How to Estimate Project Costs for Nonprofit Grants

Learn how to estimate project costs for nonprofit grant proposals. Covers bottom-up, analogous, & parametric methods, plus overhead & contingency.

Abdifatah Ali

Co-Founder

You're probably staring at a grant deadline, a half-built program idea, and a spreadsheet that already feels accusatory.

The Executive Director wants a number. The program team keeps changing the plan. The funder's budget form has six tabs, three locked cells, and one line called “other” that somehow needs to explain reality. That's a normal day in nonprofit budgeting.

The good news is that learning how to estimate project costs isn't magic, and it isn't reserved for finance people. It's a discipline. The strongest grant budgets come from the same habits every time: clear scope, defensible assumptions, detailed line items, and a budget narrative that proves you've thought through delivery, not just wishful spending.

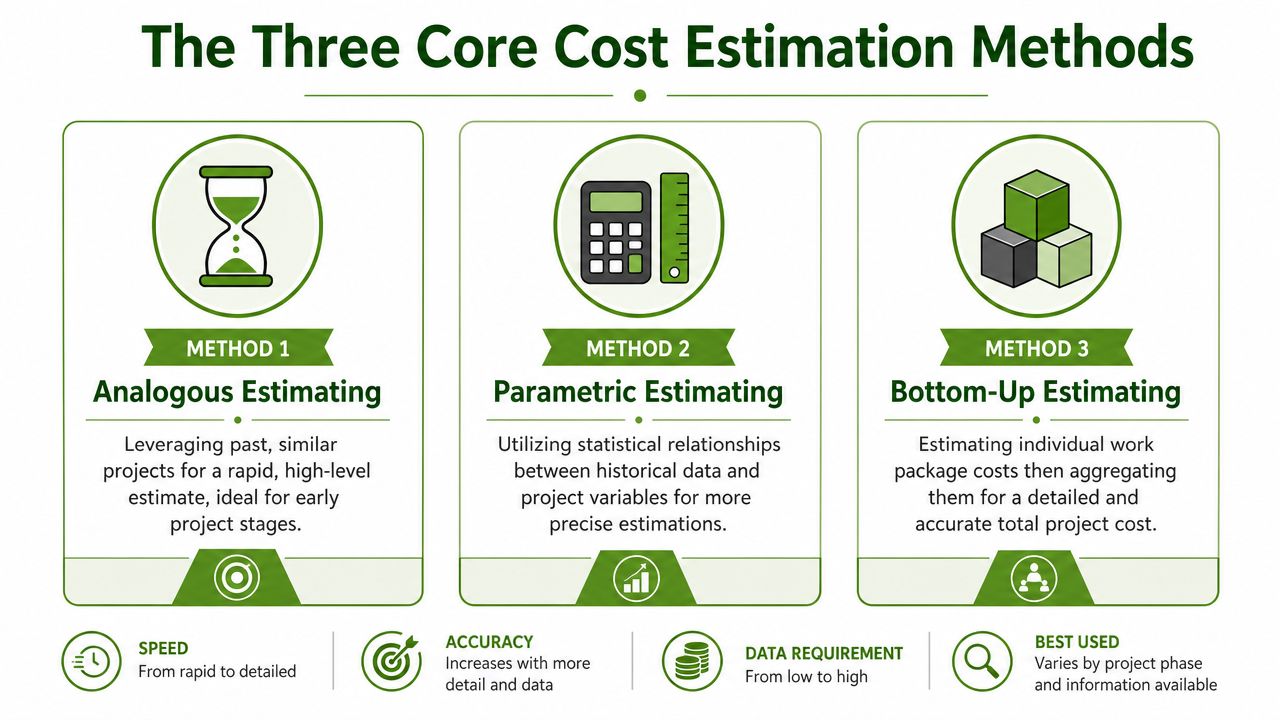

The Three Core Cost Estimation Methods

A grant budget usually starts in one of three places. You either have a past program to compare against, a unit cost you can multiply, or a team ready to price each task one by one.

The right method depends on what you know today, how much staff time you can spend on budgeting, and how closely a funder will examine your numbers. In nonprofit work, that last point matters. A usable estimate does more than total expenses. It shows a reviewer that the budget reflects real delivery conditions, shared costs, and predictable pressure points.

Analogous estimating

Analogous estimating starts with a prior project and adjusts from there. If your organization ran a community garden last year, that budget can give you a reasonable starting number for a second site.

It is fast. That is its strength.

It is also easy to oversimplify. A new neighborhood may need translation, more outreach hours, different insurance requirements, or site work that did not exist the first time. Analysts at Galorath note that analogous estimating often falls in the rough range of about ±25% to ±30%, while bottom-up estimating can reach about ±10% accuracy when complete data is available (Galorath's overview of estimation methods).

Use this method early, or when leadership needs a planning number before the program model is fully settled. For a proposal headed to a funder, treat it as a draft that still needs support.

Parametric estimating

Parametric estimating builds cost from a unit that drives spending. That might be cost per student, per workshop, per home visit, per acre restored, or per participant meal.

Nonprofits use this method all the time, even if nobody labels it that way. Forty tutoring hours at a set staff rate is parametric. Twelve training sessions with a fixed materials cost per session is parametric. The value is not the terminology. The value is that you can explain the math to a funder in one clear sentence.

This method works well for programs with repeatable services. It gets weaker when the units hide complexity. Cost per participant can look neat on paper while masking major differences in transportation needs, interpretation, case management intensity, or rural travel. If your project shares staff, space, or administrative support across activities, HireAccountants' ABC explanation is a practical way to trace those costs back to the work that causes them.

Bottom-up estimating

Bottom-up estimating prices the work at the task level, then rolls those estimates into a full budget. For grant proposals, this is the method I trust most.

A community garden budget built this way would separate site preparation, soil, lumber, tools, volunteer coordination, staff planning time, permits, interpretation, outreach, evaluation, and reporting. That detail takes longer to assemble, but it gives you something funders can follow. It also gives your own team a better chance of catching omissions before submission instead of after award.

This is usually the best choice when the proposal is competitive, the funder expects a detailed budget narrative, or your organization will need the estimate to manage implementation later. If your team needs a starting format, a grant proposal budget template for nonprofit line-item estimates can speed up the first draft.

Which method fits which moment

| Method | Best use | What it does well | Where it breaks |

|---|---|---|---|

| Analogous | Early planning and internal scoping | Produces a fast starting estimate | Carries old assumptions into new work |

| Parametric | Repeatable services with clear units | Connects cost to volume and service logic | Misses variation hidden inside the unit |

| Bottom-up | Formal grant proposals and implementation planning | Shows detail, assumptions, and operational readiness | Requires more staff input and more time |

For many nonprofit proposals, the strongest approach is not choosing one method and stopping there. Start with an analogous estimate to test feasibility, use parametric logic for repeatable services, and finish with bottom-up detail before submission. That combination produces a number you can defend and a narrative a funder can trust.

Building Your Line-Item Budget Detail by Detail

A strong line-item budget starts with scope, not with a spreadsheet. If the work isn't defined, the math won't save you.

That matters because ambiguous scope is the leading cause of cost overruns, and bottom-up estimating requires teams to identify all cost categories, gather actual historical data, and calculate labor using fully loaded employee rates rather than averages, as explained in Intuit's guide to project cost estimation.

Start with the work breakdown

Take an after-school tutoring program. Don't begin with “personnel” and “supplies.” Begin with the work itself.

A basic work breakdown might include student recruitment, family intake, tutor hiring, tutor training, session delivery, progress tracking, snacks, transportation support, and reporting. Once those pieces are visible, the budget gets easier because every line item has a home.

Practical rule: If you can't point to the task that drives a cost, the line item probably isn't ready for the proposal.

Build personnel first

In most nonprofit programs, labor is the largest expense. The cleanest budgets start by mapping who does what, how often, and for how long.

Use actual staff rates, not round numbers that “feel fair.” Include wages, benefits, payroll taxes, and any other organization-specific load factors your finance team applies. If a program manager spends part of their time supervising tutors and part on compliance reporting, split that time intentionally.

For the tutoring program, your personnel list may look like this:

- Program manager time: Oversight, school coordination, scheduling, and grant reporting.

- Tutor time: Direct instruction, lesson prep, attendance, and brief follow-up with families.

- Data or evaluation support: Tracking participation and outcomes.

- Administrative support: Purchasing, reimbursements, background check processing, and filing.

If you need a faster way to structure the sheet itself, this grant proposal budget template can help you organize categories and narrative support before you transfer numbers into a funder form.

Add direct program costs

Once labor is in place, move to the costs tied directly to delivery.

For an after-school tutoring program, that usually includes curriculum materials, printing, student folders, snacks, technology access, background checks, translation, transportation assistance, and space costs if the school or partner site charges usage fees. If you expect tutors to travel between sites, include mileage or transit reimbursements based on your actual policy.

This is also where many teams undercount recurring items. Snacks aren't one purchase. Printing isn't one purchase. Batteries, notebooks, name tags, and replacement materials have a way of showing up month after month.

A simple way to pressure-test these categories is to borrow a planning habit from event budgeting. The simple framework for managing event costs from Ticketsmith is useful because it forces you to separate fixed needs from variable ones and account for operational details people forget under deadline pressure.

Roll it up in a funder-friendly format

Funders don't just need detail. They need readable detail. A useful nonprofit line-item budget usually includes three layers:

- Budget category such as personnel, supplies, travel, equipment, or contractual.

- Line description that names the actual item or role.

- Calculation note that shows how you got there.

For example, “Tutor wages” is weaker than “Part-time tutors for direct instruction, lesson prep, and student progress notes.” “Supplies” is weaker than “Student workbooks, assessment materials, and session snacks.”

What works and what doesn't

Here's the difference I see most often:

- What works: Budgets that mirror the program plan, use real staff costs, and show calculation logic.

- What doesn't: Budgets built from old grant forms, copied labels, and rounded guesses.

The goal isn't to impress anyone with complexity. The goal is to make your estimate easy to trust.

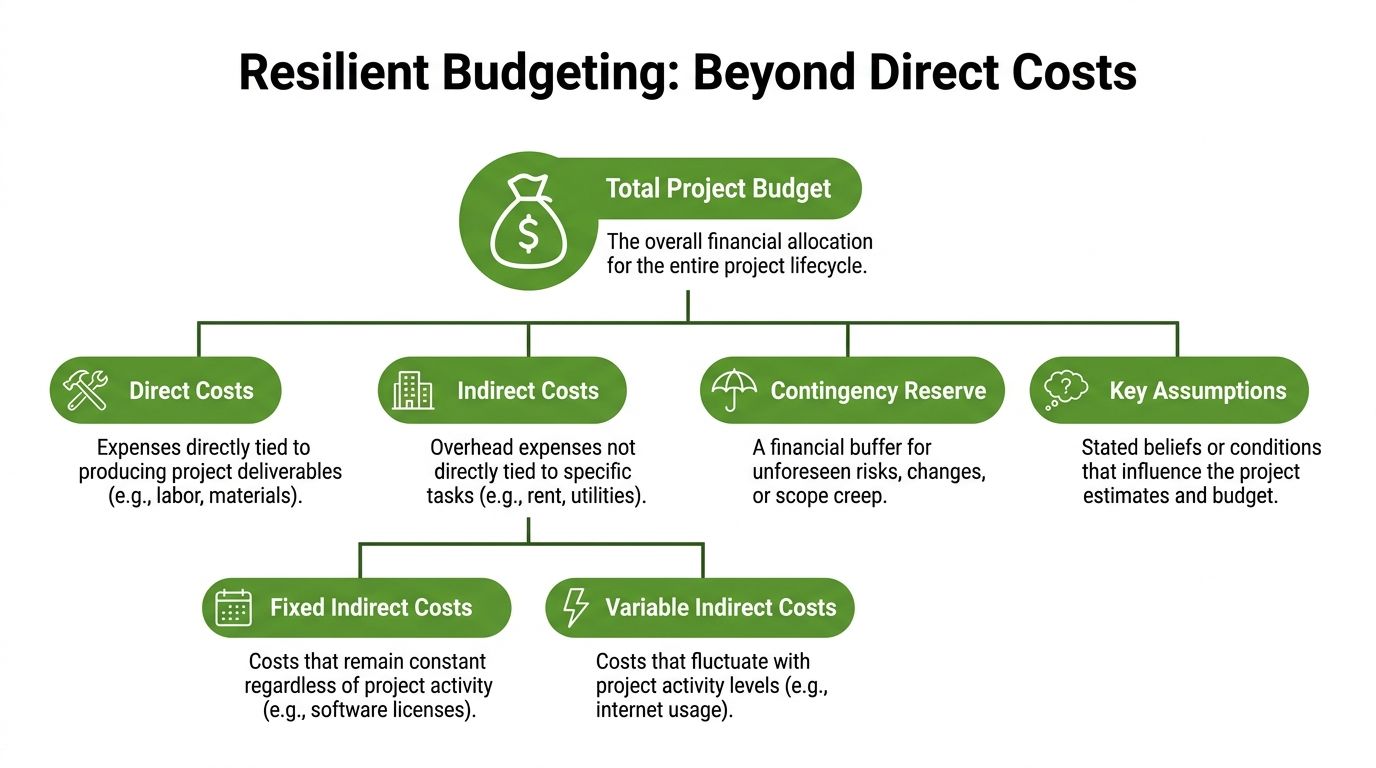

Calculating Indirect Costs Contingency and Assumptions

The direct-cost budget is only part of the picture. Projects fail financially when organizations pretend the visible program expenses are the whole cost of delivery.

Indirect costs are real costs

Indirect costs cover the operating support that keeps the project possible but doesn't sit neatly inside one activity. Think finance, HR, audit support, leadership oversight, shared software, occupancy, insurance, and general administration.

Many nonprofit teams get skittish here because they assume funders only respect “program” costs. That's backwards. Experienced funders know programs don't run themselves.

Your job is to explain indirect costs plainly. If your organization has a formal indirect cost rate or NICRA, use it according to funder rules. If not, explain the basis you used to allocate shared expenses. A basic formula looks like this:

Indirect cost amount = approved or applied indirect rate × allowable cost base

If the funder limits indirect recovery, say so in your internal working budget and track the gap. Don't omit overhead from your real planning just because the application form is narrow.

A helpful reference for making that calculation and framing it for proposals is this guide on how to calculate indirect costs.

Contingency is not padding

Contingency is a reserve for identified risk and uncertainty. It isn't a slush fund, and it shouldn't be presented like one.

This matters even more at early stages, because rough order of magnitude estimates can range from about -50% to +100%, and industry standards suggest setting aside a contingency reserve of 5% to 15% of the total estimated cost to account for risks and unknowns, according to Vista Projects' explanation of estimate classes.

A simple formula works well:

Contingency reserve = total estimated direct and eligible indirect costs × chosen contingency rate

The rate you choose should match the uncertainty in the project. New partnerships, first-time program models, fluctuating vendor pricing, or an uncertain launch timeline all support a stronger reserve. Stable, repeatable programming may justify a leaner one.

Board-ready language: “Contingency covers identifiable delivery risks such as procurement variance, staffing transitions, and startup adjustments. It is not intended for scope expansion.”

Here's a useful explainer if you want a quick refresher before writing the narrative:

Assumptions are where trust is built

A budget without assumptions is just a spreadsheet with good posture.

State what your estimate depends on. If your tutoring program assumes the school provides classroom space, name it. If your garden project assumes donated tools, say that. If your personnel calculations assume current salary schedules remain in effect during the grant period, write it down.

Good assumptions usually answer four questions:

- What did you assume about staffing

- What did you assume about volume or participation

- What did you assume about contributed resources or partnerships

- What did you assume about timing and procurement

Funders don't need every internal note. They do need enough to understand how the numbers were built and where risk sits. That transparency often matters as much as the estimate itself.

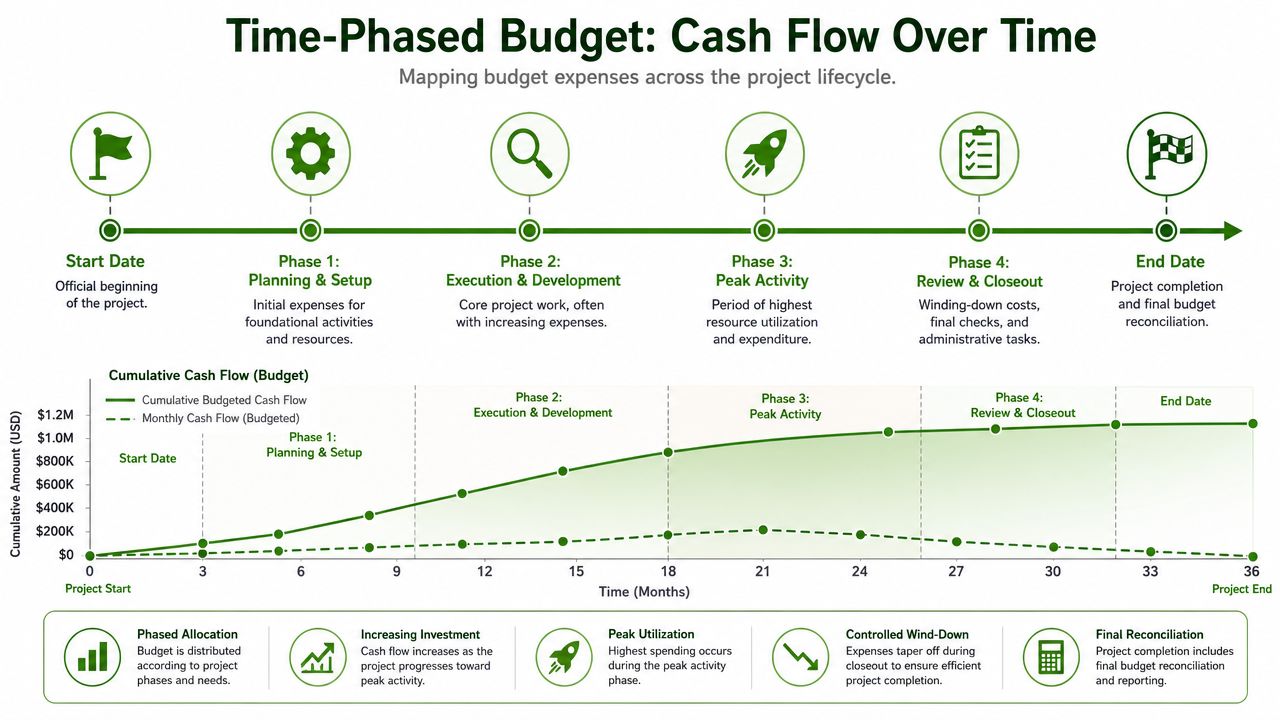

Mapping Your Budget to a Project Timeline

A static budget answers one question. A time-phased budget answers two. How much will this project cost, and when will the organization need the cash?

Funders notice when a nonprofit has thought about timing. So do finance committees. Salaries show up regularly. Training costs cluster early. Evaluation costs often hit late. Equipment purchases may happen before a single participant is served.

Turn the annual budget into a calendar

Take the after-school tutoring program and lay the costs against the grant period. Start with the sequence of work.

Quarter one might carry hiring, background checks, curriculum purchases, onboarding, and family outreach. The middle of the year may concentrate tutor wages, snacks, transportation help, and ongoing supervision. Near closeout, reporting and evaluation may rise while supply spending drops.

A basic time-phased budget can be built in a spreadsheet with columns for months or quarters. Each budget line gets assigned to the period when the expense is expected, not merely when the grant starts.

What funders learn from this view

A timeline-based budget tells a reviewer several useful things at once:

- Operational readiness: You understand what has to happen first.

- Cash flow awareness: You know when spending peaks.

- Grant management discipline: You're less likely to request funds on a schedule that doesn't match delivery.

- Implementation realism: The narrative and budget move in the same order.

If the program narrative says services start immediately but your staffing and purchasing costs don't appear until later, the budget has revealed a planning gap.

A simple layout that works

You don't need fancy software. Use rows for budget lines and columns for periods. Then add a total row at the bottom of each month or quarter.

For the tutoring example, recurring payroll may be spread evenly across the school term, while training costs sit up front and the final evaluation fee lands near the end. Once that pattern is visible, your team can spot problems early, especially if reimbursement timing from the funder is slow.

That's often the hidden benefit. A time-phased budget doesn't just help you win the grant. It helps you survive it.

Common Budgeting Pitfalls That Sink Grant Proposals

Most weak grant budgets don't fail because the team can't use Excel. They fail because the numbers expose shaky planning.

Underestimating staff time

This happens constantly. Teams budget direct service hours and forget planning, supervision, data entry, family communication, procurement, and reporting.

The fix is simple. Budget for the work people perform, not just the part that sounds programmatic.

Forgetting indirect costs

Organizations trim overhead first because they're afraid it looks wasteful. What it looks like is incomplete.

A proposal gets stronger when you show the cost of delivery and explain the basis for indirect recovery clearly.

Using round numbers with no calculation trail

A line item like “Supplies” with one large rounded figure tells a reviewer almost nothing. It signals guessing, even when the team isn't guessing.

Break large lines into understandable components. If the funder form is restrictive, keep the detail in your internal backup and budget narrative.

Budget and narrative telling different stories

The program plan says bilingual family engagement matters. The budget shows no translation, no interpreter support, and no staff time for outreach. Reviewers notice.

Read the budget beside the narrative, not after it. Every major activity in the proposal should have a financial footprint somewhere.

Ignoring math errors and formula drift

One broken cell can undermine confidence fast. So can a subtotal that doesn't match the narrative request.

Use a final review pass that checks formulas, carryforwards, and totals against the funder's required amount. Then have someone outside the drafting process read it cold.

Reviewer lens: A small budget inconsistency makes people wonder where the larger planning inconsistencies are hiding.

Treating justification as optional

Some teams assume the spreadsheet speaks for itself. It doesn't.

A short budget narrative should explain unusual costs, shared costs, constrained rates, and any assumptions a reviewer would otherwise have to guess. Clarity lowers resistance. Silence raises it.

Tools and Workflows to Streamline Your Next Estimate

The best budgeting workflow is boring in the best way. It's repeatable, documented, and easy for another staff member to pick up when someone's out sick two days before deadline.

Build a system, not just a file

A dependable estimating process usually includes a scope checklist, a standard line-item structure, a place to store historical budgets, and a review step where program and finance staff compare assumptions. That combination matters more than any one template.

If your team manages grants alongside events, capital work, or facility upgrades, it can help to study how other sectors track jobs and cost categories. For example, this look at Quickbooks for construction accounting is useful because it shows how disciplined cost tracking improves future estimates, even if your nonprofit isn't in construction.

Use tools that reduce rework

A significant drain on nonprofit teams isn't only calculation. It's hunting through RFPs, rebuilding the same budget logic in different formats, and chasing version control across email threads.

That's why more teams are moving toward centralized grant workflows. A solid overview of what that can look like appears in this guide to grant management software for nonprofits, especially for organizations that need one place to manage deadlines, requirements, documents, and reporting history.

The core principles don't change. Define the scope. Build from actual work. Show your assumptions. Match spending to timing. Make the estimate easy to inspect. That's what funders trust, and it's what your own team will need once the award arrives.

Fundsprout helps nonprofits turn messy grant requirements into organized, defensible proposals. If your team is tired of rebuilding budgets from scratch, chasing deadlines across email, and translating long RFPs by hand, Fundsprout gives you one place to analyze opportunities, structure proposal work, and manage grants from application through renewal.

Try 14 days free

Get started with Fundsprout so you can focus on what really matters.