively to a single grant-funded project.

If you’re running an after-school tutoring program, the salaries for the tutors working only on that program are a classic direct cost.

Here are a few common examples:

- Program Staff Salaries: The slice of a team member's salary that's dedicated to a specific grant's activities.

- Program Supplies: Workbooks, art supplies, or any materials bought just for that grant project.

- Project-Specific Travel: Mileage or a plane ticket for a staff member to attend a conference that was a requirement of the grant agreement.

On the other hand, indirect costs (often called overhead or administrative expenses) are the shared costs that keep the lights on for the whole organization. They aren't tied to any single grant but are essential for all of them to function. This is your office rent, the executive director's salary, or your accounting software subscription.

My rule of thumb: If the cost would disappear if the grant went away, it's probably direct. If the cost supports multiple programs or the organization as a whole, it's indirect.

Developing a Compliant Indirect Cost Rate

You can’t just assign the entire electric bill to one grant—that wouldn't be fair or compliant. Instead, you have to allocate it across all your programs. The tool for this is your indirect cost rate, a percentage you apply to your direct costs to figure out how much overhead each grant should chip in for.

This is especially critical for government grants, which can make up around 30% of a nonprofit's revenue. They demand precision, and a misstep in how you allocate costs can lead to funders clawing back money you’ve already spent.

You generally have two paths for establishing this rate:

- The De Minimis Rate: This is the simple option. For federal grants, if your organization has never had a formally negotiated rate, you can choose to use a flat 10% de minimis rate. This is calculated against your modified total direct costs (MTDC) and saves you a ton of paperwork.

- Negotiated Indirect Cost Rate Agreement (NICRA): If your actual overhead is much higher than 10%, it's worth going through the process of negotiating a formal rate with your federal cognizant agency. It’s more work upfront but ensures you recover a much more accurate share of your real operating costs.

How This Works in the Real World

Let's walk through a couple of common scenarios I see all the time.

Imagine a program director who splits her time across three different grants. Based on her timesheets, she spends her time like this:

- Grant A (After-School Program): 50% of her time

- Grant B (Summer Camp): 30% of her time

- Grant C (Community Outreach): 20% of her time

If her salary is $80,000, you would allocate it across the grants based on that documented effort. The math is straightforward: $40,000 gets charged to Grant A, $24,000 to Grant B, and $16,000 to Grant C. The key here is meticulous timesheets—they are your proof.

Another one that trips people up is in-kind contributions. Say a small arts organization has a grant that requires a $5,000 match. A skilled volunteer graphic designer donates 100 hours of her time, which you’ve valued at $50/hour. That $5,000 in donated service can be documented and used to meet the match requirement. Just be sure you have solid documentation, like a log of the hours worked and a clear basis for the valuation.

The secret to managing all this without pulling your hair out is setting up your financial system correctly from day one. Using a comprehensive grant budget template to build your budget helps you think through these details from the start. A good setup turns tracking and reporting into a simple, repeatable process instead of a forensic accounting project when the grant report is due.

Preparing Reports That Build Funder Trust

Your financial reports are so much more than a box to check. I've learned they're one of the most powerful tools you have for building a strong, lasting relationship with your funders. They tell the story of your impact, your stewardship of their investment, and the overall reliability of your organization.

Think of it this way: every report is an opportunity to prove they made the right choice in funding you. When you deliver clear, accurate, and timely reports, you're not just fulfilling an obligation—you're reinforcing their trust and making it incredibly easy for them to say "yes" to your next request.

What Goes Into a Solid Grant Report?

While every foundation has its own format, most financial reports for grants boil down to the same core pieces. Once you get these down, you can handle just about any request they throw at you.

- Budget vs. Actuals: This is the main event. It’s a straightforward comparison showing your approved grant budget right next to what you actually spent during the reporting period. No surprises here.

- A Narrative for Any Variances: Numbers on a page rarely tell the full story. If you spent 15% less on travel because a conference went virtual, or 20% more on supplies due to an unexpected price hike, you need to explain that. This context is what turns a list of numbers into a transparent conversation.

- The Paper Trail (Supporting Docs): This is where you back it all up. We're talking copies of invoices, key receipts, staff timesheets, and bank statements that verify the figures in your report.

Getting these reports right is fundamental to keeping funders happy. While the nonprofit world has its own quirks, many of the core principles overlap with the for-profit sector. If you want a broader view on financial statements, you might find some useful nuggets in a comprehensive financial reporting guide designed for small businesses.

Why a Rock-Solid Audit Trail is Your Best Friend

Want to know the secret to a stress-free audit or funder review? A meticulously organized documentation system. An "audit trail" is simply the path of paperwork that lets anyone—from your program officer to an external auditor—trace a transaction from its beginning to its end. A clean trail leaves no room for doubt.

Your goal should be to pull every single document related to a specific grant at a moment's notice.

A clean audit trail is your best defense against compliance issues. It proves not only what you spent, but also that you followed every procedure and policy required by the grant agreement.

Imagine a program officer calls to ask about a $5,000 expense you coded to their grant. With a great system, you can immediately pull up the approved budget line item, the vendor's invoice, proof of payment, and the timesheet from the staff member who did the work. That level of organization doesn't just answer their question; it builds incredible confidence in your management.

The Pre-Audit Checklist: A Quick Pulse Check

Audits don't have to be terrifying. A little preparation turns a high-stakes event into a routine process. Even the smallest nonprofit can use this simple checklist to see how ready they are and catch any weak spots before an auditor shows up.

Financial Documentation Health Check

- Grant Agreements: Are all signed agreements and any amendments filed and easy to find?

- Expense Records: Could you quickly find the invoices and receipts for a random sample of 5-10 grant-funded expenses?

- Timesheets: For staff working on multiple grants, do you have detailed, signed timesheets that properly allocate their hours?

- Bank Reconciliations: Are your bank accounts reconciled every month? Are there any old, mysterious items hanging around?

- Financial Reports: Have all funder reports been sent in on time? Do you have copies saved?

Running through this checklist every quarter can save you from a world of frantic searching down the line. It helps shift your reporting from a reactive scramble to a proactive, manageable part of your work—strengthening both your organization and the funder relationships that make it all possible.

Using Technology for Smarter Grant Accounting

If you’re still trying to juggle grant accounting with a patchwork of spreadsheets, you know the pain. It’s not just tedious; it's a huge time-sink that pulls you away from your actual mission. Modern accounting technology isn't a "nice-to-have" anymore—it's an essential tool that saves hours, prevents messy errors, and helps keep your funders happy.

Moving from spreadsheets to a proper software platform is about more than just going digital. It’s about building a connected financial system where everything talks to each other. The right tool links your grant budget to your final expense report, tracking every single dollar without you having to manually re-enter data across five different files.

This kind of setup gives even the smallest nonprofit team the power to manage complicated grants like a large, fully-staffed organization. You get to spend less time on paperwork and more time delivering your programs.

Must-Have Features in Nonprofit Accounting Software

Here’s the thing: not all accounting software is built for the weird world of nonprofit grants. A generic business platform like QuickBooks Online (without modifications) just doesn't have the muscle for proper grant management.

You need a tool designed for nonprofits from the ground up. As you look at different options, here are the absolute non-negotiables:

- True Fund Accounting: This is the big one. The software must let you create separate "buckets" for each grant or project, automatically keeping your restricted and unrestricted funds from getting mixed up.

- Automated Grant Reporting: Imagine pulling a budget-vs-actual report for a specific grant in two clicks. That's what you should be looking for. The best systems can even populate reports in the exact format your funder requires.

- Expense and Revenue Allocation: Your software should make it simple to "tag" a single expense—like a staff member's salary—to multiple grants or programs. This is crucial for correctly allocating your indirect costs and personnel time.

Beyond the basics, think about integrations. Does it connect with your payroll system? Your donor CRM? When your systems share data seamlessly, you eliminate the risk of typos and get a much clearer picture of your organization’s financial health. To see what's out there, check out our guide to the best nonprofit grant management software.

How Technology Transforms Your Workflow

Let's make this real. Say you have a federal grant that requires you to track and report on staff time.

Without the right software, it's a manual nightmare. Your program manager has to chase down timesheets, pull out a calculator to figure out salary allocations for three different people, and then painstakingly type those numbers into the grant’s budget spreadsheet. One typo can throw everything off.

Now, picture it with an integrated system:

- Staff log their hours in a time-tracking module, simply selecting the federal grant's code from a dropdown menu.

- The accounting system, linked to payroll, automatically does the math. It calculates the precise salary and benefits cost for the hours worked on that grant.

- When the report is due, you just run a "Grant Expense Report." The software instantly pulls in the allocated salary data, plus any other tagged costs like travel or supplies, and generates the report for you.

The right technology doesn't just make your current process faster; it fundamentally changes what's possible. It provides real-time visibility into your grant spending, allowing you to make proactive budget adjustments and confidently answer any funder questions that arise.

This kind of automation transforms grant accounting from a dreaded chore into a strategic tool. It keeps you compliant, builds trust with funders through accurate and timely reports, and gives you back your most precious resource: time.

Common Questions About Grant Accounting

Even with a great system, grant accounting can get tricky. Out in the real world, nonprofit leaders and program staff bump into gray areas all the time. Let's walk through some of the most common challenges and how to handle them with confidence.

How Should We Handle Reimbursement Grants?

A reimbursement grant can be a real head-scratcher for cash flow. When you get one of these, you don’t recognize any revenue just because the award letter is signed. Everything hinges on you spending your own money first.

Here’s how it works: You have to incur and pay for the approved expenses out of your organization’s own bank account. Once you’ve spent the money, you pull together all the documentation—invoices, timesheets, receipts—and submit it to the funder. Only then, at the moment you submit that reimbursement request, can you actually recognize the revenue on your books. That's the point where you've met the condition and officially "earned" the income.

Your journal entry for this would debit Grants Receivable (an asset) and credit Grant Revenue (income). It's crucial to have enough cash on hand to float these expenses while you're waiting for the funder's check to arrive.

What Is the Difference Between a Restriction and a Condition?

This is probably one of the most critical distinctions you need to understand under the accounting standard ASC 958-605. Getting it right directly affects when you can recognize revenue.

A donor restriction tells you how or when you can use the money. For example, a grant might be restricted to funding a specific youth summer camp or for use only in the next fiscal year. You usually recognize the revenue as soon as the grant is awarded, but you classify it as "with donor restrictions."

A condition is a barrier you have to get over before you’re even entitled to the funds. Think of it as a hurdle. A classic example is a matching requirement—you can’t get the funder’s money until you raise your part of the match. If you don't meet the condition, the funder can demand their money back.

Revenue from a conditional grant is only recognized once you’ve fully satisfied the condition. A restriction simply directs how you use money that is already considered yours.

What Is the Best Way to Track Staff Time on Grants?

Hands down, detailed timesheets are the most reliable and audit-proof method for tracking staff time. For many government grants, this isn't just a good idea—it's a non-negotiable requirement.

Any staff member who splits their time between different grants, or between grant work and general admin duties, needs to log their hours for each specific activity. This should be a regular habit, done daily or at least weekly. This data is the only defensible way you can allocate their salary and benefit costs as direct expenses to the correct grants.

Many organizations use time-tracking software where employees can tag hours to specific grant codes or project names. It’s a huge help in cutting down on human error and spits out the exact reports you’ll need for invoicing your funder and for your annual audit.

Can We Use Funds from One Restricted Grant for Another?

No. Never. This is a major compliance violation and one of the quickest ways to torpedo a relationship with a funder.

Money from a restricted grant must be used exclusively for the purpose spelled out in that specific grant agreement. Using it for anything else—even as a temporary loan to cover a gap in another program—is a misuse of funds. This can lead to having to pay the grant back and can seriously tarnish your organization's reputation.

You have to treat each restricted grant like its own separate pot of money. Your accounting system should be configured to enforce this separation, making it impossible to commingle the funds. Strong internal controls are your best defense here.

Stop wrestling with spreadsheets and start building funder trust. Fundsprout is an AI-powered platform that helps you find grants, write winning proposals, and manage compliance with ease. See how you can streamline your entire grant lifecycle at https://www.fundsprout.ai.

Try 14 days free

Get started with Fundsprout so you can focus on what really matters.