Your Guide to Small Business Growth Capital

Unlock your potential with this complete guide to small business growth capital. Learn to compare funding types, prepare your pitch, and strategically scale.

Abdifatah Ali

Co-Founder

When you're running a business, you have money for day-to-day operations and money for the big, game-changing moves. Small business growth capital is the latter. It's the funding you find specifically to scale your company, whether that's launching a new product, opening a second location, or expanding into a whole new market.

This isn't the same as working capital, which covers your daily operational costs like payroll and rent. Getting this distinction right is the first crucial step toward finding the right investment to fuel your future.

What Is Small Business Growth Capital?

Let's use an analogy. Think of your business as a house. The money you use for groceries, electricity, and minor repairs is your working capital. It keeps the lights on and everything running smoothly day-to-day.

Small business growth capital, on the other hand, is the money you secure to build a major new addition. It’s a strategic investment meant to dramatically increase your home's value and capacity. You're not using it to patch a leaky faucet; you're using it to execute specific, high-impact growth plans.

This is the financial engine that powers major milestones like:

- Buying new, more efficient equipment to ramp up production.

- Launching a big marketing campaign to capture a new geographic region.

- Hiring a specialized team to build out an innovative product or service.

Why Growth Capital Is a Critical Milestone

Getting growth capital is about more than just the cash. It's a powerful validation of your business model and your vision for the future. It sends a clear signal to the market, your customers, and your team that your organization is ready to climb to the next level.

And this need for growth funding is only getting more common. We're in the middle of an entrepreneurial boom. In 2025, new business formations in the U.S. hit a record high of 478,800 per month. That's a staggering 435% increase from the 90,000 monthly average back in 2004. To keep up, banks issued $84.2 billion in new loans just to businesses with under $1 million in revenue in 2023 alone. You can find more details in these small business statistics for 2025.

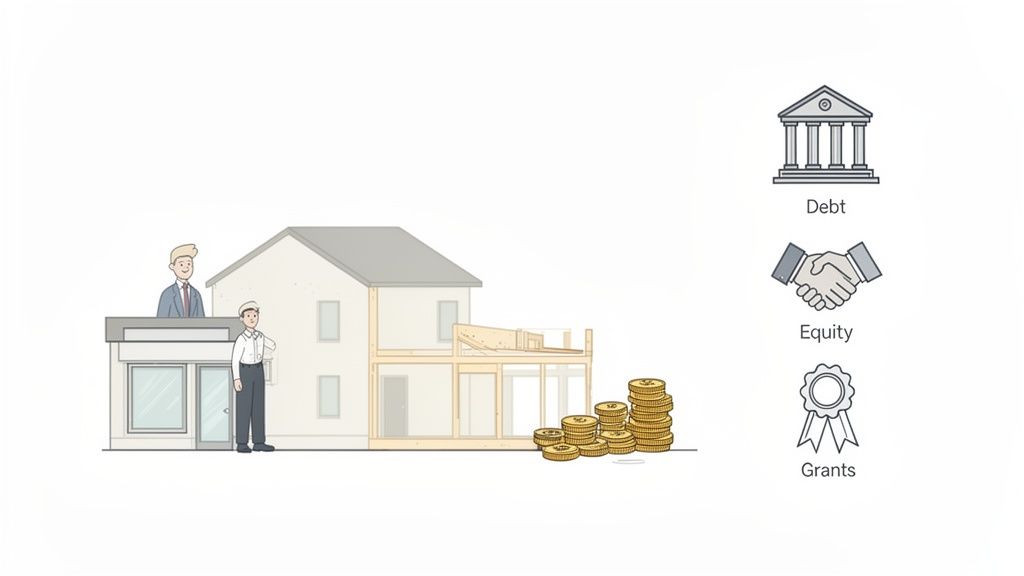

The Main Avenues for Funding Growth

There are a few well-trodden paths to securing growth capital, and each comes with its own set of rules and expectations. The main types are debt, equity, and grants. The right choice for you depends entirely on your business structure, your specific goals, and how much risk you're willing to take on. A fast-moving tech startup might be a perfect fit for equity, whereas a stable, profitable service business might be better off with a traditional loan.

Growth capital is an investment in your company's future, not a patch for its present. The goal is to generate a return—whether financial or social—that far exceeds the initial investment.

To help you get a clearer picture, here’s a quick breakdown of the most common capital types.

Growth Capital At a Glance

This table offers a quick summary of the primary types of growth capital, what they're typically used for, and who usually provides them.

Understanding these fundamental differences is the first step in building a solid funding strategy. This guide will walk you through exactly how to do that.

Exploring the Four Main Types of Growth Funding

Once you’ve decided to chase growth, the big question is: how will you fuel the journey? Think of it like planning a cross-country road trip. A sports car is great for speed, but you wouldn’t use it to haul furniture. A moving truck is perfect for cargo but terrible for a scenic tour.

The same logic applies to small business growth capital. The type of funding you choose has to match where your business is today, where you want it to go, and what you’re willing to trade to get there.

The funding world really boils down to four main roads: debt, equity, mezzanine financing, and grants. Each comes with its own unique set of rules, costs, and opportunities. Getting a handle on the differences is the first step toward making a smart decision that actually helps you grow instead of holding you back.

Let's break them down.

Debt Financing: The Business Mortgage

Debt financing is probably what most people think of when they hear "business funding." It’s a loan. You borrow a lump sum from a lender—a bank, a credit union, an online lender—and you promise to pay it back over time, with interest. Simple as that.

Think of it as a mortgage for your business. You get the cash to build an "extension"—maybe buy new equipment, stock up on inventory, or open a second location—and in exchange, you make steady, predictable payments. The best part? You keep 100% ownership of your company. The bank is just your lender, not your business partner. Once the loan is paid off, you’re done.

Of course, there's a catch. Lenders need to see that you're a safe bet. They’ll pour over your credit history, cash flow statements, and overall financial health. If your business is brand new or your revenue is all over the place, getting a traditional loan can be tough.

Equity Financing: Selling a Piece of the Pie

Equity financing works on a totally different model. Instead of borrowing money, you sell a percentage of your company—a slice of the ownership pie—to an investor for cash. These investors might be wealthy individuals (often called "angel investors") or specialized firms known as "venture capitalists" (VCs).

This is less like taking out a loan and more like bringing on a new co-owner who's got deep pockets. They are making a bet that your company is going to be a massive success, making their slice of the pie worth a lot more down the road. This is the go-to model for high-growth startups, especially in tech, that need a ton of capital to build their product and grab market share long before they turn a profit.

The upside is huge: you get a major cash injection with no monthly loan payments to worry about. The risk is shared. But the trade-off is equally significant. You give up a piece of your company forever and, usually, some control over big decisions. Your new investors have a seat at the table.

An injection of capital from the right investor can provide more than just money; it can offer invaluable expertise, industry connections, and strategic guidance that can dramatically accelerate growth.

And right now, the appetite for this kind of investment is strong. Small businesses came into 2025 feeling optimistic, with nearly 7 in 10 owners (69%) having a positive outlook on their finances. Investors are feeling it too, with the global venture capital market projected to grow at a 17.6% CAGR through 2033. This makes sense when you consider that 64% of founders start with less than $10,000 of their own money. You can dive deeper into these numbers in the latest small business growth report.

Mezzanine Financing: The Hybrid Approach

Mezzanine financing is a more advanced, hybrid option that mixes parts of both debt and equity. It's not for beginners. This is typically for established, profitable companies that need funding for a big move—like an acquisition—but might not qualify for another traditional bank loan.

Picture it as a layer of financing that sits between senior debt (your main bank loan) and pure equity. It usually starts out as a loan with interest payments, but it has an "equity kicker" attached. This kicker gives the lender the right to convert their debt into an ownership stake in your company if, for some reason, you can't repay the loan as agreed.

It’s a powerful tool that offers more flexibility than a standard loan, but it’s riskier for you because you could end up giving away equity. It’s the right move only when other doors are closed and the growth opportunity is too big to pass up.

Grant Funding: The Mission-Aligned Award

For certain businesses, and especially for nonprofits, grants are the holy grail of funding. A grant is money given to you by a government agency, a private foundation, or a corporation to support a specific mission or project. And the best part? You don't have to pay it back.

Think of it as a sponsorship. A funder gives you capital because your work aligns with their own goals—whether that’s pioneering new technology, improving a community, or advancing the arts. You get to expand your impact without taking on debt or giving up a single share of ownership.

One of the most sought-after categories is government grants for startups, which can provide that critical seed money for new, innovative ideas. The main hurdle with grants is the fierce competition. The application process can be grueling, and if you win, the reporting requirements are usually strict. You have to prove you’re using the money exactly as you promised.

Comparing Growth Capital Options

To make sense of it all, it helps to see these options side-by-side. Each has a different impact on your ownership, control, and financial obligations.

Ultimately, choosing the right funding isn’t just about getting a check. It’s a strategic decision that will define how your company grows for years to come. By understanding the core trade-offs between debt, equity, and grants, you can find the path that best fits your vision.

The Numbers Funders Actually Care About

If you want to secure growth capital, you have to learn to speak the language of funders. Whether you're talking to a bank, an angel investor, or a foundation, they all rely on a specific set of numbers to get a quick read on your organization's health, stability, and future potential. These metrics tell a story about where you've been and, more importantly, your ability to deliver a return on their investment.

Think of it like having the answer key before a test. When you understand these metrics from a funder's point of view, you can diagnose your own financial weak spots and build a powerful, data-backed case for why you’re a smart bet.

This decision tree helps visualize how factors like your growth stage and how much ownership you're willing to give up can point you toward the right kind of funding.

As you can see, a startup just finding its footing might choose between equity and grants, while a more established business with predictable revenue would likely lean toward debt to avoid giving up ownership.

Key Financial Metrics For-Profit Businesses Must Know

For any lender or investor looking at a for-profit company, your financial statements are where the rubber meets the road. They’ll zoom in on a few key figures to gauge your operational grit and the level of risk they’d be taking on.

Cash Flow: Honestly, this is the big one. Positive cash flow shows that your day-to-day operations are actually making more money than they're spending. It signals stability and proves you can handle new loan payments without breaking a sweat. For lenders, healthy cash flow is the clearest sign of a low-risk borrower.

EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization): It sounds complicated, but EBITDA just gives a clean look at your company’s core profitability. By stripping out accounting and financing decisions, it allows funders to compare your performance to others in your industry on an even playing field.

Debt-to-Equity Ratio: This one is simple: it shows how much of your business is funded by debt versus the money you (the owner) have put in. A high ratio can be a red flag, suggesting you’re stretched thin and might struggle to take on more debt. When considering your pitch, funders will dig into your spending plans and want to see they make sense for growth; it's worth learning how to calculate capital spending for smart business growth.

A compelling financial story isn't about one great quarter. It's about consistency. A proven track record of steady, predictable growth in these key areas is what truly builds a funder’s confidence.

Mission-Aligned Metrics for Nonprofits

While nonprofits absolutely need to be financially healthy, funders—especially grantmakers—are just as focused on your ability to deliver on your mission. You have to prove your impact with numbers to show you’ll be a good steward of their money.

Here are the metrics that really move the needle in the nonprofit world:

Program Efficiency Ratio: This metric reveals what percentage of your spending goes directly to your programs versus what's eaten up by administrative and fundraising costs. A high ratio, typically over 75%, is a great sign that donor funds are being put to work where it counts.

Fundraising Efficiency (Cost to Raise a Dollar): This tells funders how much you have to spend to bring in a single dollar. A low number here is fantastic—it shows your development efforts are sustainable and that their money will fuel your mission, not just a constant chase for more funding.

Social Return on Investment (SROI): SROI is a powerful way to tell your impact story. It puts a dollar value on the social, economic, or environmental good your work creates. For instance, an SROI of 5:1 means for every $1 they invest, you generate $5 in real value for the community. That’s a powerful statement.

Demonstrating these outcomes takes serious data collection and clean reporting. Managing your grant-funded projects effectively is key, not just for staying compliant, but for gathering the proof you'll need for the next funder. For more on this, you can find some great pointers in our guide to grant management best practices.

When you master the metrics that matter for your organization, you stop just asking for money. You start building an undeniable, data-driven case that proves your potential, lowers the funder’s perceived risk, and turns your pitch from a simple request into a can't-miss investment opportunity.

How to Build Your Funding Readiness Checklist

Think of securing growth capital less like a sprint and more like training for a marathon. It’s all about discipline, smart planning, and getting your business into peak condition long before you ever walk into a funder’s office. It’s not enough to have a brilliant idea; investors and lenders need to see a professional, organized operation that’s built to execute.

Walking in unprepared is one of the most common—and fatal—mistakes you can make. The competition is fierce. Access to growth capital is still a massive hurdle for small businesses, with a staggering $5.7 trillion deficit in emerging markets alone. Even here in the U.S., loan approval rates from traditional banks hover between 44-52%, and 49.2% of owners admit they struggle with cash flow. This just goes to show how critical it is to have your act together to stand out.

This checklist is your training plan. Use it to find and fix the weak spots in your pitch and build a case so compelling that funders can’t ignore it.

Fortify Your Financial Documentation

Your financial documents are the absolute bedrock of your request. They need to be clean, accurate, and tell a clear story of where you’ve been and where you’re headed. Think of them as the architectural blueprints for your business—no one is going to fund the construction of a skyscraper without them.

Before you even think about approaching a funder, get these non-negotiables in order:

- Audited or Reviewed Financial Statements: Have professional statements (Balance Sheet, Income Statement, Cash Flow) for at least the last three years. An official audit gives funders the highest level of confidence and shows you’re serious.

- Detailed Cash Flow Projections: Build out projections for the next three to five years. These can’t be pulled out of thin air; they must be grounded in solid assumptions and show exactly how this new capital will drive revenue and affect expenses.

- Current Accounts Receivable and Payable Aging Reports: These reports are a real-time health check, showing who owes you money, who you owe, and how well you’re managing the flow of cash.

- A Full List of Assets and Collateral: If you’re going after debt financing, you’ll need a detailed list of all business assets that could be used to secure the loan.

Craft a Compelling Strategic Plan

If your financials are the what, your strategic plan is the how and the why. It’s your narrative, where you connect the dots for funders and show them precisely how their money will be put to work to generate growth. This isn't a wish list; it's a detailed, actionable roadmap.

A great strategic plan answers the big questions with clarity and conviction. It needs to lay out a powerful vision and back it up with a logical, step-by-step framework. To get started building a narrative that clicks with funders, take a look at our guide on creating a fundraising plan format.

A funder’s biggest question is always, "How will my money be used, and what is the expected outcome?" A vague plan screams risk. A detailed one shows foresight and accountability.

Your plan needs to draw a straight line from the capital you receive to a measurable result. For example, be specific: "$50,000 for a new CNC machine will boost our production capacity by 30%, which lets us take on an extra $150,000 in orders each year."

Demonstrate Team and Leadership Alignment

At the end of the day, funders invest in people. They're betting on you and your leadership team to navigate the tough times and execute the plan. You have to prove you have the right people in the right seats to make it happen.

Put your team's expertise front and center:

- Professional Bios: Write detailed biographies for your key executives. Don’t just list job titles; highlight relevant industry experience, past wins, and the specific skills they bring to your growth strategy.

- An Organizational Chart: A simple chart that shows roles, responsibilities, and who reports to whom is invaluable. It proves you have a thought-out structure that’s ready to scale.

- Board of Directors or Advisors: If you have them, show them off. A strong, experienced board can dramatically increase a funder's confidence in your governance and long-term vision.

By methodically working through these three pillars—financials, strategy, and team—you stop looking like a hopeful applicant and start looking like a funder-ready powerhouse.

Growth Capital Strategies for Mission-Driven Nonprofits

For mission-driven nonprofits, the idea of small business growth capital looks a little different. The end game isn't maximizing shareholder profits; it's about maximizing social impact. Here, growth isn't measured in market share, but in lives changed, communities strengthened, or progress made toward a vital cause.

This single distinction reframes the entire funding conversation. Where a for-profit company might weigh the pros and cons of debt versus equity, a nonprofit has to find capital that can fuel its mission without ever compromising it. That’s why grant funding is, and should be, the go-to strategy for any nonprofit looking to expand its reach.

Why Grants Are the Gold Standard for Nonprofits

Grants are a different beast entirely. They aren’t loans you have to pay back, and they don’t force you to give up a piece of your organization. They are awards, given by foundations, corporations, and government agencies that truly believe in what you do and want to help you succeed. That alignment is everything.

When you secure a grant, you’ve found a partner, not just a lender. This kind of partnership lets you scale up your programs, bring on essential staff, or invest in critical infrastructure—all without the crushing weight of debt or the mission-drift that can happen when you're chasing profit-focused investors.

For a nonprofit, the right grant is more than just money—it's an endorsement of your mission and a catalyst for deeper community impact. It allows you to focus on what you do best without the distraction of a looming repayment schedule.

But winning this kind of funding means facing a unique set of challenges that for-profit businesses rarely encounter. Funders need to see a clear, believable path to both financial stability and measurable social good.

Overcoming Unique Nonprofit Funding Hurdles

Nonprofit leaders have to answer two make-or-break questions for potential funders: "Is your organization built to last?" and "How do we know you're actually making a difference?"

Answering them requires a different kind of pitch—one built on data-driven storytelling.

You have to prove your impact with concrete numbers. Instead of talking about EBITDA, you'll be highlighting your Program Efficiency Ratio. Instead of a classic ROI, you’ll present a compelling Social Return on Investment (SROI), demonstrating how every dollar invested generates significant, tangible value for the community you serve.

Beyond that, you need a rock-solid plan for the long haul. Funders are cautious about organizations that depend on a single income stream. A diversified funding strategy—blending individual donors, corporate sponsorships, and maybe even earned revenue—shows you have the foresight to make sure your mission endures. For those focused on building this long-term strength, it's wise to explore specific funding opportunities like nonprofit capacity building grants that are designed to fortify your organization from the inside out.

Using Modern Tools to Compete and Win

The grant-seeking world is incredibly competitive. Success often boils down to efficiency, precision, and the power of your story. This is where modern AI-powered tools have become a real game-changer, leveling the playing field for nonprofits of all sizes.

These platforms can slash the time you spend searching for opportunities by delivering a handpicked pipeline of grants that perfectly match your mission. Instead of your team digging through thousands of irrelevant listings, they can pour their energy into the funders who are most likely to say yes.

AI assistants can then help you write powerful proposal narratives, using your own documents and impact data to tell your story in a consistent, authentic voice. This makes sure every application you send isn't just well-written, but also rings true to your mission. Finally, these tools help simplify the complex reporting and compliance that comes with grant money, keeping your funders happy and paving the way for future support.

By approaching growth capital through a mission-first lens—and using the right technology to back up your efforts—nonprofits can build a powerful and sustainable engine for scaling their impact.

Answering Your Top Questions About Growth Capital

Diving into the world of small business growth capital can feel like learning a new language. You're bound to have questions, and getting straight answers is the first step toward building a funding strategy that actually works.

Let's break down some of the most common questions business and nonprofit leaders have when they start looking for the fuel to expand. Think of this as the practical advice you need to move forward with confidence.

How Much Growth Capital Should I Ask For?

This isn't a number you should guess. The right amount has to come directly from a detailed, bottom-up financial model that's built on your strategic growth plan. Before you even think about a final figure, you need to calculate the precise cost of every single initiative you're planning.

This means getting granular. Itemize everything, from hiring new team members and buying specific equipment to launching that ambitious marketing campaign you've been dreaming of. Your "ask" should be the sum total of all these costs, plus a healthy contingency fund—usually 10-20%—to handle the inevitable surprises that always crop up.

Requesting too little puts your entire growth plan at risk, while asking for too much signals to funders that you haven't done your homework. A justifiable number, backed by a solid plan, shows you've thought through how every single dollar will be used to generate a specific, measurable return—whether that’s profit or social impact.

What Is the Most Common Mistake When Seeking Funding?

Hands down, the single biggest mistake is a lack of preparation. It happens all the time: an organization with a fantastic idea approaches funders but doesn't have the professional documents or strategic clarity to back it up. For any experienced investor, lender, or grant reviewer, that’s an immediate deal-breaker.

What does poor preparation look like?

- Outdated Financials: Showing up with financial statements that are months, or even years, old.

- A Vague Plan: Not having a clear, detailed roadmap for how the funds will be spent and what the results will be.

- No Market Research: Being unable to demonstrate a deep understanding of your industry, competitors, and the customers you serve.

Funders see hundreds, sometimes thousands, of proposals. They can spot an unprepared organization a mile away. A very close second mistake is chasing the wrong type of funding—like a nonprofit taking on high-interest debt for a program that can't possibly generate revenue. Putting in the work to get your house in order and picking the right funding vehicle is everything.

Can I Use Growth Capital to Cover Operating Losses?

This is a critical point, so let's be direct: no. Mixing this up can torpedo your funding request before it even gets off the ground. Growth capital is strictly for expansion—activities designed to generate future returns. Think opening a new location, investing in technology, or buying machinery to boost production.

The money for your day-to-day costs, like payroll, rent, and utilities, is called working capital.

Using growth capital to plug holes in your operating budget is a massive red flag for funders. It tells them your core business model isn't sustainable. It suggests there are fundamental problems with profitability or cash flow that need to be fixed first. Funders want to invest in scaling a healthy operation, not bailing out a struggling one. If you’re facing operational shortfalls, you have to solve those underlying issues before you can realistically seek capital for expansion.

Research backs this up. One study found a powerful link between how businesses used their funding and the growth that followed. Companies that directed capital toward forward-looking projects—like launching new products or scaling up operations—saw their growth rates jump by an average of 70 to 95 percentage points. The data is clear: funders are backing a growth story, not a survival plan. Before you approach them, make sure you have a compelling one to tell.

Finding the right funding opportunities and crafting winning proposals is a major challenge for mission-driven organizations. Fundsprout is an AI-powered platform designed to help nonprofits succeed, from finding perfectly matched grants to writing compelling narratives and managing compliance. Discover how you can build a stronger funding strategy with Fundsprout.

Try 14 days free

Get started with Fundsprout so you can focus on what really matters.