A Clear Example of Direct Costs for Nonprofit Budgeting

Struggling with grant budgets? This guide breaks down a clear example of direct costs, showing you how to categorize and justify expenses like a pro.

Abdifatah Ali

Co-Founder

When you're building a grant budget, the most straightforward expense to account for is staff salaries for employees working exclusively on that project. Think of these as the expenses you can point to and say, "This dollar was spent solely for this program." They're not shared operational costs; they are tied directly to a single, grant-funded activity.

What Are Direct Costs in a Nonprofit Budget?

Let's cut through the financial jargon. Imagine your nonprofit is launching a new community garden project. The direct costs are the actual seeds, soil, and tools you have to buy specifically for that garden. They are expenses 100% dedicated to a single program. Without them, the project literally can't get off the ground.

These costs are the heart and soul of your grant proposal. They represent the tangible resources a funder’s money will purchase and show exactly how you'll put their investment to work. This is the "doing" part of your budget—the line items that directly fuel your mission's impact.

For example, if you're running an after-school tutoring program, the direct costs are easy to spot. It’s the portion of the tutor's salary for the hours they spend with students, the workbooks you buy for the kids, and the bus tokens you provide to get them to the center safely. Each expense is clearly and exclusively linked to the tutoring program itself.

Key Categories of Direct Costs

To build a grant budget that funders trust, you need to group these expenses into clear, understandable categories. Each one tells a part of your project's story, from who will do the work to what tools they'll need to succeed.

To help you get started, here's a quick look at the most common categories you'll find in a nonprofit grant budget.

Common Direct Cost Categories at a Glance

Understanding these buckets is the first step toward building a transparent and justifiable budget that funders can get excited about.

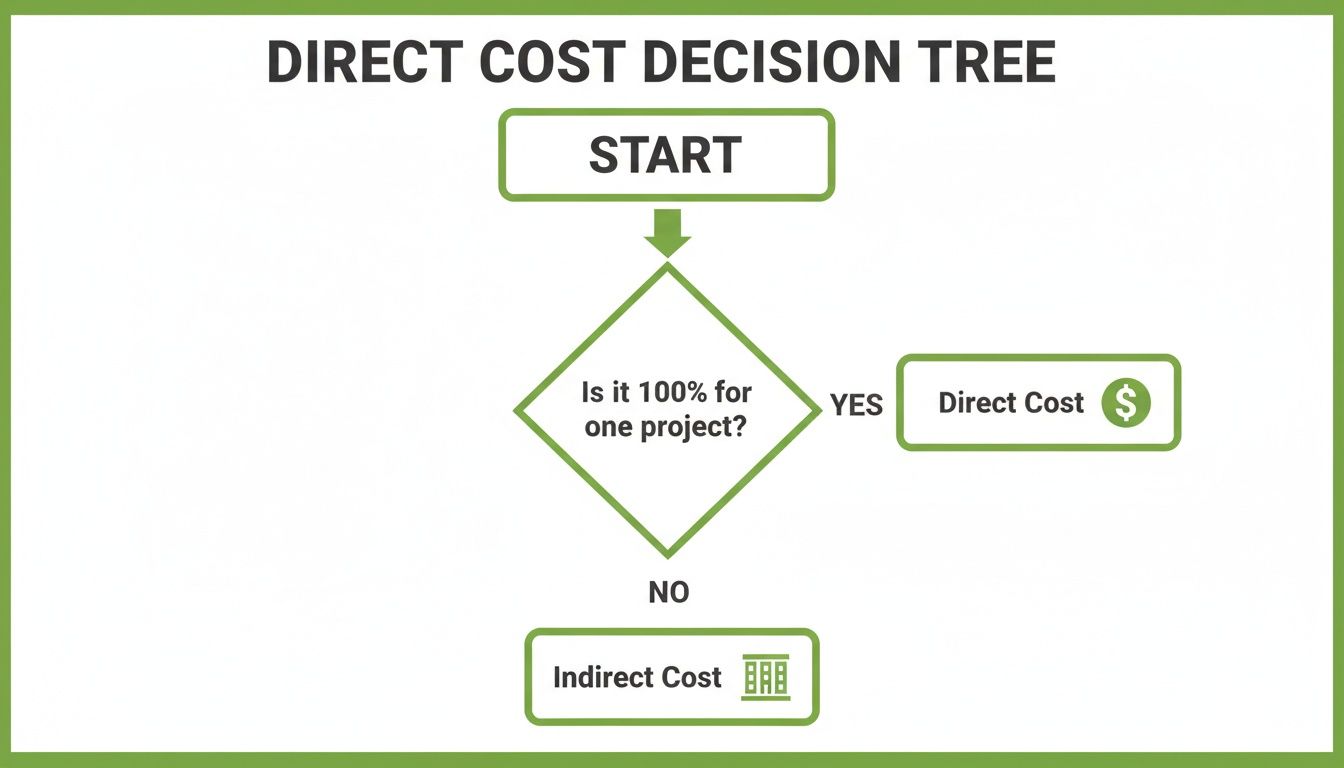

A direct cost is any expense that is incurred for and can be traced directly to a specific project or program. If you can answer "yes" to the question, "Was this cost solely for this one project?" it’s a direct cost.

This clarity is non-negotiable for funders. They need to see a direct line between their investment and your actions. Personnel costs are often the biggest piece of this puzzle, and it's important to budget for them accurately. For instance, global medical benefit costs are projected to jump by 10.4% in 2025, a trend that directly impacts your payroll expenses. You can dig deeper into these kinds of trends by reviewing insights from the WTW 2025 Global Medical Trends Survey. Getting a handle on these primary categories is your first step toward creating a budget that is realistic, defensible, and ultimately, fundable.

The Five Essential Examples of Direct Costs

Knowing the textbook definition of a direct cost is one thing. But when you’re staring at a blank grant budget template, you need to know what it looks like in the real world. This is where theory meets practice.

Let's walk through the five most common types of direct costs you'll budget for. To keep it grounded, we'll use a single, consistent example: a nonprofit launching a new youth literacy program.

Think of it this way: you're packing a suitcase for a specific trip. The clothes, toiletries, and guidebook you pack are your direct costs—they're essential for that trip. The suitcase itself, which you use for all your travel, is more like an indirect cost.

Staff Salaries and Fringe Benefits

For most nonprofits, your people are your biggest investment, and their time is your most significant direct cost. We're not talking about your Executive Director's full salary, but rather the specific slice of a staff member's time dedicated exclusively to the grant-funded program.

For our youth literacy program, the most obvious example is the salary for a part-time Reading Specialist hired just for this project. If they work 20 hours a week and spend 100% of that time on program activities—tutoring students, planning lessons, reporting on progress—then their entire salary is a direct cost.

Don't forget fringe benefits. Things like health insurance, retirement contributions, and payroll taxes are directly tied to that salary. If the specialist's salary is a direct cost, then the 30% (or whatever your rate is) budgeted for their benefits is also a direct cost.

A word of caution: funders demand proof. You absolutely must be prepared to back this up with timesheets or clear documentation showing that the time you billed to their grant was spent only on their project.

Project Supplies

Once you have your people, you need to give them the tools to do the job. Project supplies are the tangible, consumable items that get used up while running your program. They're the ingredients in your project's recipe.

For the literacy program, this category is pretty clear-cut:

- Books and Workbooks: The actual reading materials you'll purchase for the students in the program.

- Art Supplies: Crayons, paper, and markers needed for creative reading-comprehension activities.

- Printing Costs: The cost to print reading logs for students, informational handouts for parents, and certificates of completion.

Here's a simple gut check: Ask yourself, "Will this item be gone or completely used up by the end of the project?" If the answer is yes, it’s almost always a direct supply cost.

You wouldn't be buying these specific books or printing these worksheets if it weren't for this grant. That tight connection is what makes them a perfect example of a direct cost.

Project Specific Travel

Travel can be a fuzzy area, but it qualifies as a direct cost when it's absolutely essential for running the program. This isn't about an employee's daily commute; it’s about the travel required to deliver the actual services.

In our literacy program, a few types of travel would easily count as direct costs:

- Mileage Reimbursement: If the Reading Specialist drives their own car to visit students at three different school sites for tutoring, their mileage is a direct cost.

- Bus Tokens for Participants: If you provide transportation to help kids get to your program, that's a direct cost. Their participation depends on it.

- Conference Travel: If the grant funds a new curriculum and requires your program manager to attend a specific training conference to learn how to implement it, the airfare and hotel are direct costs.

Justification is everything here. You have to be able to draw a straight, clear line from each trip to a specific project goal.

Equipment

Equipment is different from supplies. It's about durability and cost. A workbook is a supply because it's used up. A tablet computer used for reading software is equipment because it lasts. As a rule of thumb, funders typically define equipment as a tangible item with a useful life of more than one year and a price tag over a certain amount, often $5,000.

Let's say our literacy program needs five specialized tablets with interactive reading software. If each tablet costs $1,200, the total purchase of $6,000 crosses that threshold and becomes an equipment cost. Since those tablets will be used exclusively by students in this program, their full cost can be charged directly to the grant.

This distinction matters because funders treat equipment differently. They might want to see multiple quotes or have specific rules about depreciation. Understanding these details is key to building a solid budget, and looking at a complete budget example for a nonprofit can show you exactly how these line items are presented.

Consultant and Contractor Fees

Finally, you can't always do everything in-house. Direct costs often include payments to outside experts or firms for services that are 100% for your project. You might bring in a consultant for niche expertise or hire a contractor to handle a specific task.

For our youth literacy program, a great example is hiring an independent evaluator to measure our success.

- Consultant: Paying an evaluator a $7,500 fee to design and conduct pre- and post-program assessments of the students' reading abilities. That service is entirely for this project.

- Contractor: Hiring a graphic designer to create a set of custom decodable readers that form the core of your curriculum.

These fees are direct costs because the work is specific, time-bound, and wouldn't exist without the grant-funded program. It’s a clean, direct line from the expense to the project's activities.

Drawing the Line Between Direct and Indirect Costs

Knowing the difference between direct and indirect costs is probably one of the most critical skills you can have when building a grant budget. If you get it wrong, you’re looking at rejected proposals or, even worse, compliance nightmares down the road. But when you get it right? You build trust with funders and secure your nonprofit’s financial health.

Think back to our analogy of your project as a recipe. The direct costs are the specific ingredients you need for that one cake—the flour, eggs, and sugar. In contrast, indirect costs (often called overhead or Facilities & Administrative costs) are the expenses for the kitchen itself.

You absolutely need the kitchen to bake the cake, but the electricity, rent, and insurance for that kitchen support every single meal you cook. These costs are essential but shared, which is what makes them indirect.

So, What Exactly Are Indirect Costs?

Indirect costs are all the shared operational expenses that keep your nonprofit’s doors open but can't be pinned to just one project. Think of them as the foundational costs that benefit all of your programs, not just the one you're seeking funding for.

Here are a few classic examples of these shared expenses:

- Administrative Salaries: The portion of salary for your Executive Director, HR manager, or finance team who support the entire organization.

- Office Rent and Utilities: The cost of your main office space, including electricity, water, and internet that everyone uses.

- General Insurance: Your organization's overall liability insurance that covers all operations, not just a single program.

- Office Supplies: General supplies like copy paper, pens, and printer ink that are available to all staff.

The key difference here is traceability. If you can’t easily and accurately trace an expense back to one specific grant-funded project, it belongs in the indirect cost pool.

This simple decision tree is a great tool for quickly deciding where a cost belongs.

As the flowchart shows, the core principle is simple: if a cost isn't 100% dedicated to a single project, it should almost always be classified as indirect.

Direct Costs vs Indirect Costs A Clear Comparison

To help clear up any lingering confusion, let's put some common nonprofit expenses side-by-side. Seeing how the same type of expense can be either direct or indirect depending on its use really makes the distinction click.

Nailing this distinction is fundamental to building a budget that funders will approve. For a hands-on look at how these items are structured in a real proposal, checking out a complete sample grant budget is an excellent next step.

It's important to remember that indirect costs aren't "less important" than direct costs; they're just accounted for differently. A strong nonprofit needs both well-funded programs and a stable operational backbone to truly succeed.

Why Do Funders Cap Indirect Costs?

You'll notice that funders often cap the percentage of a grant award that can go toward indirect costs, typically somewhere between 10% to 15%. They do this to make sure the bulk of their investment goes directly into programmatic activities—the work that achieves the project's stated goals.

This cap forces nonprofits to be efficient and strategic. You can't just ask for a grant to cover all your overhead. Instead, you have to calculate your total project costs (direct + indirect) and ensure your indirect portion falls comfortably within the funder's allowed limit. Understanding this from the start is absolutely essential for creating a budget that's both realistic and fundable.

How to Document and Justify Your Direct Costs

Simply listing your expenses isn't enough—a grant budget is only as strong as the story and the proof behind it. To build trust with funders and sail through any potential audit, you have to create a bulletproof financial narrative. Every single dollar you ask for needs a clear, logical, and documented reason for being there.

This process turns your budget from a simple spreadsheet into a compelling argument for your project's success. It proves to the funder that you are a responsible steward of their resources and have a concrete plan to turn their investment into real-world action. Without solid justification, even the most reasonable expense can be questioned or disallowed.

Think of yourself as a detective building a case. You need to gather the evidence—the receipts, timesheets, and invoices—that proves each cost is directly and exclusively tied to your project. This isn't just about checking a compliance box; it's about demonstrating your organization's competence and meticulous attention to detail.

Building Your Paper Trail for Key Costs

A solid justification is built on a meticulous paper trail. Each direct cost category has its own documentation needs, and being proactive about collecting this information from day one will save you from massive headaches down the road. Vague or missing records are a huge red flag for funders.

For personnel costs, the gold standard is detailed timesheets. Any staff member whose salary is partially or fully charged to a grant must keep clear records showing the specific hours they worked on that project’s activities. These aren't just for payroll; they are your primary evidence for the funder.

The same level of detail applies to your other expenses:

- Supplies: Keep every receipt and invoice. A great habit is to code them with the project name or grant number the moment you make the purchase.

- Travel: Maintain clear mileage logs for any vehicle reimbursement. For bigger trips, you'll need all receipts for flights, hotels, and meals, plus a short report explaining the trip's purpose and how it directly supported the grant’s objectives.

- Equipment: Save the purchase invoice and any quotes you gathered to ensure a competitive price. Be ready to explain exactly why this specific piece of equipment was essential for the project's success.

This isn't optional. Without this level of detail, you risk having costs disallowed during a report or audit, which can seriously damage your relationship with the funder and tarnish your organization's reputation.

The Art of the Budget Justification Narrative

Your budget justification, often called the budget narrative, is where you explain the "why" behind each number. It’s a short, clear explanation for each line item that connects the cost directly to your project's goals. Your mission is to prove every expense is reasonable, necessary, and allocable to this specific project.

A strong justification for any direct cost should quickly answer three key questions:

- What is it? (A clear description of the expense.)

- How did you calculate the cost? (Show your math. For example: 50 participant workbooks x $10/workbook = $500.)

- Why is it essential for the project? (Connect the expense to a specific program activity.)

Your budget narrative should leave no room for questions. A funder should be able to read it and understand precisely how you plan to spend every dollar and why it’s critical for achieving the outcomes you’ve promised.

Poor documentation can have devastating financial consequences. For instance, failed data integrations serve as a stark example of direct costs in technology projects, with organizations losing an average of $2.5 million per failure in software, labor, and hardware costs. Detailed planning and justification are crucial to prevent such losses. To understand the full financial impact, you can discover more insights on data transformation challenges. For practical help structuring your narrative, explore our comprehensive grant budget template, which provides a clear framework to follow.

Avoiding Common Budgeting Mistakes with Direct Costs

Simple mistakes in your grant budget can feel like tiny cracks in a foundation, but they can easily lead to a rejected proposal or a nightmare during an audit. Think of your budget as a pre-flight checklist; it's your chance to spot and fix problems before they become serious. When you get the details right, you show funders you’re trustworthy, transparent, and ready to manage their investment well.

The most common tripwire is misclassifying costs. It can be tempting to label an expense as "direct" to recover as much funding as possible, but this can backfire spectacularly. For instance, charging a slice of your Executive Director's salary as a direct cost looks great on paper, but unless you have meticulous timesheets proving they worked 100% on that specific project, it’s a huge red flag for funders.

This is where that line between direct and indirect costs is so important. If a cost benefits the organization as a whole—even a little bit—it belongs in the indirect pool. Getting this wrong isn't just a simple mistake; it can lead to disallowed costs, which means your nonprofit could be forced to pay back the funds.

Underestimating Your True Project Costs

Another hole nonprofits frequently dig for themselves is underestimating what it will actually cost to run the program. This often happens with things like program supplies or travel, where unexpected price jumps can blow a hole in your budget overnight. A classic example? Forgetting to account for inflation on a multi-year grant.

If you budget $5,000 for supplies in year one, you can't just assume that same amount will work three years later. That’s a recipe for a budget shortfall. A much smarter approach is to:

- Get Fresh Quotes: Don't guess or use old numbers. Call your vendors and get current pricing before you submit the proposal.

- Build in a Cushion: Not every funder allows a formal contingency line, but where you can, building in a small buffer (around 5%) for unexpected cost increases is a savvy move.

- Factor in Inflation: For any multi-year project, be sure to add a reasonable cost-of-living adjustment (2-4%) for salaries and a similar bump for supplies and other costs.

Failing to budget realistically doesn't just put a financial strain on your team. It also sends a signal to the funder that you might not have a solid handle on the real-world costs of your work, which can damage the credibility you've worked so hard to build.

Ignoring Specific Funder Guidelines

Every funder plays by its own rules. A one-size-fits-all budget is a fantasy. One foundation might be happy to cover equipment as a direct cost, while another might forbid it entirely. Ignoring these details is one of the fastest routes to the "no" pile.

A funder's guidelines are not suggestions; they are the rules of the game. You absolutely must read the Request for Proposal (RFP) and any financial instructions from top to bottom. It's a non-negotiable step.

This kind of detailed management is critical in every sector. In manufacturing, for example, profitability hinges on carefully managing the direct costs of raw materials. In fact, strong management of these costs helped U.S. manufacturing investments abroad earn a 9.0% return. You can discover more insights about direct investment trends to see just how vital this is. Just as a manufacturer has to track every penny spent on materials, your nonprofit must track and justify every cost according to the funder's specific rulebook.

Answering Your Top Questions About Direct Costs

Even after you've got the basics down, grant budgets have a way of throwing curveballs. The line between direct and indirect costs can get fuzzy, and every unique project seems to come with its own tricky questions. This is where we’ll tackle some of the most common head-scratchers that pop up when you're deep in the grant writing trenches.

Think of this as your on-call advice from a seasoned grant professional. We'll give you clear, straightforward answers to help you navigate those gray areas and build your budget with confidence.

Can a Portion of Our Office Rent Be a Direct Cost?

This is probably the most common question I get, and the answer is almost always no—with one major exception. Normally, your office rent is a classic indirect cost. It's part of your overhead, supporting the entire organization, so you can't pin it to just one project.

But here’s the exception: if your organization rents a separate, dedicated space that is used exclusively for a single grant-funded project, then that rent becomes a direct cost. For example, say you rent a small studio just for your "Art Therapy for Veterans" program. If only that program’s staff and participants ever set foot in it, you can charge the full rent directly to that grant. The key here is 100% exclusivity. The moment another program uses that space, even for a quick meeting, it's no longer exclusive and has to be treated as an indirect cost.

How Do We Handle Salary Increases in a Multi-Year Grant?

Forgetting to plan for salary increases in a multi-year grant is one of the quickest ways to find yourself with a budget crisis down the road. It’s a huge mistake to assume the salary you budget in year one will still be enough in year three. Funders not only understand this; they expect you to plan for it.

You absolutely should build a reasonable cost-of-living adjustment (COLA) right into your personnel budget for years two and three. A standard annual increase of 2-4% is a pretty common and accepted practice. Just make sure it aligns with your organization's own HR policies or what’s happening in your local economy.

The most critical part is being upfront about it in your budget justification. Your narrative needs to spell it out clearly.

Example Justification: "Personnel costs for the Program Coordinator include a projected 3% cost-of-living adjustment for Year 2 and Year 3 to account for inflation and ensure staff retention throughout the entire grant period."

This simple sentence shows the funder you’re a forward-thinking, responsible manager of their funds, which goes a long way in building trust.

Are Volunteer Hours Considered a Direct Cost?

Volunteer time is an incredible asset, but it isn't a cash expense. Because of that, you can't list volunteer hours as a direct cost that you're asking the funder to pay for. Think about it—that would be like asking them to reimburse you for money you never actually spent.

That said, the value of that time is massive and definitely belongs in your budget. You should list it as an in-kind contribution or cost share. This is a powerful way to show the funder that the community is invested in your project and that their grant money will be amplified by your dedicated volunteer base.

To do it right, you calculate the dollar value of that volunteer time using a defensible, standard rate (like the national volunteer hour value published by Independent Sector) and list it in a separate section of your budget. This is especially important when a funder requires a "match," because your in-kind contributions often count toward hitting that target.

What Is the Difference Between a Consultant and a Subcontractor?

This is a subtle but crucial distinction, and getting it wrong can have serious compliance consequences. While both consultants and subcontractors are direct costs for outside services, funders see them very differently and often have separate rules for each.

A consultant is usually an individual expert or a firm you bring in for specialized advice, training, or a specific service. They support your project, but they aren't carrying out a core piece of the program themselves.

- Example: You hire a professional evaluator to measure your program's outcomes and write the final impact report.

A subcontractor (sometimes called a subrecipient) is another organization you partner with to deliver a significant, programmatic piece of the work you promised the funder. They are essentially a partner in executing the core services.

- Example: Your nonprofit gets a grant to run a literacy program, and you hire a partner organization to run all the parent engagement workshops.

So why does this distinction matter so much? Funders typically have much stricter rules, heavier documentation requirements, and sometimes even require pre-approval for subcontractors. If you misclassify a subcontractor as a consultant, you could end up in hot water with compliance. Always check the funder’s guidelines and categorize these partners correctly. It protects your organization and keeps your relationship with the funder on solid ground.

At Fundsprout, we know that building a compliant and compelling grant budget is one of the toughest parts of the funding game. Our AI-powered platform helps you handle everything from finding the right opportunities to crafting a narrative that justifies every dollar. Stop guessing and start building budgets that win. Learn more about Fundsprout and transform your grant writing process today.

Try 14 days free

Get started with Fundsprout so you can focus on what really matters.