What is a 990-t? A Quick Guide for Nonprofits

What is a 990-t? Learn its impact on UBTI and how nonprofits stay compliant and funded in 2026.

Abdifatah Ali

Co-Founder

As a nonprofit leader, you’re laser-focused on your mission. But what happens when your organization starts earning income from a side business, like renting out your facility or selling merchandise? That's where Form 990-T comes in.

Think of it this way: your standard Form 990 is your organization’s report card to the public and the IRS. The 990-T, on the other hand, is a specific tax bill for income earned from activities that aren't directly connected to your core charitable purpose.

What Is Form 990-T and Why It Matters

While your main Form 990 is an informational return, the 990-T is a true tax return. It’s the official form for reporting what the IRS calls Unrelated Business Taxable Income (UBTI). This is the income your nonprofit generates from activities that look and feel more like a commercial business than a charitable program.

Let's say your environmental nonprofit sells t-shirts with your logo to raise awareness. That's clearly related to your mission. But what if you started using your screen-printing equipment to print custom shirts for local for-profit businesses? That second income stream would likely be considered unrelated, triggering the need for a 990-T.

Leveling the Playing Field

So, why does the IRS care about your side gigs? The whole point of the 990-T is to ensure fairness. It prevents a nonprofit from having an unfair tax advantage when competing directly with a for-profit company that has to pay taxes on its earnings. It keeps the competition honest.

This isn't a new concept. The IRS introduced this requirement way back in 1950 to address this very issue. Officially called the Exempt Organization Business Income Tax Return, Form 990-T is required for any nonprofit with $1,000 or more in gross income from these unrelated activities.

Who Needs to Pay Attention?

Getting this right is a big deal. Overlooking your 990-T obligations can lead to some painful penalties and interest payments. Worse, it could trigger an audit and, in extreme cases, even put your coveted tax-exempt status at risk. On the flip side, handling it correctly shows donors and grantmakers you’re financially savvy and committed to compliance.

Here’s a quick gut check. Your organization probably needs to file a Form 990-T if you meet these three conditions:

- You have $1,000 or more in gross income from an activity that qualifies as a trade or business.

- You conduct this business activity on a regular basis.

- The business itself is not substantially related to carrying out your exempt purpose.

A clean compliance record, including any necessary 990-T filings, strengthens your financial narrative. It’s a key piece of the due diligence puzzle for funders, much like the details confirmed in your organization's IRS determination letter.

Quick Guide to Form 990-T Filing

To help you keep these key details straight, here is a quick-reference table.

This table provides a snapshot, but understanding the nuances is crucial for making the right call for your nonprofit.

How to Spot Unrelated Business Income in Your Day-to-Day Operations

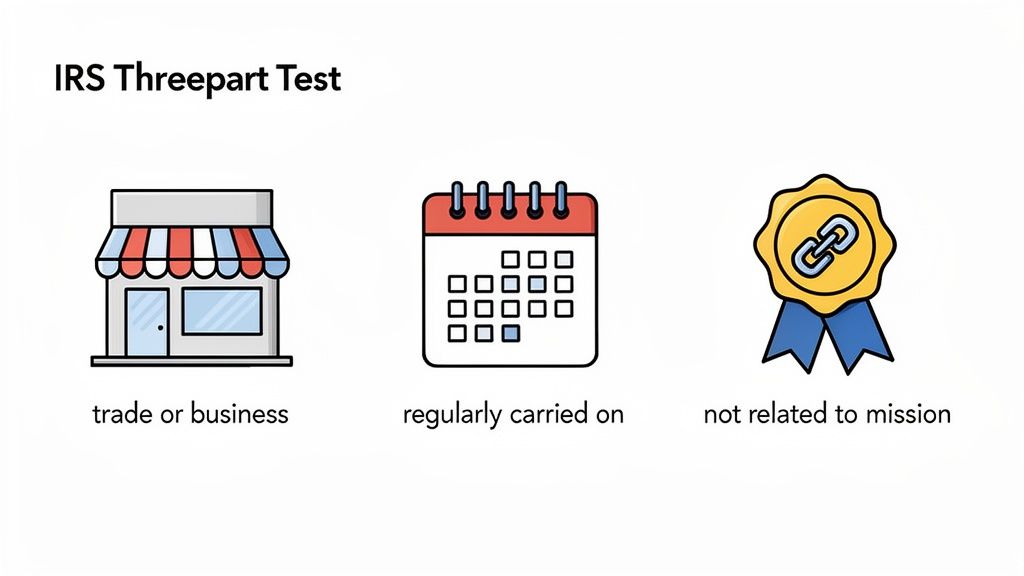

So, how can you tell if that new revenue-generating idea is actually Unrelated Business Taxable Income (UBTI)? It’s a common question, and thankfully, the IRS has a straightforward, three-part test to help you figure it out. If an activity checks all three boxes, the income is probably UBTI and needs to be reported on Form 990-T.

This is more common than you might think. A revealing study found that over 26% of nonprofits with assets of $1 million or more reported some kind of taxable business activity. For the charitable corporations in that study, the average taxable revenue hit $1,545,685—a clear sign that UBTI is a real consideration for many organizations with diverse income streams. You can dive deeper into these federal tax data findings on the American Accounting Association website.

The IRS Three-Part Test for UBTI

To determine if an activity creates UBTI, you have to run it through three specific filters. Think of it as a checklist. The activity must be a trade or business, be regularly carried on, and not be substantially related to your mission.

Let's unpack what each of those really means.

An activity is generally considered an unrelated business—and its income subject to tax—if it meets all three of these criteria:

- It is a trade or business.

- It is regularly carried on.

- It is not substantially related to your organization's exempt purpose.

It’s an all-or-nothing test. If an activity fails to meet even one of these conditions, the income it generates typically isn't considered UBTI.

1. It Is a Trade or Business

First, the activity must qualify as a trade or business. This is a pretty wide net. It covers almost any activity done with the goal of making money from selling goods or providing services. The key here is the intent to produce income, even if the venture ends up losing money.

For example, imagine your animal shelter decides to sell branded coffee mugs in an online store. That's a trade or business. The primary purpose is to earn money from a product sale.

2. It Is Regularly Carried On

Next, the activity has to be regularly carried on. This test is all about frequency and continuity. The IRS will compare your activity to how a similar for-profit business would operate.

If you run a gift shop that's open all year, that’s clearly regular. On the other hand, holding a one-off bake sale to raise money for a specific project wouldn't be considered "regularly carried on."

3. It Is Not Substantially Related

This is the final—and often the trickiest—piece of the puzzle. The activity itself must not be substantially related to your organization’s tax-exempt purpose. It’s not enough for the profits to fund your mission; the activity itself must contribute meaningfully to achieving it.

For instance, a museum selling prints and reproductions of art from its own collection is substantially related to its educational mission. A hospital that operates a public cafeteria is also related because it serves patients, visitors, and employees. But what if that same museum started selling commercial blenders? The link to its mission is gone, making it an unrelated business activity.

When organizing fundraising events that involve ticket sales or sponsorships, it's vital to track these different revenue sources carefully. Using specialized event management software for nonprofits can make this much easier by helping you separate mission-related contributions from potential UBTI.

Don't Pay Taxes You Don't Owe: Common UBTI Exemptions

So, you've identified an income stream that looks like it might be a trade or business. Don't panic just yet. Before you start earmarking funds for a tax bill, you need to see if the activity qualifies for one of the many exemptions the IRS provides.

Think of these as "get out of jail free" cards for specific, common nonprofit activities. The IRS created these statutory exemptions to ensure that typical fundraising and operational activities don't accidentally trigger Unrelated Business Income Tax (UBIT). Getting familiar with them is key to smart program design and protecting your organization's resources.

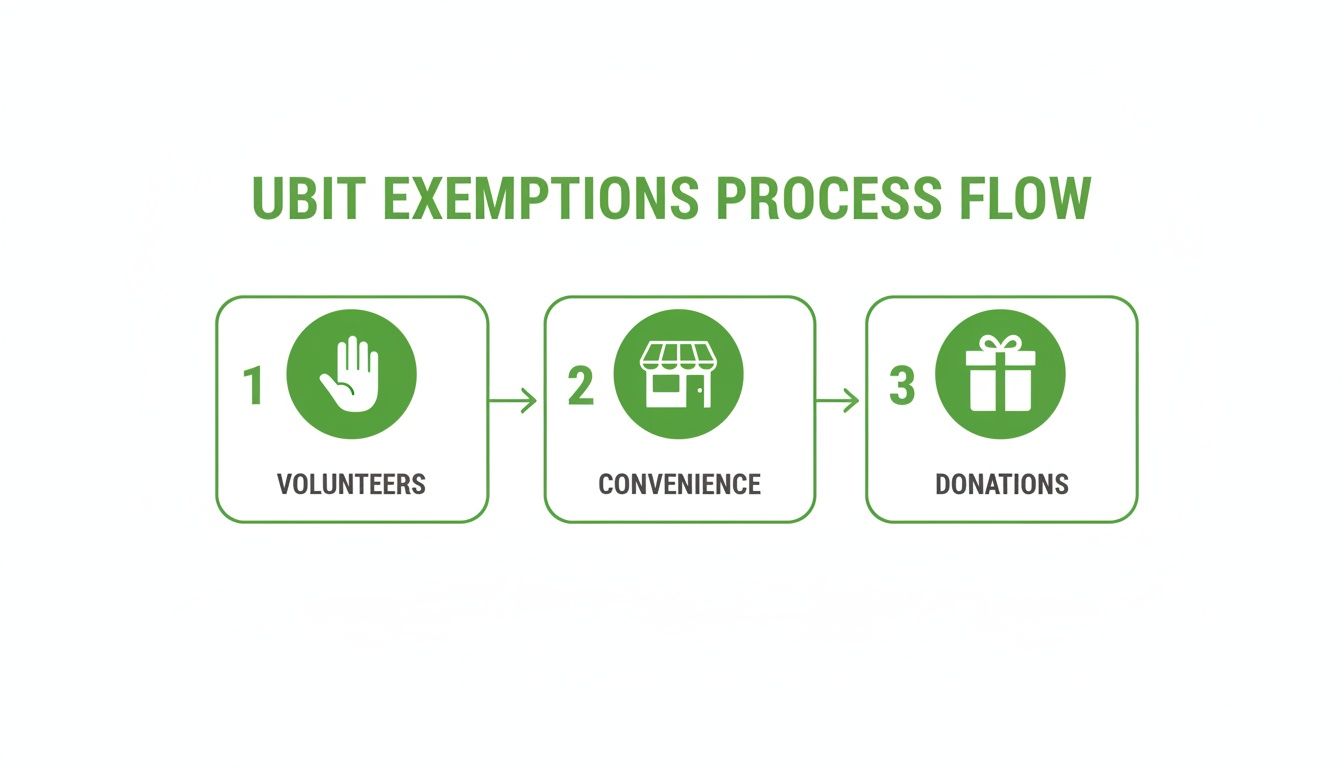

The flowchart below highlights three of the most powerful and widely used exemptions.

As you can see, simply by structuring an activity around volunteer labor, selling donated goods, or for the convenience of your members, you can often sidestep UBIT entirely.

Key Statutory Exemptions from UBTI

Let's break down the most common exemptions every nonprofit leader should have in their back pocket.

Volunteer-Run Activities: If an activity is run almost entirely by volunteers, the income is exempt. The IRS defines "substantially all" as at least 85% of the labor being performed by unpaid workers. A classic example is a church's weekly bake sale, where members of the congregation bake the goods, set up the table, and handle the sales—all without pay.

Convenience of Members: Income from a business operated mainly for the convenience of your members, students, patients, or employees is also exempt. This rule covers things like a university cafeteria serving its student body or a hospital gift shop selling magazines and flowers to patients and their families.

Sale of Donated Merchandise: When you sell items that were given to your nonprofit, the income you generate isn't UBTI. This is the bedrock exemption that allows thrift stores run by organizations like Goodwill and The Salvation Army to sell donated clothing and furniture tax-free.

Beyond these activity-based exemptions, there's another massive category of protected income: passive income. This is a huge deal for any nonprofit with an endowment or investment account.

Key Takeaway: The IRS generally excludes passive income from UBIT. This means dividends, interest, annuities, most royalties, and capital gains from selling property are typically not taxed.

This protection is what allows your investment earnings to grow without a tax drag. But be warned: the rules get tricky. The major exception is income from debt-financed property. If you earn rental income from a building that still has a mortgage, for instance, a portion of that income could suddenly become taxable UBTI.

UBTI vs Exempt Income Common Scenarios

Seeing these rules in action can help clarify when an activity crosses the line. Here’s a quick comparison of common nonprofit scenarios.

These examples show just how nuanced the rules can be. The same activity—selling merchandise—can be taxable in one context and exempt in another.

Avoiding Costly Exemption Mistakes

Misinterpreting these exemptions is one of the most common—and costly—mistakes a nonprofit can make. One major pitfall is confusing corporate sponsorships with advertising. If you provide a corporate partner with a "substantial return benefit" (like an ad that says "buy our product!"), that payment is taxable advertising income, not a tax-exempt sponsorship donation.

Another frequent error involves mixed-use facilities. Let's say your organization owns a building and you rent out the auditorium on weekends for weddings to generate extra income. You must have a system to accurately track and separate the direct and indirect expenses tied to that rental activity. If you don't, and an audit occurs, you could face penalties for underpaying your taxes.

How to Calculate and File Your Form 990-T

Alright, let's move from theory to practice. Filing a Form 990-T isn't just about spotting unrelated income—it’s about nailing the calculations, hitting your deadlines, and keeping spotless records. It can feel intimidating, but breaking it down into steps makes it manageable.

The whole process starts with calculating your Unrelated Business Taxable Income (UBTI). Think of it like a mini tax return for each business-like activity. You begin with the gross income that activity generated.

Then, you get to subtract the expenses that are directly connected to running it. This is where good bookkeeping really pays off. Deductible costs can include anything from staff salaries and marketing materials for that specific activity to a fair portion of shared overhead like rent or utilities. Getting this right is crucial—it ensures you're not paying a penny more in tax than you legally owe.

Understanding the Siloing Rule

Now for a critical twist in the rules: "siloing." In the past, you could lump all your unrelated business activities together. If your gift shop lost money, you could use that loss to offset profits from, say, renting out your parking lot. Not anymore.

The IRS now requires you to calculate UBTI for each unrelated business activity separately. A loss from one "silo" (like the gift shop) cannot be used to reduce the taxable income from another "silo" (like facility rentals). Each one stands on its own.

This change means you absolutely have to track the finances for each income stream independently. A great way to handle this is by setting up separate nonprofit bank accounts or using your accounting software to tag and segregate every dollar of income and expense for each activity.

Filing Deadlines and Extensions

When it comes to IRS deadlines, there's no room for error. For the vast majority of nonprofits, Form 990-T is due by the 15th day of the 5th month after your fiscal year ends. So, if you run on a calendar year (ending December 31st), your deadline is May 15th.

Feeling the time crunch? You can file for an automatic 6-month extension using Form 8868. Just be sure to file it on or before the original deadline. But here’s the catch: an extension to file is not an extension to pay. You still need to estimate the tax you'll owe and pay it by the original due date to avoid penalties.

Penalties and Recordkeeping

Ignoring these rules can get expensive, fast. The IRS can impose penalties of up to 25% of the unpaid tax for both filing late and paying late. For a nonprofit, that's a significant hit to your budget and your mission.

With around 1.41 million U.S. organizations filing a Form 990 of some kind each year, compliance is a massive focus for the IRS. A 990-T filing is a smaller subset, but it's a major red flag for auditors if it's missing or incorrect. A detailed analysis of nonprofit federal tax data highlights how crucial this compliance is for maintaining your status and eligibility for grants. The last thing you want is an audit or, in a worst-case scenario, a threat to your tax-exempt status.

To stay protected and prepared, your best defense is a solid audit trail. Keep detailed records of everything, including:

- Receipts for all unrelated income sources.

- Invoices and documentation for every related expense.

- Your methodology for allocating shared costs (like rent or utilities) across different activities.

- Internal notes or memos explaining why you've classified any borderline activities as "related" to your mission.

The Connection Between 990-T Compliance and Grant Funding

Keeping your financial house in order is about so much more than just satisfying the IRS—it’s about building rock-solid trust with your funders. Grantmakers, from the largest foundations to government agencies, perform rigorous due diligence. Your complete financial picture, which absolutely includes any Form 990-T filings, is a critical piece of their review puzzle.

When you manage and file your 990-T correctly, you send a powerful signal. It tells funders you operate with a high level of financial sophistication, transparency, and a deep commitment to good governance. In a competitive funding environment where every little detail matters, that’s a huge advantage.

A Signal of Good Governance

On the flip side, errors, late filings, or failing to file a necessary 990-T can raise immediate red flags. To a potential funder, it might suggest weak internal controls, a lack of financial oversight, or a fundamental misunderstanding of compliance. Those are risks many grantmakers simply aren't willing to take.

How you handle Unrelated Business Taxable Income (UBTI) directly shapes the perception of your organization's financial health. Funders want to see that you are not only generating diverse revenue streams but also managing them responsibly and legally. This perspective shifts 990-T compliance from a tedious administrative chore into a strategic part of a successful fundraising program.

Proper 990-T management showcases fiscal responsibility, directly impacting how foundations and government agencies perceive your organization's stability and readiness for funding.

The link between government funding and UBTI is especially direct. An analysis of Form 990 data revealed that at least 30% of filers received government grants, and many of those same organizations also managed UBTI to diversify their revenue. This makes understanding what is a 990-T essential for staying compliant within grant pipelines. You can explore more about this complex relationship between nonprofits and government revenue on the Johnson Center's blog.

Ultimately, a well-managed 990-T demonstrates to funders that you have a comprehensive grasp of your financial obligations. It’s a skill set that goes hand-in-hand with proper grant management. If you’re looking to tighten up your processes, our guide on the essential principles of accounting for grants is a great place to start.

Got Questions About Form 990-T? We’ve Got Answers.

As a nonprofit leader, you’re bound to run into some specific questions when dealing with tax forms. Let's tackle some of the most common ones about Form 990-T to help you navigate these tricky situations with confidence.

Do We Still File a 990-T If Our Unrelated Business Lost Money?

Yes, you probably do. The IRS doesn't look at your net profit to decide if you need to file; it looks at your gross income.

If your organization brought in $1,000 or more in total revenue from an unrelated business—before you subtract any expenses—a Form 990-T is required. This holds true even if that business activity ended up losing money for the year. Filing allows you to properly document the activity, its expenses, and stay compliant with the "siloing" rules for reporting each unrelated business separately.

What's the Real Difference Between Form 990 and 990-T?

It’s helpful to think of it like this: one is your annual report card, and the other is a potential tax bill.

- Form 990: This is your nonprofit’s yearly information return. It’s all about transparency, showing the public and the IRS your mission, finances, and how you're governed.

- Form 990-T: This is a straight-up tax return. Its only job is to report income from business activities that aren't related to your mission and to calculate any Unrelated Business Income Tax (UBIT) you might owe.

Is Corporate Sponsorship Money Considered UBTI?

This is a classic "it depends" situation. The answer lies in the details of your sponsorship agreement. If a company's payment qualifies as a qualified sponsorship, it's generally not UBTI. This means the sponsor gets little more than their name or logo displayed.

But, the moment you cross the line into advertising, the game changes. If you start promoting their products, endorsing them as an exclusive provider, or telling your audience to buy something, that income is likely taxable advertising revenue. It must be reported on Form 990-T.

When Should We Call in a Professional?

Navigating UBTI can get complicated fast. It’s always a smart move to consult a CPA or tax advisor who lives and breathes nonprofit accounting, especially if you find yourself:

- Launching a major new revenue-generating program.

- Unsure how to properly allocate expenses between your mission-based and business activities.

- Handling income from property that has a mortgage (debt-financed property).

- Just feeling overwhelmed or uncertain about your filing duties.

Getting an expert opinion early on can save you from major headaches and costly mistakes down the road.

Managing compliance, from 990-T filings to intricate grant reports, is essential to your nonprofit's long-term health. Fundsprout’s AI-powered platform helps you keep everything on track by centralizing your funding pipeline, making proposal writing easier, and simplifying your reporting. Discover how you can secure more funding while maintaining flawless governance.

Try 14 days free

Get started with Fundsprout so you can focus on what really matters.