Mastering the Statement of Activities for Nonprofits

Master the nonprofit statement of activities. Learn components, formats & how to use it for grant success & compliance. Essential guide for directors.

Abdifatah Ali

Co-Founder

A grant application is open on your screen. The funder wants your statement of activities, and someone on your team has asked a fair question: “Is that just our profit and loss?”

If you are a new executive director, this is the moment when nonprofit finance can feel needlessly opaque. You know your programs are working. You know your staff is stretching every dollar. But the funder is not asking for your passion. They are asking for evidence that your organization understands how money supports mission, how restricted funds are managed, and whether your operations can sustain the work you promise to do.

The statement of activities earns its place in this context.

Used well, this report does more than satisfy auditors and accountants. It helps you explain how revenue came in, what it was used for, what was limited by donor intent, and what changed in your organization’s net assets over the period. In plain language, it tells the financial story behind your mission. For a small nonprofit, that story can shape grant decisions, board confidence, and renewal conversations.

Why Your Statement of Activities Tells Your Mission's Story

The statement of activities matters because outsiders rarely see your daily decisions. They do not see a program manager reshuffling supplies to stay within a grant budget. They do not see your finance lead tracking a restricted award separately from general donations. They see a proposal, a few attachments, and a question in the back of their mind: can this organization manage funds responsibly?

The statement of activities answers that question in one of the clearest ways available.

Under U.S. GAAP, it is a required nonprofit financial statement governed by FASB ASC 958-220-45, and it serves as the nonprofit version of an income statement. The key difference is that it organizes financial activity by donor restriction status, not by profit margin, as explained by Clark Nuber’s overview of nonprofit statement of activities reporting.

That distinction is more important than it sounds.

A for-profit company usually asks, “Did we earn a profit?” A nonprofit asks, “What resources came in, what obligations shaped their use, and how did that affect our ability to carry out the mission?” The statement of activities is built to answer that second question.

What funders often see in this report

When a grantmaker reviews your statement, they are often looking for signals such as:

- Revenue stability: Are you relying on a narrow set of funding sources, or do you have a balanced base?

- Stewardship: Do restricted funds appear to be managed in a disciplined way?

- Operational reality: Are expenses aligned with the work you say you do?

- Financial movement: Did net assets improve, shrink, or shift because of intentional program delivery?

A strong statement of activities does not just say your organization is mission driven. It shows how financial decisions and donor intent connect to actual operations.

For a small nonprofit, this report becomes a bridge between accounting and fundraising. It can support a grant narrative, explain a past deficit without panic, and show why a new award would fill a real gap instead of disappearing into confusion.

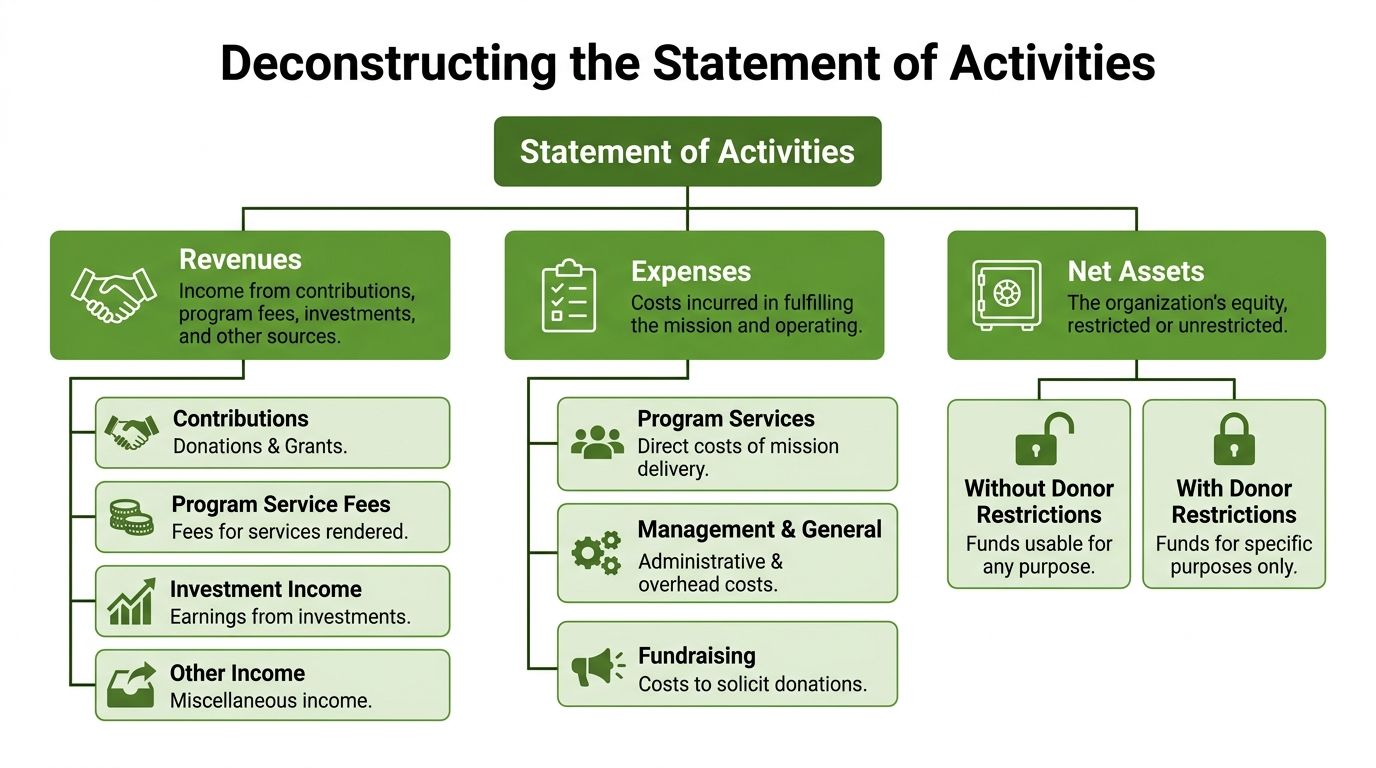

Deconstructing the Statement of Activities

A statement of activities usually becomes easier to read once you stop thinking of it as one dense report and start thinking of it as a simple flow. Money comes in. Money goes out. The remaining effect changes net assets.

That is the whole story.

Think in buckets, not line items

I often explain this report with a bucket analogy.

You have one bucket for funds without donor restrictions. Those are resources you can use for general operations, salaries, rent, program support, or whatever the organization needs within board-approved plans.

You have another bucket for funds with donor restrictions. Those dollars came in with instructions. A donor may have limited them to a specific program, time period, or purpose.

Then you have the total view, which combines both.

The statement tracks what flowed into each bucket, what was spent, and what changed by the end of the period.

The three core parts

Revenues

This section lists what the organization received during the reporting period. Common lines include contributions, grants, program service fees, investment income, and other income.

The practical question is not just “how much came in?” It is “what kind of money came in?” If a large share arrived with donor restrictions, your organization may look healthy on paper while still feeling tight on operating cash.

Expenses

This section shows what the organization spent to carry out its work and operate the entity. Expenses may include salaries, occupancy, supplies, professional fees, and other costs.

On the statement of activities, expenses contribute to the change in net assets. They also help readers judge whether spending patterns align with your stated mission and infrastructure needs.

Change in net assets

This is the bottom-line movement for the period. At minimum, nonprofits must present the change in net assets without donor restrictions, the change in net assets with donor restrictions, and the total change in net assets.

Many readers get tripped up at this point. A positive total change does not always mean you have flexible money to spend. If most of that increase sits in restricted net assets, your organization may still need unrestricted support.

What releases from restriction mean

One of the most useful parts of the statement is the line often called net assets released from restrictions.

Under FASB ASC 958, donor-restricted grants initially increase net assets with restrictions. When the organization fulfills the donor’s conditions or uses the funds for their intended purpose, the amount is released from restrictions and shifted into unrestricted operational use, as described by AccountingCoach’s explanation of the statement of activities.

That release is not new money. It is the formal accounting recognition that restricted funds have now been used properly.

If a funder wants proof that you can manage restricted awards, the release line helps tell that story. It shows movement from promise to execution.

Where preparation quality matters

A messy report often reflects messy setup. If your chart of accounts, grant tracking, and period close process are inconsistent, the statement will be harder to trust and harder to explain.

If your team needs a broader refresher on how to prepare financial statements effectively, that resource gives useful context on the discipline behind clean reporting. For grant-specific bookkeeping considerations, this guide on https://www.fundsprout.ai/resources/accounting-for-grants is also worth reviewing before your next reporting cycle.

Statement of Activities vs Other Financial Reports

A common source of confusion is that nonprofit leaders receive several financial reports that sound similar but answer very different questions. The statement of activities is only one piece of the set.

Here is the simplest way to separate them: each report answers a different management question.

Nonprofit Financial Statements at a Glance

| Financial Statement | Question It Answers | Key Information |

|---|---|---|

| Statement of Activities | What changed over the reporting period? | Revenue, expenses, gains, losses, releases from restriction, and changes in net assets |

| Statement of Financial Position | Where do we stand at one point in time? | Assets, liabilities, and net assets at a specific date |

| Statement of Cash Flows | Where did cash come from and where did it go? | Cash movement from operating, investing, and financing activities |

| Statement of Functional Expenses | How were expenses used across the organization? | Costs grouped by function such as program services, management and general, and fundraising |

The statement of activities is the motion picture

If the statement of financial position is a snapshot, the statement of activities is the movie. It shows what happened across the fiscal period.

This matters in grant conversations because funders are not only judging your current balance. They are judging whether your organization can manage the flow of revenue and expenses over time.

The statement of financial position is the balance snapshot

This report shows what you own, what you owe, and what remains as net assets on a specific date.

It is useful for discussing liquidity, obligations, and reserves. But it does not explain how the organization got there during the year. That narrative belongs to the statement of activities.

The cash flow statement answers a different problem

Cash and income are not the same. A nonprofit can report revenue before cash is received, and it can record expenses that do not immediately require cash.

That is why a nonprofit may appear stable on its statement of activities while still facing a short-term cash squeeze. The cash flow statement helps you see that distinction.

Functional expenses add the trust layer

The statement of functional expenses focuses on how costs are used by mission function. It is especially helpful for board members, donors, and watchdog readers who want to understand spending patterns.

If your executive team learns to ask the right question before opening the report, confusion drops quickly. If you want to understand performance over time, start with the statement of activities. If you want to understand position on a date, start with the balance sheet equivalent. If you want to understand cash timing, use the cash flow statement.

How to Classify Expenses for Funder Trust

Expense classification is where many nonprofits unintentionally weaken their financial story. The issue is not usually bad intent. It is inconsistency.

A funder sees salaries in one place this year, another place next year, and an unclear allocation note in the audit file. Confidence drops. The organization may still be doing good work, but the reporting no longer feels dependable.

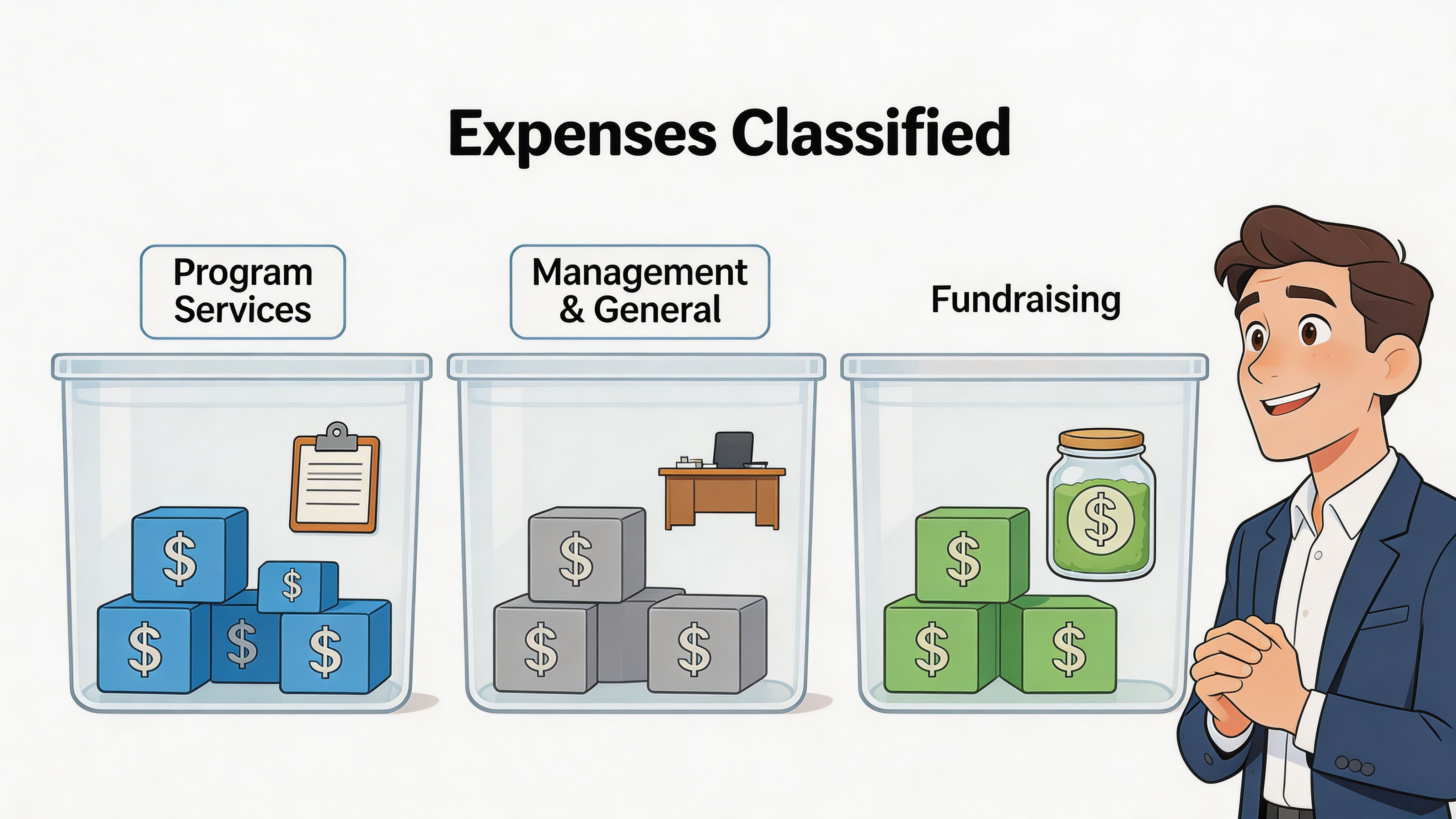

The statement of activities becomes more credible when expenses are classified carefully and consistently into program services, management and general, and fundraising.

According to Sage’s discussion of the nonprofit statement of activities, U.S. nonprofits average 72% program, 15% admin, and 13% fundraising, and a program ratio above 70% correlates with increased grant awards from major foundations. The same source notes that post-2016 ASU 2016-14 simplified reporting while still requiring disaggregated expense disclosures.

What each category means in practice

Program services

These are costs directly tied to mission delivery.

For a food pantry, this may include food distribution staff, pantry supplies, and direct program occupancy costs. For a youth tutoring nonprofit, it may include tutor wages, curriculum materials, and program transportation.

Management and general

These are the costs of running the organization itself.

Think finance staff, audit fees, board meeting support, general insurance, and a share of rent for administrative offices. These costs are necessary. They are not waste. But they should be classified accurately.

Fundraising

These are costs tied to generating contributed revenue.

Examples include donor appeal design, event promotion, development staff time devoted to solicitations, and fundraising software. If a cost exists primarily to bring in contributions, it belongs here.

Why funders care so much

A grantmaker is not looking only for a “high program percentage.” They are looking for a report they can trust.

If your nonprofit forces every shared salary into program just to look lean, astute readers notice. If you classify thoughtfully, explain your method, and stay consistent year after year, your financials become more believable.

Honest allocation builds more trust than aggressive allocation.

Reasonable allocation methods

Shared costs need a documented method. The best method is the one your team can defend and repeat consistently.

Examples include:

- Time-based allocation: Split staff compensation based on documented time spent across activities.

- Space-based allocation: Use square footage for occupancy and facility costs.

- Usage-based allocation: Assign costs like printing, software, or supplies based on actual use when available.

If your team needs examples of direct cost treatment before allocating shared expenses, this reference on https://www.fundsprout.ai/resources/example-of-direct-costs can help sharpen the distinction.

A short training video can also help staff and board members understand why the categories matter:

A quick allocation test

Before finalizing your report, ask:

- Would a stranger understand the purpose?

- Would the same cost land in the same category next quarter?

- Could we explain this to an auditor or grant officer without hesitation?

If the answer is no, revisit the classification now. It is much easier to fix before the report goes out than after a renewal question lands in your inbox.

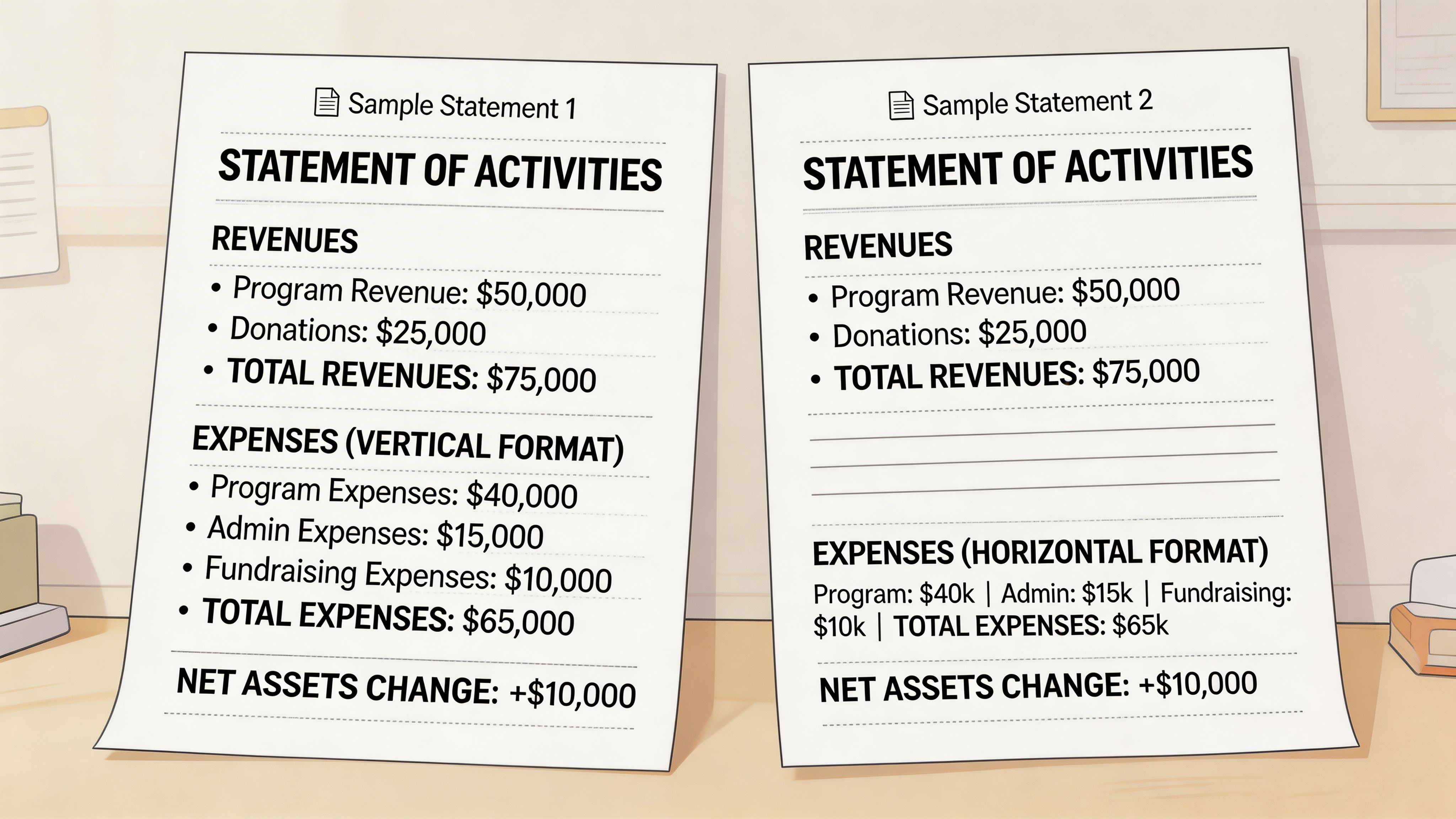

Sample Statement of Activities Formats in Action

Most leaders understand the statement of activities only after they see one in context. The layout may vary, but the storytelling logic stays the same.

One report might be compact and straightforward. Another may split columns by restriction class, program stream, or comparative period. If you want a simple visual example of financial data, that image can help readers picture how information is often arranged on the page.

{kind=link}

Format one for a small community nonprofit

A small organization often uses a vertical statement that looks something like this in concept:

| Line Item | Without Donor Restrictions | With Donor Restrictions | Total |

|---|---|---|---|

| Contributions and grants | X | X | X |

| Program service revenue | X | X | |

| Special event revenue | X | X | |

| Net assets released from restrictions | X | (X) | 0 |

| Total revenue and support | X | X | X |

| Program expenses | X | X | |

| Management and general | X | X | |

| Fundraising | X | X | |

| Change in net assets | X | X | X |

The value of this format is clarity.

An executive director can look at it and answer several questions quickly. How much support came in? How much was restricted? What did it cost to run programs? Did restricted funds move into active use during the year?

Reading the story behind the lines

Suppose a community arts nonprofit receives contributions, a local grant for youth workshops, and some earned income from ticket sales.

The statement might show:

- General contributions in the unrestricted column because leadership can use them where needed.

- A youth workshop grant in the restricted column because the donor specified the purpose.

- Ticket sales as program service revenue because the organization earned them through mission-related activity.

- A release from restrictions once the youth workshops took place and the restricted funds were used as intended.

That last line is especially important. It helps a reader see that the organization did not just receive a restricted grant. It delivered the work and accounted for the shift properly.

Format two for an organization with several restricted grants

A more complex nonprofit may still present the GAAP-required totals but use supporting schedules internally to track multiple grants.

For example, a health nonprofit could maintain:

- a main statement of activities with restricted and unrestricted columns

- a grant detail schedule by funder

- a release schedule showing when restricted funds moved into use

- a functional expense report tied to each program area

Leaders often get confused at this point. They think the statement of activities itself must carry every grant detail. It does not. The main statement presents the required categories. Supporting schedules provide the extra narrative for management, board review, and grant reporting.

Your statement of activities should stay readable. Use schedules and notes to add depth, not clutter.

Two common presentation styles

Single-year operating view

This is common for smaller teams and for grant attachments. It focuses on one reporting period and gives the reader a clean view of current-year performance.

Best for:

- annual reporting packages

- board packets for straightforward organizations

- grant applications asking for the latest audited or internal financials

Comparative view

Some nonprofits present current and prior year side by side. This helps the reader notice shifts in revenue mix, expense growth, and changes in net assets.

Best for:

- strategic planning discussions

- trend analysis

- renewal proposals where you want to show disciplined financial management over time

What to annotate when sharing with non-finance readers

If you submit this report to a board member, program director, or funder, add a short cover note that explains:

- Which lines are restricted versus flexible

- Any unusual one-time revenue or expenses

- Why releases from restrictions matter

- What the change in net assets does and does not mean

That small amount of guidance can prevent a common mistake. Someone sees a healthy total at the bottom and assumes the organization has plenty of cash. The note helps them understand whether the strength is operational, restricted, temporary, or seasonal.

Use Your Statement for Winning Grant Proposals

Many nonprofits attach the statement of activities to a grant proposal and move on. That wastes one of the most persuasive documents in the packet.

A funder is not just asking for a finance report. They are asking for proof that your organization can receive money, honor restrictions, spend with discipline, and report back clearly. The statement of activities can support all four points if you use it intentionally.

According to Jitasa’s discussion of nonprofit statements of activities, 68% of small nonprofits under $1M revenue struggle with grant compliance, creating a risk of 22% renewal denial rates. The same source says organizations with more than 15% annual releases from restrictions see 35% higher renewal success, which highlights how useful this report can be in renewal and compliance conversations.

Turn the report into a narrative, not an attachment

A good proposal does not assume the reviewer will interpret your financials the way you want. It guides them.

When you reference your statement of activities in the budget narrative or organizational capacity section, explain what it demonstrates.

For example:

- Your mix of revenue shows that the organization already manages both contributed and earned income.

- Your restricted and unrestricted activity shows that the finance team can separate donor intent from general operations.

- Your release pattern shows that awarded funds are being used and reported in alignment with program delivery.

- Your expense structure shows that the requested grant will support a real operating need, not a vague gap.

What funders often want to infer

Grantmakers often read the statement of activities to answer questions they may not state directly.

Can this organization handle restricted awards

If your report shows restricted support coming in and then being released appropriately as work is completed, that is a concrete sign of financial discipline.

This is especially helpful for renewal proposals. You are showing a history of doing what you said you would do.

Is the need credible

A proposal becomes more believable when the financial statement supports the narrative.

If your program has grown but unrestricted support has not kept pace, the statement of activities can help explain why you are seeking capacity funding, bridge funding, or general operating support.

Will our grant be absorbed into confusion

Small nonprofits sometimes lose credibility not because they lack impact, but because their financial presentation is messy. Clear activity by restriction class reduces that concern.

Funders do not expect perfection. They do expect a line of sight between awarded dollars, actual use, and resulting financial reporting.

A practical grant-writing workflow

Use the statement of activities before drafting the proposal, not after.

Review it with these questions in mind:

| Question | What to look for in the statement of activities |

|---|---|

| What funding gap are we trying to solve? | Shrinking unrestricted support, rising program costs, or heavy dependence on restricted revenue |

| What proof do we have of stewardship? | Clean releases from restrictions and consistent expense patterns |

| What should we explain proactively? | One-time deficits, unusual revenue spikes, or timing differences |

| What kind of request fits our reality? | Program support, general operating support, bridge funding, or renewal |

Then pair that review with a planning tool such as this https://www.fundsprout.ai/resources/grant-budget-template so your budget and your statement of activities tell the same story.

Language you can adapt for proposals

You do not need accounting jargon. You need precise, plain English.

Examples:

- “Our recent statement of activities shows a consistent pattern of using restricted funds for their intended program purposes and formally releasing them as activities are completed.”

- “The report also shows pressure on unrestricted operating support, which is why this request focuses on sustaining core program delivery capacity.”

- “Because our organization tracks restricted and unrestricted activity separately, we can provide clear post-award reporting tied to donor intent.”

These sentences work because they connect finance to trust.

What not to do

Avoid these habits:

- Do not paste numbers without interpretation. Readers may miss the meaning.

- Do not hide a deficit. Explain it if it reflects a planned investment, timing issue, or temporary funding shift.

- Do not oversell flexibility. Restricted net assets are not the same as general operating cash.

- Do not submit inconsistent reports. If the proposal budget, board packet, and statement of activities tell different stories, the reviewer will notice.

The strongest grant proposals treat the statement of activities as evidence. Not decoration. Not a compliance extra. Evidence.

Using Your Statement to Predict Future Funding Needs

The statement of activities is backward-looking by design, but good leaders use it to see forward.

One year of data can tell you what happened. Several years side by side can warn you what may happen next.

According to Givecloud’s discussion of nonprofit statements of activities, multi-year trends can reveal dependency risks when more than 50% of revenue comes from a few grants. The same source notes a recent FASB proposal around liquidity disclosures and cites analysis that nonprofits with less than 6 months of unrestricted reserves have 2.5x higher bankruptcy risk.

What to scan first across multiple years

Start with trend lines, not individual transactions.

Look for patterns such as:

- Growing restricted revenue with flat unrestricted support

- Recurring deficits in unrestricted activity

- Program expansion without a matching increase in flexible funding

- Dependence on a small group of grants or contracts

A nonprofit can show a positive total change in net assets and still be heading toward strain if the unrestricted side keeps weakening.

Three forecasting questions for leadership teams

Are we too dependent on a narrow revenue base

If a small set of grants drives most of the organization’s support, you have concentration risk. One delayed renewal can force staffing or program cuts.

Are restricted funds masking operating stress

A healthy restricted balance can create false comfort. If general operations rely on a thin pool of flexible support, leadership needs to know that early.

Are releases keeping pace with delivery

If restricted balances grow but releases stay slow, that may mean program timing is off, reporting is lagging, or grants are structured in a way that limits flexibility.

The most useful forecasting insight is often simple: which part of our financial story is healthy, and which part only looks healthy because of restriction timing?

A workable review rhythm

For a small nonprofit, you do not need a complex forecasting model to get value from this report.

Use a recurring review with your finance lead and development lead:

- Compare the current statement of activities with prior periods.

- Highlight shifts in unrestricted and restricted activity.

- Mark any grants that represent concentration risk.

- Translate those findings into fundraising priorities for the next cycle.

When finance and fundraising read the same report together, pipeline planning improves. The team stops chasing every opportunity and starts prioritizing support that fits the actual financial shape of the organization.

Common Questions About the Statement of Activities

Is the statement of activities the same as a grant budget

No. A grant budget is a forward-looking plan for a specific request or award. The statement of activities reports what happened across the organization during a period.

A funder may ask for both because one shows planning and the other shows financial track record.

How often should we prepare it

Externally, many nonprofits issue it as part of annual financial reporting. Internally, leaders often benefit from reviewing it more regularly so they can catch shifts in restricted funding, expense patterns, and net asset movement before year-end.

What software helps create it

Most nonprofit accounting systems can generate a statement of activities if the chart of accounts and fund structure are set up well. The software matters, but discipline in coding revenue, restrictions, and expenses matters more.

What if our board confuses it with cash on hand

That is common. Walk them through the difference between a change in net assets and actual cash available. A short cover memo can prevent major misunderstandings.

What should a new executive director focus on first

Start with three questions: what money is flexible, what money is restricted, and what changed this year that affects sustainability? Those answers make the rest of the report easier to understand.

Fundsprout helps nonprofits connect the dots between grant strategy, proposal writing, and compliance. If your team needs a better way to find relevant funding, organize proposal work, and keep reporting ready for renewals, explore Fundsprout.

Try 14 days free

Get started with Fundsprout so you can focus on what really matters.