Optimize General & Administrative Expenses for Nonprofits

Master general & administrative expenses for nonprofits. Calculate, budget, and report G&A to win more grants & ensure compliance. Essential guide.

Abdifatah Ali

Co-Founder

You’re probably looking at a grant budget right now with a familiar knot in your stomach. The program team needs room for direct services. The funder’s guidance hints that “overhead” should stay lean. Meanwhile, you know the organization still has to pay for finance, HR, rent, audit support, insurance, software, and the executive time required to keep everything compliant.

That tension is where a lot of nonprofit leaders make avoidable mistakes. They understate general & administrative expenses in proposals, treat infrastructure as if it’s optional, and then scramble to deliver the grant with weak systems and exhausted staff. The result isn’t efficiency. It’s hidden subsidy, compliance risk, and preventable cash strain.

A better approach is to treat G&A as mission support. Not bloated overhead. Not a line you apologize for. A necessary investment that lets programs operate legally, report accurately, and scale without breaking.

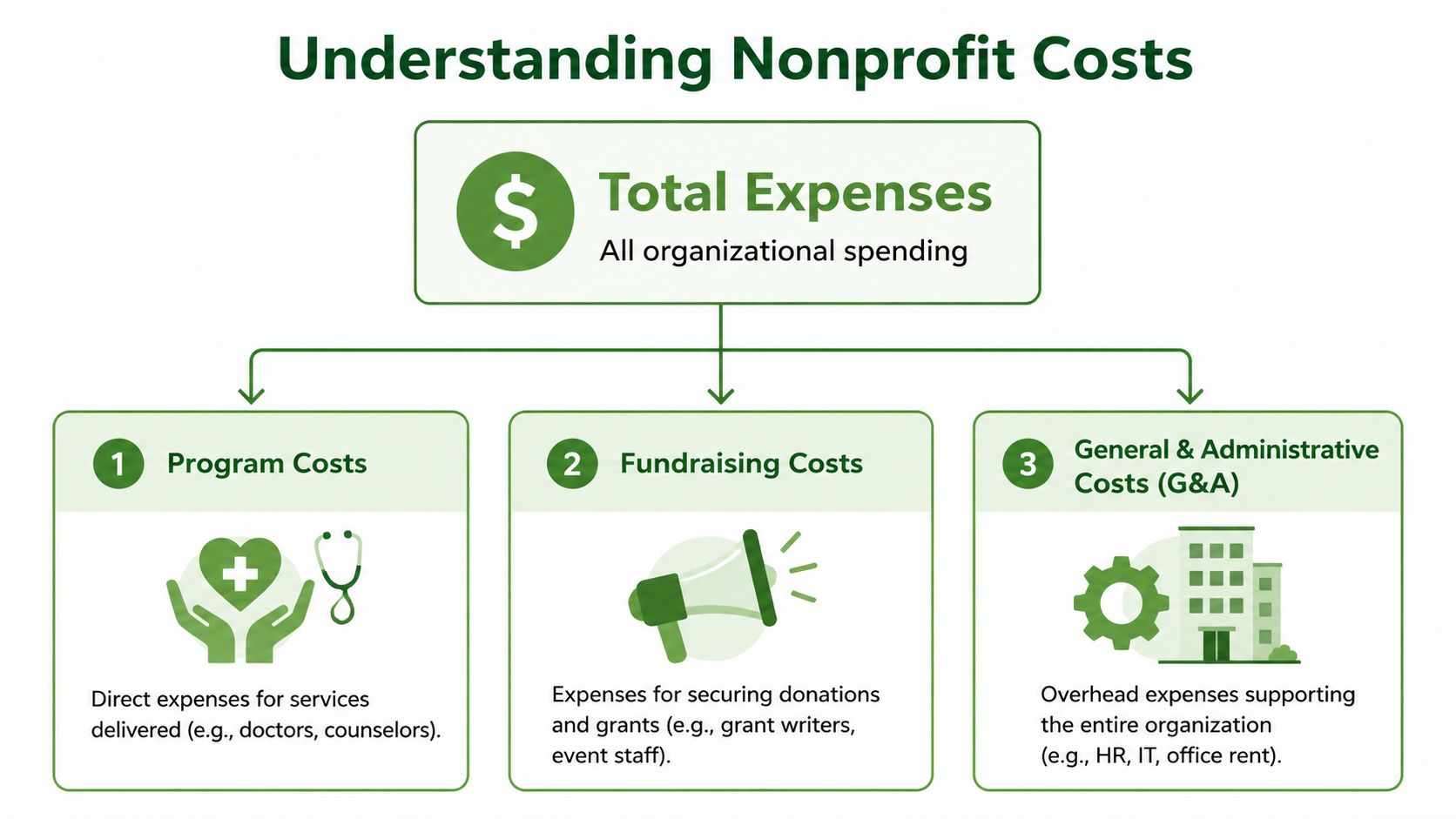

What Are G&A Expenses and Why They Matter for Grants

General & administrative expenses are the shared costs that keep the organization operating. They usually include executive and administrative salaries, office rent, utilities, insurance, legal and accounting services, compliance support, information technology, and other back-office functions that don’t map neatly to one program but are required for all of them to run.

For grant work, that definition matters because funders often examine these costs closely. Some funders set G&A caps of 15% to 25% of total budget, and high G&A can disqualify an application outright, according to ValueSense’s review of nonprofit G&A constraints. The same source says organizations that keep G&A under 20% through shared services win 30% more grants, and it notes that hybrid nonprofits saw facility G&A fall 18% in Q1 2026, which opened room for more program spending and stronger eligibility for competitive grants.

That doesn’t mean the lesson is “slash admin.” It means know your real cost structure and manage it intelligently.

What belongs in G&A

If a cost supports the whole organization rather than one grant, one donor campaign, or one service line, it probably belongs in G&A. Common examples include:

- Finance operations: bookkeeping, controller oversight, audit prep, accounts payable

- Leadership support: executive direction that isn’t directly supervising one funded program

- Shared office costs: rent, utilities, insurance, reception, office management

- Organization-wide systems: accounting software, payroll tools, cybersecurity, general IT support

- Compliance infrastructure: legal review, HR administration, board support, policy maintenance

Many new executive directors benefit from revisiting the basics of understanding accounting expenses before they finalize grant budgets, especially when they need to separate organization-wide overhead from direct program delivery.

Practical rule: If you removed the cost and the whole organization would become less stable, less compliant, or less able to report accurately, you’re likely looking at G&A.

Why funders care

Funders aren’t wrong to ask hard questions about overhead. They want confidence that grant dollars will reach the intended work. But the strongest proposals don’t pretend administration is free. They show that the organization has enough infrastructure to manage the award well.

A grant-funded program without reliable finance support can miss reporting deadlines. A nonprofit without proper HR processes can create avoidable staffing problems. A leadership team that underbudgets administration often pushes true costs into unrestricted funds, then wonders why growth feels fragile.

The goal isn’t to win points for having the smallest G&A line. The goal is to show that your organization uses administrative resources with discipline, transparency, and purpose.

Distinguishing G&A from Program and Fundraising Costs

Most classification problems start with one bad habit. People ask, “Is this expense important?” Nearly every nonprofit cost is important. The better question is, “What activity does this cost support?”

Think about a community health clinic. A clinician delivering care is a program cost. A grant writer preparing foundation applications is a fundraising cost. The finance director reconciling accounts and preparing audit schedules is a general & administrative cost. All three are necessary. They just serve different functions.

The practical distinction

Program costs exist because you deliver services.

Fundraising costs exist because you raise contributed revenue.

G&A costs exist because the organization itself must function.

That sounds simple until you get to shared roles, software, and executive time. Then judgment matters. In nonprofits, G&A often makes up 15% to 25% of total operating budgets, with typical breakdowns of 50% to 60% personnel, 15% to 20% occupancy, 10% to 15% professional services, and 10% to 15% technology and office expenses, according to Financial Modelslab’s nonprofit G&A guide. The same source says exceeding a 25% G&A ratio correlates with a 30% to 50% lower funding success rate.

That’s one reason clean classification matters. If you dump shared costs into the wrong bucket, your ratios stop telling the truth.

Expense classification examples

| Expense Item | Program Cost | Fundraising Cost | General & Administrative (G&A) Cost |

|---|---|---|---|

| Counselor salary providing client services | Yes | No | No |

| Case manager travel to client site | Yes | No | No |

| Program-specific training materials | Yes | No | No |

| Curriculum licenses used only in a funded program | Yes | No | No |

| Grant writer salary | No | Yes | No |

| Donor event venue rental | No | Yes | No |

| Online donation platform fees | No | Yes | No |

| Direct mail appeal printing | No | Yes | No |

| Executive director time on organization-wide planning | No | No | Yes |

| Finance director salary | No | No | Yes |

| Audit fee | No | No | Yes |

| General liability insurance | No | No | Yes |

| Office rent for shared headquarters | No | No | Yes |

| Payroll software for the whole organization | No | No | Yes |

| CRM used only for donor cultivation | No | Yes | No |

| HR consultant updating handbook | No | No | Yes |

| Development director travel to meet prospects | No | Yes | No |

| Program supervisor managing one grant-funded service line | Yes | No | No |

| Board meeting support and governance records | No | No | Yes |

| Volunteer recruitment ad for a gala | No | Yes | No |

| Client meals required by program design | Yes | No | No |

| Website donation landing page redesign | No | Yes | No |

| Cybersecurity software protecting all staff devices | No | No | Yes |

| Temporary bookkeeper during audit season | No | No | Yes |

| Executive director time supervising a program manager | Yes, if documented | No | Yes, if organizational |

Where teams usually get it wrong

Misclassification tends to show up in a few repeat areas:

- Executive salaries: One executive role can support programs, fundraising, and administration. Allocate it based on actual duties and documentation.

- Software: Donor databases are usually fundraising. Accounting software is usually G&A. Program case management systems are usually program.

- Occupancy: Shared rent often belongs in G&A unless you have a defensible allocation method by space usage.

- Communications: A brochure for clients is program. A year-end appeal is fundraising. General brand management may be G&A, depending on function.

The cleanest books aren't the ones with the lowest overhead. They're the ones where every dollar has a defensible home.

A simple test for gray areas

Ask three questions:

- Would this cost exist if the program ended but the organization stayed open? If yes, it leans G&A.

- Is the primary purpose to raise money? If yes, it leans fundraising.

- Can you tie the expense directly to service delivery? If yes, it leans program.

That framework won’t solve every edge case, but it keeps your team from making classification decisions based on optics instead of accounting logic.

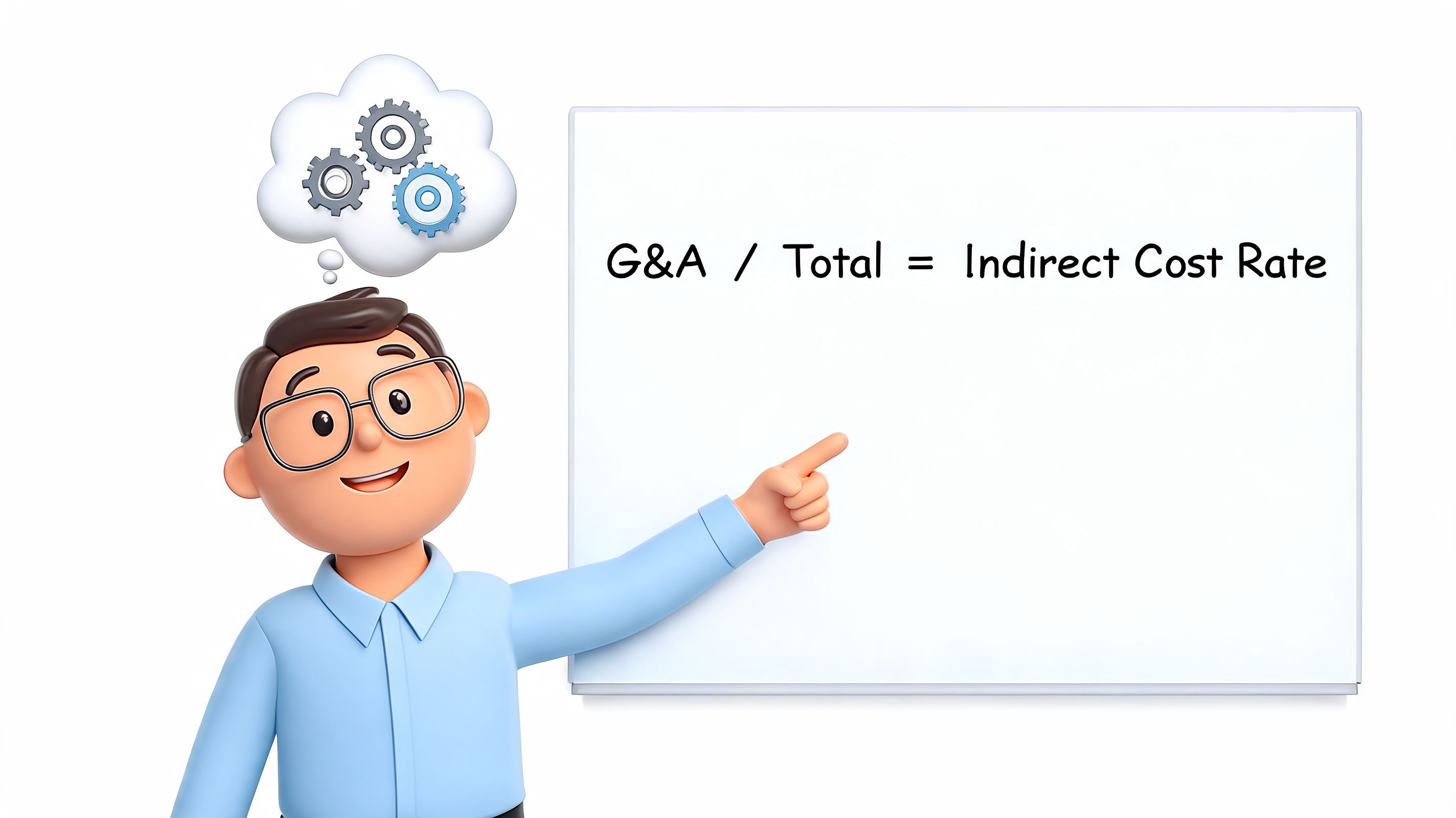

Calculating Your Nonprofit's Indirect Cost Rate

You can’t defend your indirect costs if you’ve never calculated them clearly. Too many nonprofits use a rough guess, then build proposal budgets around that guess. That creates problems fast, especially when a federal opportunity asks for a defined rate or a funder asks how you arrived at your administrative charge.

Start with the simple organizational view

A useful internal KPI is the G&A-to-revenue ratio, calculated as G&A / Revenue × 100. Spendesk’s explainer on general and administrative expenses describes this as a critical KPI for nonprofits and places benchmark ranges at 10% to 20%. It gives a practical example where $100k in admin salaries + $10k in rent + $2.5k in utilities = $112.5k in G&A on $500k in revenue, which yields a 22.5% ratio. The same source says each 5% increase in that ratio can erode operating margins by 3% to 7%, and ratios above 20% can reduce funder confidence by 35%.

That ratio isn’t the same as a federally negotiated indirect cost rate, but it tells you whether your back-office cost structure is generally in line with your revenue base.

Then calculate the rate you’ll use for grant planning

Most nonprofits should calculate at least two versions of an indirect rate:

- Internal G&A rate: total G&A divided by total organizational expenses or revenue, depending on your management preference

- Grant budgeting rate: a defensible rate based on the direct-cost base allowed by the funder

To build either one, your chart of accounts has to be clean. If expense coding is inconsistent, your rate will be unreliable. To address this, practical business expense categorization tips can help staff assign costs consistently before you try to calculate any rate.

How to approach MTDC for federal-style budgeting

For many government grants, the more relevant concept is Modified Total Direct Costs, usually called MTDC. In practice, that means you identify your allowable direct cost base, then apply an indirect rate to that base.

A workable process looks like this:

Build your indirect pool

Include shared administrative costs such as finance, HR, executive administration, general office occupancy, and organization-wide systems.Build your direct cost base

Include direct program costs that fit the grant’s rules and your accounting records.Remove excluded items from the base when required

Federal opportunities often exclude certain items from the base. Read the notice carefully and align your calculation with the specific grant terms.Divide the indirect pool by the approved direct cost base

That gives you the rate you can defend.

For a deeper walkthrough, keep a practical calculator and examples handy. This guide on how to calculate indirect costs is a useful reference point when you’re building budgets or checking whether your assumptions hold up.

What a good rate calculation should produce

A solid indirect cost calculation should answer four questions without hesitation:

- What costs are in the pool

- What costs are in the base

- Why certain costs were excluded

- Whether the rate matches actual historical operations

If your finance team can't explain the rate in plain language to a program director, it probably isn't ready for a funder.

The rate itself matters, but the discipline behind it matters more. Funders and auditors both notice when an organization uses the same logic year after year and keeps documentation that ties back to actual books.

Budgeting and Allocating G&A Expenses for Proposals

The grant budget is where theory gets tested. If your true administrative need is higher than what you put in the proposal, the difference doesn’t disappear. It lands somewhere. Usually in unrestricted funds, staff burnout, delayed reporting, or postponed systems work.

That’s why accurate G&A budgeting is a sign of organizational maturity. It tells a funder that you understand your cost structure and intend to manage the award responsibly.

There is no single perfect percentage

Organizations vary widely. Discern’s metric guide on G&A as a percentage of revenue places typical G&A expenses between 4% and 30% of total revenue, depending on size, industry, and growth stage. It gives one example of a company with $75 million in revenue and $9.75 million in G&A, which reflects a 13% ratio.

That range matters because nonprofits often go hunting for one “acceptable” number. There isn’t one. What matters is whether your rate is reasonable for your model, your compliance requirements, your staffing structure, and your scale.

Build proposal budgets from actual operating reality

When I review budgets that later go sideways, I usually find one of two problems. Either the organization copied last year’s indirect line without recalculating it, or it shaved G&A to satisfy a presumed funder preference and hoped to absorb the shortfall later.

A stronger process looks like this:

- Use recent actuals first: Start with historical administrative spending, not wishful thinking.

- Allocate shared personnel carefully: Executive directors, operations staff, and finance roles often need documented splits across program, admin, and fundraising.

- Match the funder’s format: If the application asks for indirect, use indirect. If it expects fully loaded direct lines, translate the same reality into that structure.

- Write the budget narrative clearly: Explain how administrative support protects compliance, reporting quality, financial stewardship, and continuity.

If you need a clean working format, this grant proposal budget template can help teams map direct and indirect assumptions before they submit.

A defensible salary allocation example

An executive director’s compensation rarely belongs entirely in one bucket. Part of the role may involve direct program oversight. Part may involve fundraising. Part may involve administration, governance, audit review, insurance oversight, and organization-wide leadership.

That means you need support for the split, such as time records, a written allocation methodology, calendar-based estimates reviewed periodically, or a board-approved cost allocation policy.

A simple narrative might read like this:

The Executive Director provides organization-wide leadership, grant compliance oversight, financial review, board coordination, and direct supervision of program leadership. Salary costs are allocated based on documented functional responsibilities and reviewed periodically for consistency with actual activity.

What does not work

These habits create trouble fast:

| Weak practice | Why it fails |

|---|---|

| Setting G&A at an arbitrary cap with no calculation | It breaks the link between budget and reality |

| Charging shared admin time as fully direct without support | It creates audit and reporting risk |

| Leaving out software, insurance, and finance review costs | It understates what delivery actually requires |

| Using different allocation logic for each proposal | It makes your books hard to defend |

The cleanest grant budgets don’t hide overhead. They show that the nonprofit knows how to carry the full cost of quality work.

Navigating Allowable and Unallowable Costs

Every nonprofit leader eventually learns this the hard way. A cost can be real, necessary, and still not be allowable as charged to a specific grant.

That’s why compliance work around general & administrative expenses has to start with policy, not preference. Federal funding rules often shape the strictest version of this discipline, and many foundations borrow the same logic even when they don’t use federal language.

What usually counts as allowable G&A

Allowable doesn’t mean automatically chargeable in every situation. It means the cost is generally permissible if it’s reasonable, properly allocated, documented, and consistent with the funder’s rules.

Typical examples include:

- Financial management: audit support, accounting services, bookkeeping, payroll processing

- Administrative leadership: executive oversight tied to governance, risk management, and organizational administration

- Insurance and occupancy: general liability coverage, office rent, utilities, shared office operations

- Organization-wide systems: accounting software, payroll platforms, cybersecurity, administrative IT support

- Compliance functions: HR administration, policy maintenance, records retention, procurement oversight

What usually creates problems

Some costs are commonly restricted, disallowed as direct charges, or require special scrutiny under grant rules.

Watch these closely:

- Lobbying activities: often restricted or unallowable under many grants

- Entertainment expenses: usually difficult to justify as allowable

- Fundraising costs: typically not chargeable to program grants as direct program expenses

- Personal or inadequately documented expenses: lack of support can make even legitimate costs fail review

- Bad allocations: a cost may be allowable in theory but disallowed if the method of assigning it is inconsistent

Your first compliance document shouldn't be a grant budget. It should be a written cost allocation policy that staff can actually follow.

Inflation changed the pressure on admin budgets

The compliance conversation is harder when costs are rising. Rippling’s G&A overview notes that amid 2025 to 2026 inflation, global wages rose 5.2% and utilities rose 12%, increasing G&A pressure. The same source says a 2026 Deloitte study of 200 nonprofits found that AI adoption in G&A functions reduced those expenses by 10% to 20%, helping organizations stay under the 10% to 15% G&A-to-revenue ratio recommended by evaluators like Charity Navigator.

That doesn’t mean every nonprofit should rush into automation for its own sake. It does mean leaders should review manual accounting, bill pay, document collection, and reconciliation work with fresh eyes.

Documentation is what saves you

If you want costs to survive scrutiny, keep these basics in place:

- Written allocation methodology

- Consistent coding in the accounting system

- Support for shared salary allocations

- Invoices, contracts, and approvals

- Periodic review of actual use versus budgeted use

A reasonable cost with weak records becomes a questioned cost. A modest investment in documentation usually prevents much larger headaches later.

Communicating Your G&A Needs to Funders

Funders rarely respond well to defensive language about overhead. If your narrative sounds like an apology, it invites doubt. If it sounds disciplined, specific, and tied to outcomes, it builds trust.

The shift is simple. Stop framing G&A as money that does not reach the mission. Start framing it as the infrastructure that lets the mission operate safely, consistently, and accountably.

What funders want to hear

A strong explanation of administrative costs usually does three things well:

Connects support functions to program quality

Finance review supports accurate drawdowns, clean reporting, and timely closeout.Shows discipline instead of sprawl

The organization monitors shared costs, allocates them consistently, and adjusts when spending drifts.Makes growth look manageable

Additional funding won’t overwhelm the back office because the nonprofit has thought through what administration the work requires.

That’s a much better story than “we tried to keep overhead low.”

Language that works better than overhead talk

Try language like this in narratives and conversations:

Administrative costs support the financial controls, compliance oversight, technology systems, and executive management required to deliver the proposed services responsibly and report on outcomes accurately.

Or this:

Shared operational costs are allocated using a consistent methodology so that program budgets reflect the true cost of implementation without overstating direct service expenses.

Those sentences do an important job. They move the conversation from overhead as waste to infrastructure as stewardship.

How to answer hard questions

When a funder pushes back, stay calm and stay concrete.

| Funder concern | Strong response |

|---|---|

| “Your admin costs seem high” | Explain what functions are included, how they’re allocated, and why they are necessary for compliance and service continuity |

| “Can’t this be covered elsewhere?” | Clarify what unrestricted funds already subsidize and why full-cost funding improves long-term stability |

| “We prefer direct service spending” | Connect admin support to reporting, staffing reliability, risk management, and program execution |

For teams that need help refining these conversations internally before they happen externally, these effective communication strategies are useful for aligning finance, development, and program staff around the same message.

A funder doesn't need you to pretend your infrastructure is free. They need confidence that it is well run.

The tone matters

Be transparent. Be brief. Be specific.

What doesn’t work is sounding aggrieved about overhead caps or trying to bury G&A in vague language. Experienced reviewers know what administration costs. They’re looking for organizations that understand their own operations and can justify them cleanly.

FAQ on General and Administrative Expenses

Can restricted grant funds pay for G&A

Sometimes yes, sometimes no. It depends on the funder’s rules, the approved budget, and whether the administrative cost is treated as allowable indirect expense or built into permitted direct lines.

The key is not to assume. Read the award terms, the budget instructions, and any indirect cost guidance before submission. If the grant limits indirect costs, don’t charge disallowed administration somewhere else without a defensible basis. That’s how reporting problems start.

What if a funder’s cap is lower than our real rate

This is common. When it happens, handle it openly.

You usually have a few options:

- Use unrestricted support as subsidy: That’s acceptable if leadership understands the true gap and approves the subsidy consciously.

- Revise scope to match the cap: If the funder will only support a thinner infrastructure layer, the project may need a smaller footprint.

- Blend revenue sources: Some nonprofits pair a restrictive grant with general operating support or a second funder that helps absorb shared costs.

- Negotiate where possible: Some funders won’t move. Others will allow fuller coverage if you explain the cost drivers clearly.

The mistake is pretending the gap isn’t there. A capped indirect line doesn’t change your actual administrative burden.

How should a new or very small nonprofit estimate G&A for its first proposal

Start with reality, not aspiration. List the administrative costs you already incur or know you must incur to manage the grant responsibly. That often includes bookkeeping, payroll processing, leadership oversight, insurance, software, and basic office operations.

Then create a simple allocation approach and document it. Even if your systems are small, the method should be consistent. Small nonprofits often underbudget because the founder or executive director absorbs unpaid or undercounted administrative work. That may get one proposal out the door, but it isn’t a sustainable operating model.

Should we always try to lower G&A

No. You should try to eliminate waste, duplicate systems, poor vendor terms, and weak processes. That’s different from stripping away necessary capacity.

Sometimes higher G&A reflects a transition you need, such as stronger financial controls, better reporting systems, or investments that prepare the organization for larger and more complex awards. The right question is whether the spending is justified, documented, and producing a more resilient organization.

What records matter most if our allocations are reviewed

Keep records that show your logic and your consistency. That usually means a written cost allocation policy, approved budgets, payroll records, role descriptions, vendor invoices, and support for how shared salaries or occupancy are divided.

If your team can explain the allocation method the same way in the proposal, the accounting system, and the financial statements, you’re in good shape. If every grant uses a different logic, fix that before your portfolio grows.

If your team is trying to tighten G&A management without weakening programs, Fundsprout can help you connect budgeting, proposal development, compliance planning, and renewal tracking in one place. It’s built for mission-driven organizations that need a clearer path from funding strategy to grant execution.

Try 14 days free

Get started with Fundsprout so you can focus on what really matters.